If you entered this NFL season as a Kansas City Chiefs fan, you’re probably hoping for a Super Bowl win after clinching three of the past five Super Bowls and having Patrick Mahomes as your quarterback and Taylor Swift backing the team. (As a Patriots fan, I remember that feeling.) Similarly, after the S&P 500 beat earnings estimates for several quarters, investors aren’t just hoping to beat earnings. They are looking for both a beat and better guidance going forward. Investors had to settle for just one of those in the second quarter.

With 99 percent of the S&P 500 reporting, 79 percent beat earnings expectations. This is just above the five-year average of 77 percent. But they beat estimates by only 3.6 percent, well below the 8.6 percent average the market has gotten used to over the past five years. Market valuations had risen to 21x forward earnings estimates during reporting season, which caused investors to punish earnings misses more severely this quarter. Companies saw a 4.4 percent average decline from the two days before to two days after missed earnings estimates—worse than the historical 2.3 percent average decline. Conversely, companies saw only a 0.9 percent gain if they beat estimates. It’s tough to remain on top.

The Biggest Companies Still Driving the Market

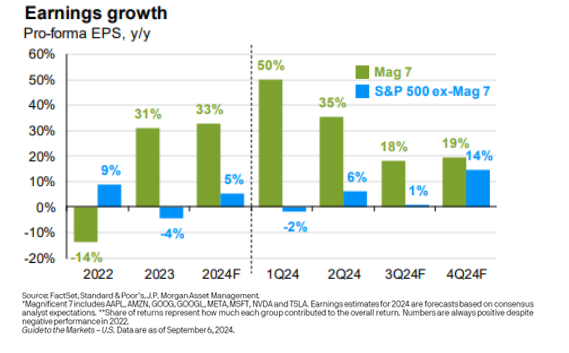

As we entered earnings season, the Magnificent Seven (i.e., Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla) were expected to drive earnings with 28 percent growth, while expected growth for the rest of the index was only 4 percent. The top names met those high expectations, delivering 35 percent growth for the quarter. The rest of the index, on the other hand, had only 6 percent growth.

Nvidia may be a prime example of rising expectations, as it beat earnings estimates by 5.2 percent during the quarter but still saw its stock price fall 6.4 percent after reporting earnings. This story is likely to persist in the third quarter, with the Magnificent Seven expected to report growth of 18 percent, while the rest of the index is expected to show growth of only 1 percent. Analysts are expecting earnings growth to broaden out beyond the third quarter. How that plays out with the current dispersion in valuations could affect relative performance between the top names and the rest of the index.

What’s Happening Beyond the Top Names

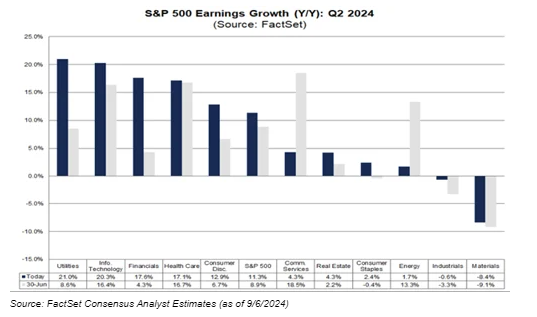

From a sector perspective, the top names drove the earnings picture in their respective sectors, including Apple, Microsoft, and Nvidia in tech; Amazon in consumer discretionary; and Meta and Alphabet in communication services. But there were still solid earnings across the board. Nine of 11 sectors reported year-over-year growth in the second quarter. Utilities, financials, and health care were three of the top five sectors. All saw double-digit growth—and these sectors do not contain any of the Magnificent Seven. Relative to expectations at the beginning of the quarter, utilities and financials handily beat earnings expectations. There was broad-based growth within these sectors, with no single name providing the reason for the earnings beat.

On the negative side, communications services suffered, primarily due to Warner Bros. Discovery taking a $9.1 billion write-down of goodwill primarily related to its TV assets and the uncertainty of fees from cable and satellite distributors. Several energy names guided down and/or missed earnings in Q2, including Chevron and Exxon Mobil due to lower refining margins. Falling oil prices after quarter-end could continue to put pressure on those firms but could also lead to better margins for companies where oil is a cost.

What Does a Mixed Quarter Mean for the Future?

While the market was expecting more from companies in the second quarter, analysts lowered expectations for the third quarter providing an easier bar for companies to beat with growth expectations of only 4.9 percent. Still, with valuations hovering above 20x forward earnings, companies will likely need to give analysts a reason to maintain their 15 percent earnings growth expectations in the fourth quarter and for the full year in 2025. Revenues that were just above 5 percent in the second quarter are expected to remain there, continuing to put pressure on firms to maintain high profit margins through cost reductions to meet those earnings targets.

Don’t Count Out the Big Names

Despite some disappointing economic data recently, expectations remain high. And just like any fan hoping for a Super Bowl or bust, it might be tough not to be disappointed. Despite that, counting out the biggest U.S. companies or a quarterback like Patrick Mahomes is something I’m not ready to do.

Disclosure

The information on this website is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets.

The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. All indices are unmanaged and investors cannot invest directly in an index.

The MSCI EAFE (Europe, Australia, Far East) Index is a free float‐adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index consists of 21 developed market country indices.

One basis point (bp) is equal to 1/100th of 1 percent, or 0.01 percent.

The VIX (CBOE Volatility Index) measures the market’s expectation of 30-day volatility across a wide range of S&P 500 options.

The forward price-to-earnings (P/E) ratio divides the current share price of the index by its estimated future earnings.

Third-party links are provided to you as a courtesy. We make no representation as to the completeness or accuracy of information provided on these websites. Information on such sites, including third-party links contained within, should not be construed as an endorsement or adoption by Commonwealth of any kind. You should consult with a financial advisor regarding your specific situation.

Member FINRA, SIPC

Please review our Terms of Use.

Commonwealth Financial Network®

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Commonwealth Financial Network

Read more commentaries by Commonwealth Financial Network