Key Takeaways

- 2Q24 earnings season were solid in aggregate

- Current 2025 estimates are likely too high

- Mega-cap tech remains a standout

That’s a wrap! This week marks the ‘unofficial’ end to 2Q24 earnings season – and aside from a few wobbles, it has been reasonably good. S&P 500 earnings growth came in at a solid 11.2% YoY pace – its best quarterly performance since 4Q21. MAGMAN’s earnings remained strong (~40%) and earnings from the rest of the Index (i.e., the other 494) advanced 5.6% – its highest earnings growth since 3Q22. And, margins continued to expand (12.7%) – above the 10-year average of 11.1% and had the best quarter since 3Q21. But given extended valuations, the bar was high – with companies that beat on earnings rewarded less than average and those who missed earnings punished more than average in the days following their earnings releases. Below are some of the other key themes that emerged from this quarter’s earning season:

- No recession, but slowdown occurring | The term ‘recession’ was notably absent amidst earnings calls this quarter. In fact, the number of companies mentioning the word ‘recession’ declined to the lowest level since 2006! However, it’s worth mentioning that most companies are reporting data from Easter until June, and economic momentum has changed markedly in the last two months. For example, several companies across a variety of industries (Home Depot, Zip Recruiter, Trex) have noted that economic activity softened in July and is likely to continue to do so through at least the third quarter.

- 2025 EPS may be too optimistic | While 2Q earnings were solid, companies offered soft forward guidance amid slowing activity. All eleven sectors experienced downward revisions to their 3Q estimates, with the broad S&P 500 down 2.6%. However, consensus EPS estimates for 2025 ($277/share) were largely unscathed – still revised up over 1% YTD and representing ~15% EPS growth over 2024! Given our forecast for slowing economic activity near term, 2025 EPS estimates are likely too optimistic and will need to be revised lower. Amid still elevated valuations, this is likely to lead to more volatility.

- Broad based consumer slowdown | Consumer weakness was a key theme throughout the 2Q24 earnings season. While pockets of weakness occurred in prior quarters (e.g., travel in 2020, durable goods in 2023), this was the first quarter of a broad slowdown across most industries. Case in point: a weak consumer was cited in restaurants (McDonald’s), home improvement (Home Depot), online retailers (Amazon) and staples (Procter & Gamble). And areas that have been resilient up until now, such as travel (Hilton, Airbnb) flagged a more discerning consumer who is increasingly looking to trade down. This slowdown in spending filtered through to earnings, with the Consumer Discretionary sector ex-Amazon (given its tech-related revenue exposure) posting its weakest EPS growth (+0.5% YoY) since 4Q20! Further declines (-1.9%) are likely in 3Q.

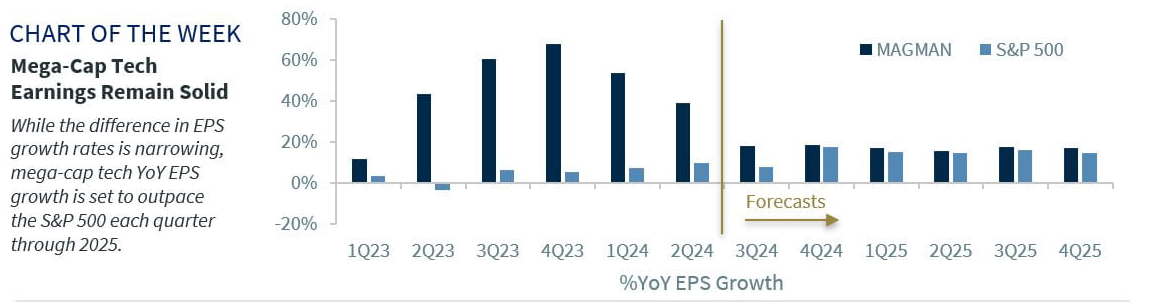

- Mega-cap tech remains a standout | While Nvidia has not yet reported, mega-cap tech (MAGMAN) underperformed the S&P 500 by an average of ~1.1% in the three days following reporting results—its first decline since 3Q22. The softer performance likely reflects elevated expectations heading into the quarter, as MAGMAN’s earnings remain strong. Mega-cap tech earnings growth rose ~40% YoY – outpacing the S&P 500 for the sixth straight quarter. While all the mega-cap tech names beat bottom line estimates, the 6.1% aggregate beat was the lowest since 4Q22 – which likely contributed to the slight underperformance. On a bright note, each of the companies highlighted robust demand and investment in AI-related products that should support earnings moving forward. In fact, MAGMAN’s EPS growth is expected to outpace the S&P 500 each quarter through 2025. Strength in earnings is why we favor mega-cap tech and would use any periods of weakness as buying opportunities.

- Fed Rate cuts needed | 2Q earnings calls highlight that momentum is building for Fed rate cuts. Here are three reasons why:

- Prohibitively high interest rates | Elevated interest rates are hampering economic activity across a wide swath of the economy. For the consumer, Home Depot and other durable goods areas noted that consumers are deferring larger projects waiting for rates to come down, which is also consistent with broader housing market activity. For businesses, select industrials noted slowing demand as customers remain cost conscious amidst a higher rate environment.

- Slowing labor market | Official metrics (e.g., monthly job growth, job openings, claims) suggest a slowing labor market. The slowdown was corroborated in earnings calls. For example, Robert Half, a staffing company and one of our ‘on the ground’ labor market indicators, noted that it is seeing signs of project and hiring deferrals.

- Further moderation in inflation | Given a stretched consumer, businesses noted a loss in pricing power. With consumers pushing back on price increases, companies have focused on volume growth rather than price increases. This is driving retailers and restaurants to ramp up promotional activity to drive sales. This bodes well for a further deceleration in inflation.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.