Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- S&P 500 ex-MAGMAN earnings are improving

- Higher bar for 2Q earnings could lead to volatility

- The health of the consumer will be in focus

The Pendulum Swings Back to the Micro (from Macro). This week marks the official start to 2Q24 earnings season, with the big banks among the first to report. While much of the last six weeks has been dominated by the softening macro backdrop, the S&P 500 looked past the weakening data – notching 37 record closes already this year. The reason: improving earnings. And with earnings a fundamental driver of the equity market, the next six weeks will provide a glimpse into how companies and consumers are navigating the growth slowdown. The results will be key to whether stocks can hold onto and potentially build on their recent gains or suffer a near- term pullback. Below we provide an early look at some of the key trends that will drive the market in the weeks ahead and what to expect during the upcoming earnings season:

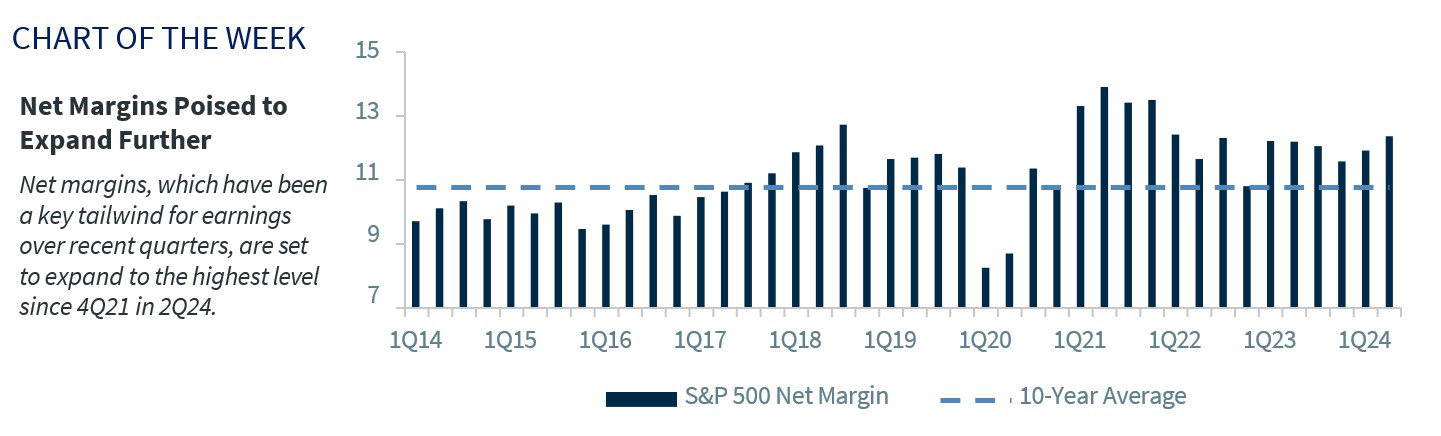

- Headline figures poised to accelerate | With valuations at the highest level since 2021, earnings will need to be the catalyst to drive the market higher as current valuations have already priced in much of the good news. Fortunately, given the resilience of the economy up until this point, earnings are on track to rise at a healthy pace. In fact, consensus expectations for S&P 500 earnings are for them to climb 9.5% on a year-over-year basis in 2Q24 – the fourth consecutive increase and the fastest pace since 4Q21. More important, if earnings beat by even a touch, 2Q24 earnings growth could easily end up with a double-digit gain! Despite the slowdown in the economy, top-line sales growth should record its 15th consecutive positive quarter, with sales rising (+4.5%) at their fastest pace since 4Q22. In addition, margins – a major tailwind for S&P 500 earnings in recent quarters – should remain above their 10-year average (10.8%) for the 14th consecutive quarter and expand to the highest level (12.4%) since 4Q21.

- Tech remains a standout/rest of index improving | In 2Q, seven out of the 11 sectors are expected to post positive EPS growth. Much like recent quarters, EPS growth will be led by tech-related sectors, with communication services (+22% YoY) and info tech (+16% YoY) expected to deliver the best earnings growth. While mega-cap earnings (MAGMAN*) should slow from the recent ascent, earnings growth should remain robust at a 30% YoY pace! The key difference this quarter: the rest of the Index outside MAGMAN will start to contribute to S&P 500 earnings growth. In fact, S&P 500 ex-MAGMAN earnings growth is expected to be ~6.5% YoY – thanks to a positive reversal in healthcare and energy earnings. This will be the highest earnings growth for S&P 500 ex-MAGMAN since 3Q22. More important, their earnings are expected to accelerate through year-end, closing the gap with MAGMAN’s earnings growth—a key reason why we expect a broadening of performance beyond mega-cap tech going forward.

- Higher bar for earnings could lead to volatility | In the 12 weeks leading up to the 2Q24 earnings season, S&P 500 earnings were revised down only 0.1% – marking the second smallest downward revision in 11 quarters and well below the previous 10- year average decline of 3.5%. This set up will make it more challenging for companies to solidly beat their earnings forecast. The higher earnings bar could drive up volatility, particularly with valuations at current levels. For companies who do not beat or guide higher, they are more likely to see their stock price punished given the market’s lofty expectations. However, with the S&P 500 only experiencing one 5% pullback this year (typically 3-4 5% pullbacks occur in any given year) and the 2nd smallest intra- year drawdown (5%) over the last 25 years, any earnings misses could spark a near-term pullback.