Navigating Public and Private Credit Markets: Liquidity, Risk, and Return Potential

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits- Public markets offer potentially healthy opportunities for excess returns (alpha) given structural inefficiencies and macroeconomic volatility driven by divergent global growth and inflation paths. Public fixed income liquidity remains robust, aided by innovations like ETFs and portfolio trading.

- Less-liquid investments like private markets should offer an excess premium – which we estimate to be about 200 basis points – to compensate investors for potential lost alpha from active management in public fixed income, opportunity costs associated with the inability to rebalance, and potential costs of cash shortfalls for unexpected liquidity needs.

- Liquidity premiums have compressed in both public and private credit markets, with lower-quality segments of each facing elevated vulnerability to economic slowdowns and higher interest rates. Public markets offer opportunities to pivot to more attractive sectors.

- Asset selection matters. Following significant repricing in rates globally, we see tremendous value today in high quality, liquid public fixed income – which can offer attractive yields and serve as a hedge against risk assets – as well as in select private investments in less trafficked areas such as asset-based lending and opportunistic financing.

Public and private credit markets can both offer attractive investment opportunities that reward careful analysis across regions, sectors, and securities. As an active daily participant in both of these markets, PIMCO observes that there are key structural differences between them as well as significant sources of relative value differentiation today.

Two concepts central to comparing these markets are liquidity and alpha. Liquidity measures how easily financial assets can be bought or sold without severe price changes. Alpha refers to the opportunity for excess investment returns beyond the performance of the broader market.

Public fixed income markets tend to offer real-time liquidity to investors. This allows investors to shift from areas where liquidity premium and risk premium have compressed to areas that remain attractive – in other words, to pursue active alpha opportunities instead of applying a buy-and-hold approach (learn more in our recent video, “High Quality Credit Opportunities”). Additionally, public markets have become ripe for alpha given today’s environment of elevated macroeconomic volatility, heightened geopolitical risks, and diverging global growth and inflation trajectories.

When investing in private markets, investors give up near-term liquidity in an effort to capture a liquidity premium over a longer horizon. Additionally, segments of private markets offer superior documentation through the sponsor-lender relationship, or structural seniority through asset coverage, that can limit downside risk if credit deteriorates.

Based on the significant deal flow we are seeing across markets, we also observe that the liquidity premium in many areas of private markets has tightened to unattractive levels – as it has in certain areas of public markets. We are also seeing deterioration in covenants that traditionally protected lenders in private credit markets.

Investors should consider changes in valuations and market structure across private and public fixed income markets in recent years while making allocation decisions.

Gauging public credit liquidity

Liquidity depends on the number of available buyers and sellers, trade size and frequency, and information transparency and accessibility. Liquid markets better reflect fundamental asset values and facilitate price discovery. They allow investors to react quickly to new information by easily trading in and out of assets. That can enhance the opportunity for alpha through active adjustment based on incoming information and changes in valuations.

To be sure, some traditional measures indicate that public bond market liquidity has diminished. For example, there has been a reduction in the supply of bonds held by primary dealers, which historically have served as market makers. Recently, we’ve heard arguments – often pointing to these lower primary dealer inventories – that liquidity in public corporate credit markets has evaporated, particularly outside of the largest issuers.

However, we believe equating dealer balance sheet size with public fixed income market liquidity is inaccurate. This is because the primary dealer relationship has become less essential in the wake of technological advances such as exchange-traded funds (ETFs), all-to-all trading (in which any market participant can trade directly with another without going through a primary dealer), and portfolio trading.

For example, portfolio trading allows buying and selling of a basket of bonds in a single transaction. It is designed to improve execution and reduce costs. Dealers can hedge these trades in the deep and liquid ETF market, where ETF market makers serve as additional liquidity providers.

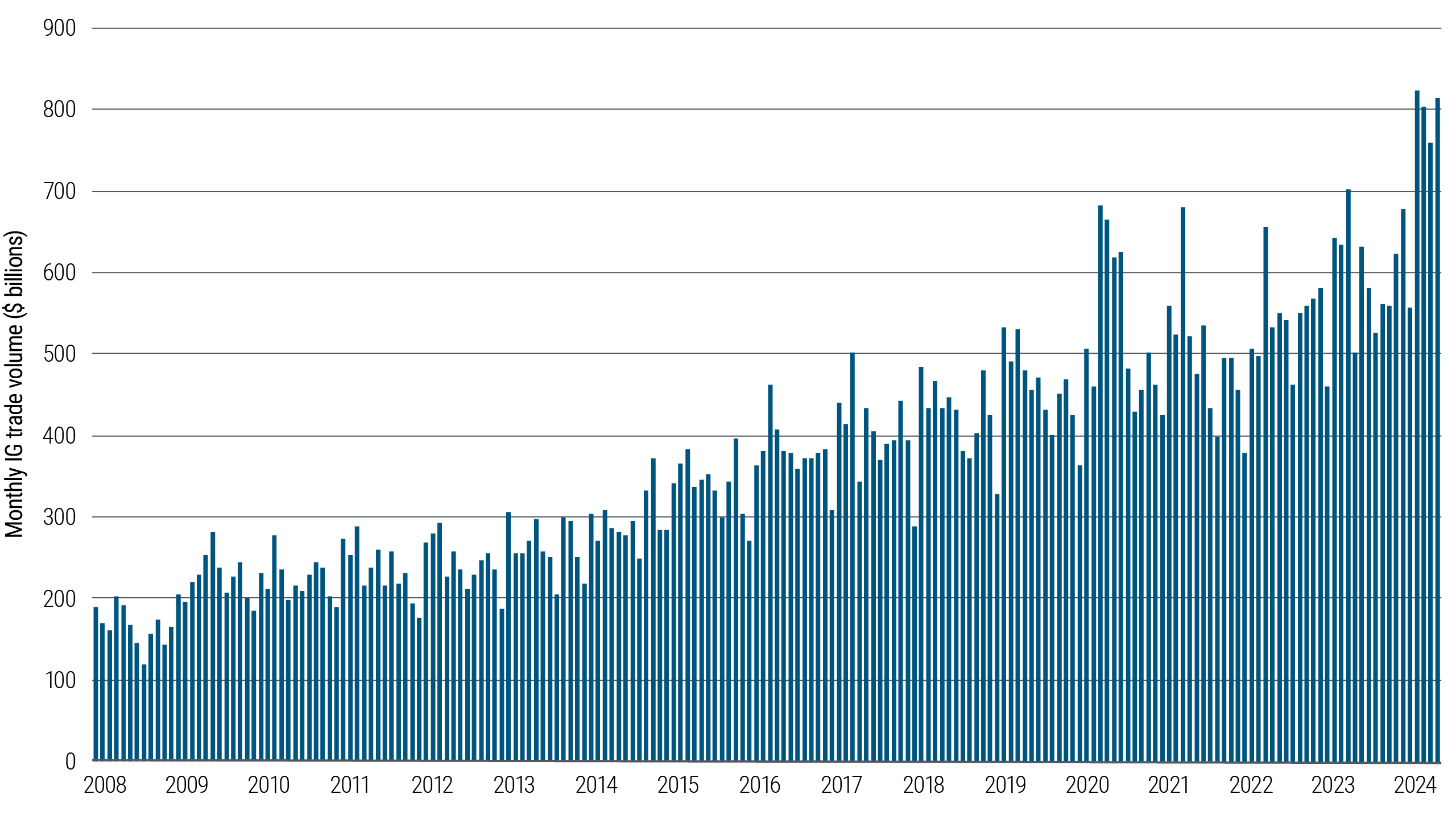

Trade volumes also indicate liquidity is abundant in high quality public credit markets (see Figure 1).

Ongoing innovation in technology and product design should continue to support liquidity and increase trading volumes in public markets, in our view.

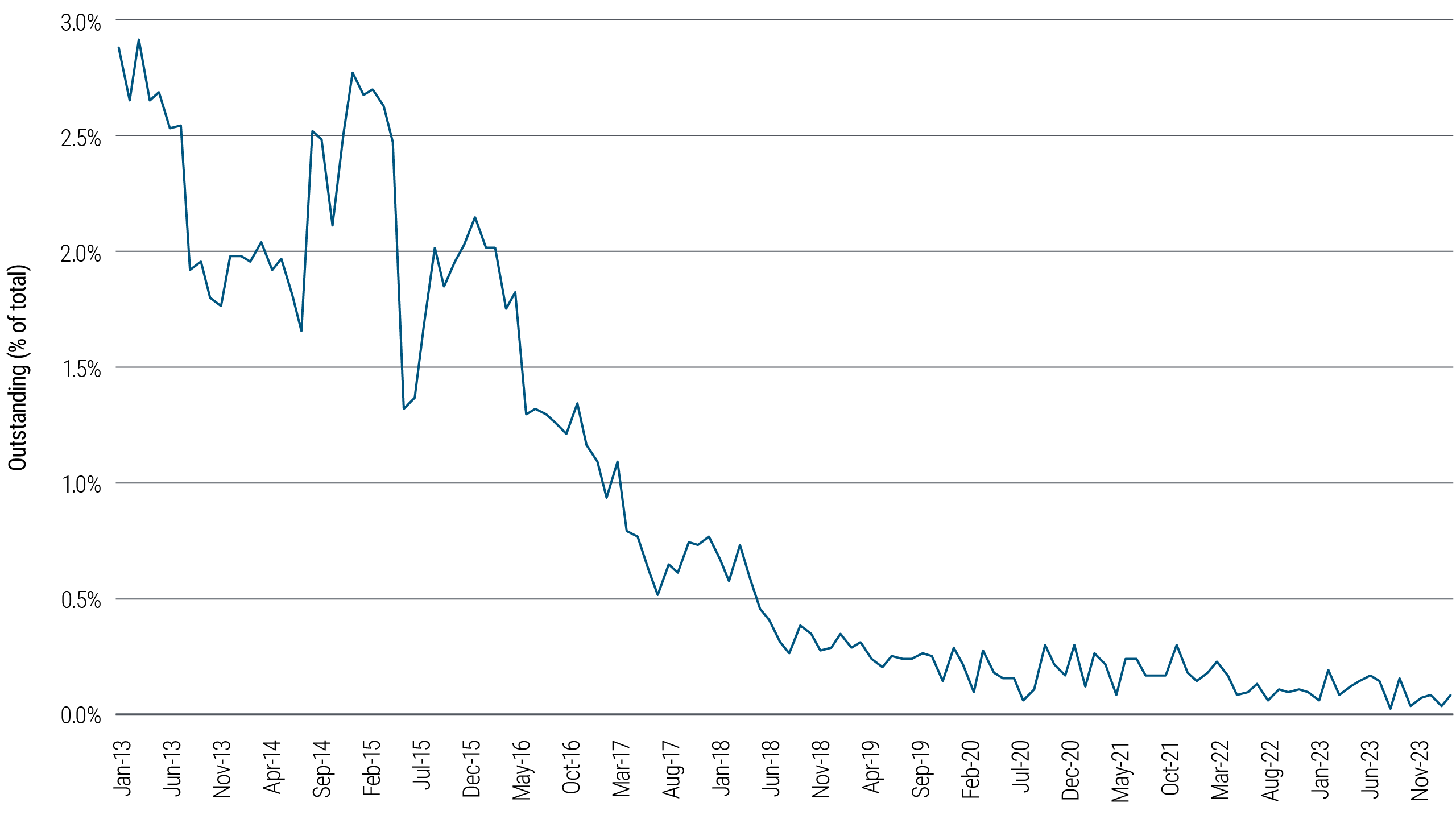

Average daily trading activity for U.S. dollar investment grade (IG) bonds in 2024 is $34.8 billion as of 25 June, according to J.P. Morgan. As shown in Figure 2, only a small percentage of IG bonds don’t trade each month.

Source: Barclays as of 1 December 2023

Weighing opportunity costs, alpha, and liquidity premium

When moving from public into private markets, investors typically give up some liquidity in pursuit of long-term returns. It’s important to assess the potential gains versus some inherent risks.

By locking up capital in private assets, an investor forgoes active opportunities to trade that capital. Alpha often comes from trades arising out of market dispersion or buying undervalued assets. The cost of providing liquidity is the net present value of these missed opportunities. Relatedly, illiquid portfolios can’t easily be rebalanced after a sell-off or a rally.

Adding illiquid assets also increases the risk of not having enough liquid assets for spending needs. A liquidity premium is needed to offset the expense of protecting the portfolio against this risk.

Based on these risks and associated costs, we estimate long-term illiquidity costs to be around 200 basis points (bps) a year. That includes the cost of lost alpha from active management of fixed income portfolios, the cost of the inability to rebalance portfolios, and the cost of liquidity shortfalls for unexpected liquidity needs.

Meanwhile, the compensation for providing liquidity is declining across both public and private credit markets as more capital chases too few opportunities. New investments are entering at potentially unattractive valuations, with corporate spreads across public and private credit markets near record lows.

In public corporate credit, liquidity premiums and risk premiums have declined to what we would consider less attractive levels. As a result, we have shifted our active public fixed income strategies to areas that we believe offer healthy liquidity and risk premiums, such as agency mortgages and senior structured products. Such ongoing active adjustment has the potential to lead to superior returns than would be expected based on initial spread.

Similar to the tightening that has occurred in public investment grade spreads, the liquidity premium in investment grade segments of private credit markets has tightened to less than 100 bps. We believe that level is insufficient relative to the opportunity costs associated with rebalancing, lost alpha from public fixed income, and potential costs of cash shortfalls.

Additionally, many private investment grade issuers are also able to access more liquid public fixed income markets and thus are only willing to pay a small additional spread to borrow capital in private markets for certain capital structure nuances that affect credit quality. Adjusting for credit quality differences between public and private investment grade issuers, the excess spread of less than 100 bps becomes even less attractive.

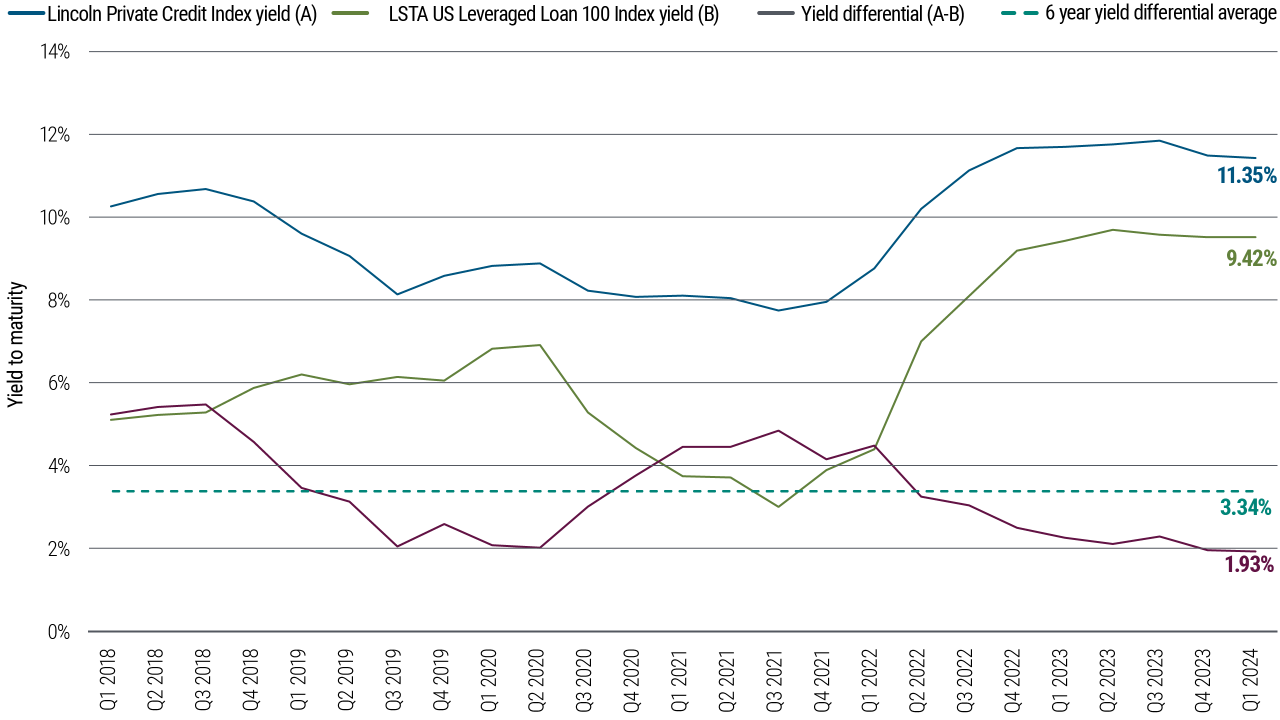

When we shift beyond investment grade and compare the broadly syndicated loan market versus private corporate credit (middle market direct lending investments), we observe something similar. The spread premium for private corporate direct lending relative to broadly syndicated loans has tightened from about 400 bps three years ago to 193 bps in 2024 (see Figure 3), according to PIMCO calculations based on Lincoln and LSTA data.

Source: Lincoln International, LSTA as of 31 March 2024. Past performance is not a guarantee or a reliable indicator of future results. It is not possible to invest directly in an unmanaged index. The Lincoln Private Credit Index tracks the fair market value of 1,600 middle market, direct lending credit investments. The LSTA US Leveraged Loan 100 Index measures the market-weighted performance of the largest institutional leveraged loans based on market weightings, spreads, and interest payments.

Weighing the shrinking liquidity premium against the associated costs to provide that liquidity suggests that investors today are receiving inadequate compensation for locking up capital in certain private credit areas, particularly those where incentives are to raise capital and deploy funds immediately.

Credit quality differs across public and private markets

Investors should also take into account the differences in average credit quality between public and private credit markets:

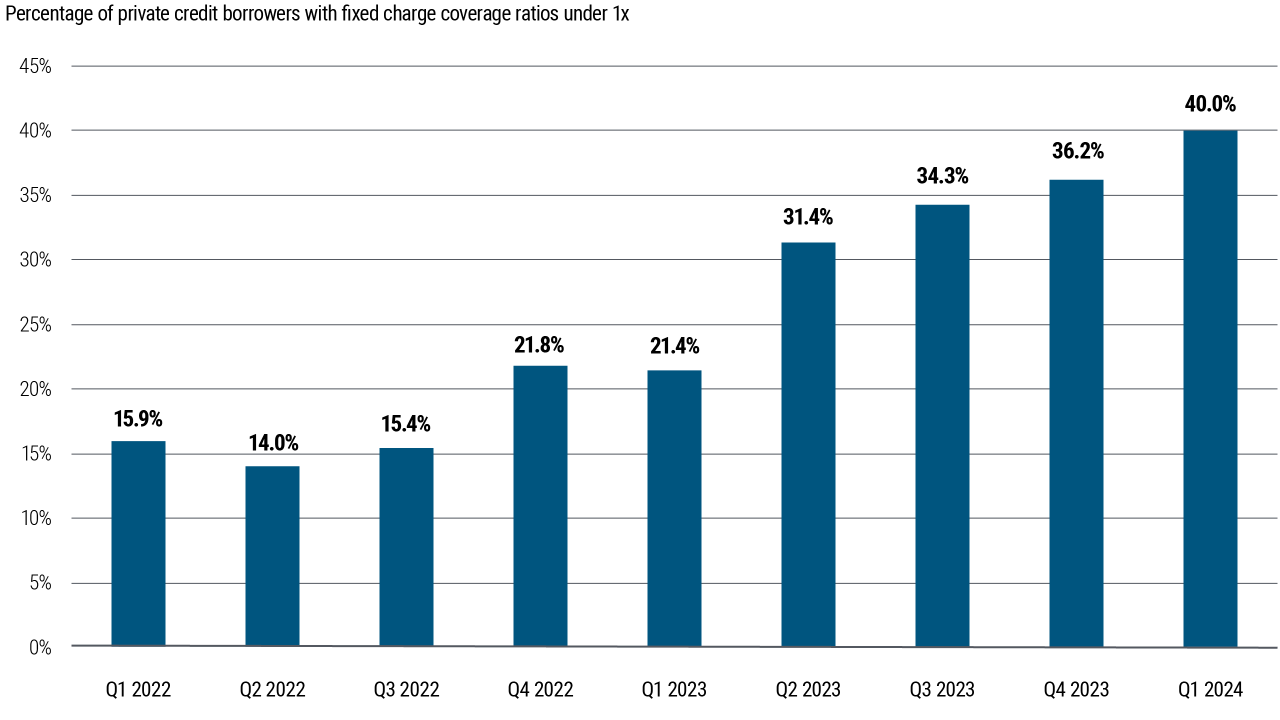

- Credit quality and free cash flow generation: Private corporate credit is heavily concentrated in sectors such as technology and health services, which are susceptible to AI disruption and changing business conditions (for more, see our latest Secular Outlook, “Yield Advantage”). These are typically smaller, leveraged companies financed with floating-rate debt, making them vulnerable to sustained high interest rates, economic slowdowns, defaults, and lower recoveries. Higher interest rates have started to affect interest coverage ratios (how well earnings cover concurrent interest payment expenses) for private companies much more than in public markets. The percentage of private corporate direct lending borrowers with fixed charge coverage ratios below 1x has risen from 15.9% two years ago to 40% this year (see Figure 4). This means 40% of private credit borrowers (size weighted) are not producing enough cash flow to service all debt, taxes, and capital spending needs. If interest rates stay elevated for longer or economic growth slows, these borrowers would be more vulnerable to further increases in leverage, declining credit quality, and higher expected losses. Such a credit cycle would likely create attractive opportunities to provide new financing with preferable terms to new investors.

Source: Lincoln International as of 31 March 2024. Fixed charge coverage ratio (FCCR) = (LTM EBITDA - Taxes - Capex) / (Interest Expense + (1% * Total Debt)). Capital expenditures (“Capex”) utilizes LTM Capex by default. If LTM Capex is not available, NFY Capex is utilized, and LFY Capex if both LTM Capex and NFY Capex are unavailable.

- Private equity dynamics: Private equity owners are experiencing longer hold periods and valuation pressures due to the sharp rise in base rates, which has diminished their willingness and ability to support portfolio companies. Furthermore, the influx of new entrants into the space has weakened the importance of the sponsor-lender relationship and led to a deterioration in private credit documentation.

- Market shifts and innovations: Many higher-quality companies have been moving back to public markets, leaving private credit portfolios with selection bias issues. Private credit innovations like synthetic payment-in-kind (PIK) structures – which allow interest payments to come from other borrowings – may merely mask borrower stress as higher rates pressure free cash flow in older investments.

Balancing the risks and costs against potential investment returns within private markets more broadly, we see many attractive options for investors who can manage around illiquidity – but careful selection within sectors and companies is key (learn more in our recent video, “Unlocking the Power of Private Credit”).

Conclusion

PIMCO’s global platform spans public and private markets, and we are constantly seeking relative value opportunities among asset classes, sectors, and regions. Not all areas of public fixed income or private credit markets will be permanently attractive or unattractive. There will always be opportunities across different segments of both markets. Investment decisions should reflect the most up-to-date valuations and quality assessment across the entire opportunity set.

Based on current relative valuations and market conditions, we strongly believe there is tremendous value in high quality, liquid public fixed income. Starting yields look very attractive when compared with most alternatives across the risk and liquidity spectrum.

With inflation falling toward central banks’ targets, high quality fixed income may also offer an attractive, liquid hedge to risk assets. Additionally, private investments in less trafficked areas – such as asset-based lending and opportunistic financing – that have adequate liquidity compensation, superior credit quality, and strong asset protection may offer attractive value to investors.

Disclosures

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Alternatives involve a high degree of risk and prospective investors are advised that these strategies are appropriate only for persons of adequate financial means who have no need for liquidity with respect to their investment and who can bear the economic risk, including the possible complete loss, of their investment. Private credit involves an investment in non-publically traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2024-0620-3656879

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All