In an election year, we are bound to hear a lot of commentary about the merits and drawbacks of both major candidates’ economic policies. History shows that while a president’s policies can make life easier or more difficult for various sectors of the economy, U.S. Federal Reserve (Fed) policy has much more impact on the economy overall.

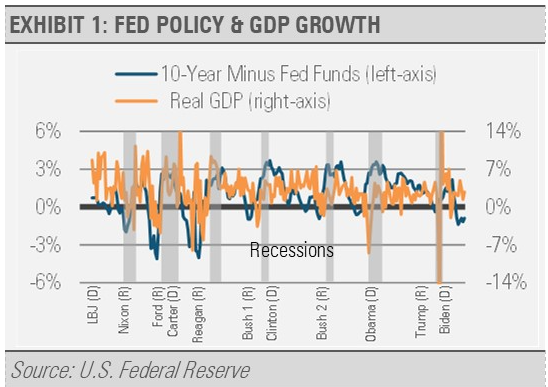

Regardless of president, party, or economic policy, it’s Fed policies that have been the primary drivers of inflation and other measures of economic health. Among the Fed’s policy levers is the ability to set short-term interest rates. When running a restrictive monetary policy to fight excessive inflation, the Fed may increase short-term interest rates to a level that is higher than long-term interest rates, known as an inverted yield curve. Regardless of president or party in office during an inverted yield curve, a recession has almost always followed. When the Fed is running a looser monetary policy and holding short-term interest rates substantially below long-term interest rates, the economy has typically grown at a more robust pace. No president or party has such a history of influencing the backdrop for economic growth as the Fed.

We view Fed policy decisions as the primary driver of the recent bout of inflation. Yes, the government overstimulated the economy with massive fiscal spending and supply chain disruptions exacerbated the economic challenges created by a huge jump in demand. This large jump in demand was caused by the spike in household incomes that was a direct result of the multiple fiscal stimulus packages. But the Fed was overseeing all of this and is the only entity that can control the supply of money in the economy. Inflation is typically the result of too much money chasing too few goods and services. Along with the massive increase in federal government spending through multiple stimulus packages well beyond what was necessary, the Fed added to the inflation trouble by expanding the monetary base further rather than identifying and neutralizing the inflation risk through tighter monetary policy. Only after inflation proved to be persistent and not transitory did the Fed begin to fight inflation. Since the Fed began tightening policy, the annual growth rate of the Consumer Price Index (CPI) has dropped by 2/3rds and is closing in on the Fed’s inflation target.

This is just one example of how powerful Fed policy can be. The Federal Reserve Act of 1913 gave the Fed responsibility for setting monetary policy. There are three tools of monetary policy: open market operations (buying and selling government securities), the discount rate (setting short-term interest rates), and reserve requirements (commercial bank regulatory requirements).

There had been some concern that when the Fed was holding short-term interest rates near zero, their tool kit was limited as they would be unable to reduce interest rates in order to offset economic weakness. Now that interest rates have moved much higher, the Fed is fully equipped across its entire set of tools to manage monetary policy as appropriate to respond to any new macroeconomic challenges.

Fed independence and leadership consistency are key to a stable economy. We have seen the ill effects of when central banks lose their independence and instead become subject to the whims of politicians. For example, it is widely understood among economists that the U.S. bout of inflation in the 1970s was initiated by then-Fed Chairman Arthur Burns acquiescing to President Nixon’s pressure to keep interest rates low despite building inflationary risks.

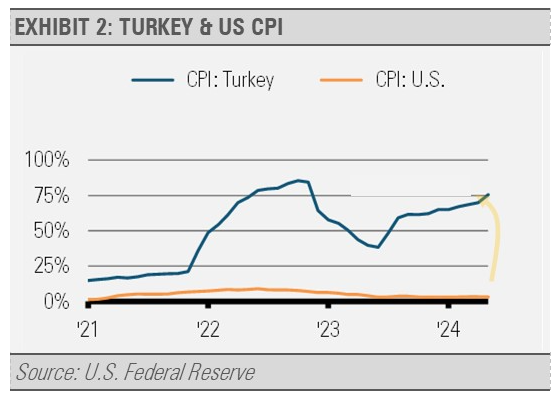

More recently, Turkey’s bout of inflation and the plunge in the value of the Turkish currency, the lira, is a great example of why the lack of central bank independence can be problematic. Turkish President Tayyip Erdoğan previously stated that he believed high inflation is the outcome of high interest rates. This goes against the mainstream thinking and evidence that suggests the relationship is the other way around.

Beginning in late 2021, the Turkish central bank followed Erdoğan’s instructions with a series of reductions in interest rates as the government aimed to stimulate domestic investment and support export-oriented sectors.

However, the decision to cut interest rates came with a trade-off. The new economic policy targeting lower interest rates did indeed spur inflation. While the U.S. experienced a painful bout of inflation, measured as the year-over-year change in consumer prices, the pain the U.S. experienced pales in comparison to what Turkey continues to experience with the annual change in prices peaking at more than 80% and consistently exceeding 40%.

At a time when several emerging markets were preparing for tighter monetary policy, the interest rate cuts led to a weakening of the lira. As Turkey’s economy is reliant on imported goods in several sectors, the currency depreciation caused increasing pressure on consumer prices. The recent Turkish experience is just one example of what can happen when a central bank falls under political influence.

In addition to independence, we believe that consistent application of monetary policy is a key ingredient to stable prices, jobs creation, and economic growth. Going from one extreme to the other risks a negative shock to the system as we saw in Turkey. This is why we prefer the steady hand of current Fed Chairman Powell to the more extreme hawkish and dovish views we sometime see in the press. Powell has publicly committed to finishing out his current term as Fed Chairman which lasts until May 2026, which we view as a strong positive for the U.S. economy.

As has been the case for decades, it is the Fed who holds the greatest influence of U.S. macroeconomic events. This will hold true regardless of who wins the presidential election this November.

For more news, information, and analysis, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by Stringer Asset Management