Five Dynamics That Could Drive the Financial Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOriginally published May 24, 2024

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Inflation should resume its downward trend

- Positive earnings streak should continue

- Expect some election volatility this summer

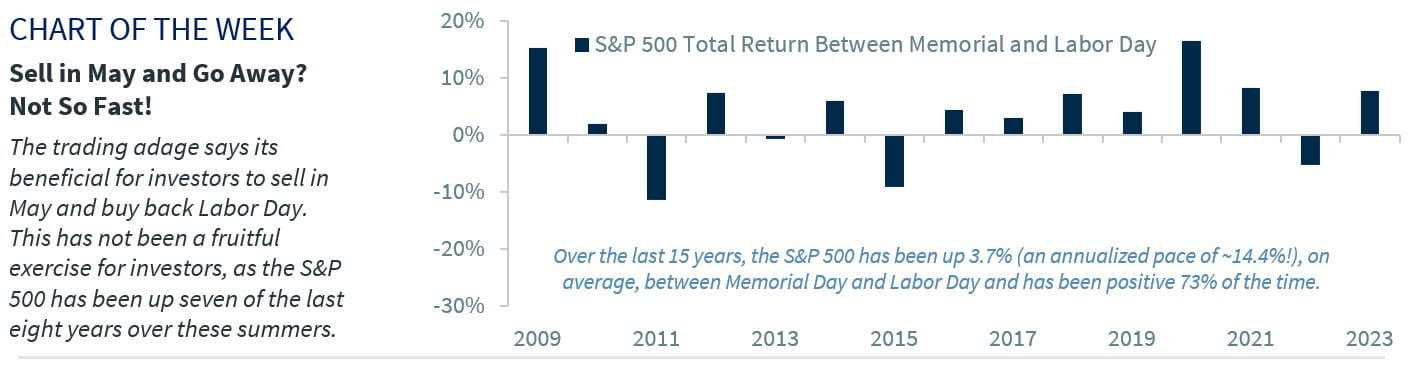

While Memorial Day ushers in a fun-filled weekend of festivities, family picnics and barbeques with friends – we must always remember to honor all the men and women who valiantly served and made the ultimate sacrifice for our country to defend our freedoms. We salute you. And with the summer season unofficially kicking off this weekend, be safe wherever your travels may take you. In fact, this Memorial Day is expected to draw a near record number of travelers, with AAA projecting ~44 million people traveling this holiday weekend – that’s a 4% increase from last year and the second highest number in ~20 years! As we set our sights on the summer, here are five dynamics that could drive the financial markets between Memorial Day and Labor Day:

-

The data dependent Fed | Fed fund forecasts have swung wildly, moving from six 25 bp rate cuts at the start of the year to just 35 bps of easing (one to two cuts) today. The sharp repricing has been driven by sticky inflation and the economy’s resilience.

- June 11-12 FOMC meeting—while no rate changes are expected, an updated dot plot and economic forecasts will be presented. Does the Fed still see a steady decline in rates? Do cuts start this year? How fluid are its economic forecasts?

- July 30-31 FOMC meeting—earliest meeting the Fed could potentially cut rates. While many believe the Fed will wait until September, it is premature to overlook July. While the window for a July cut is small, keep in mind we still get 3 PCE, 2 CPI, and 2 payroll readings before that meeting. If these readings suggest cooling inflation and job market, combined with continued corporate rhetoric of a slowing consumer, this meeting could be a chance for the Fed to take an ‘insurance’ cut.

- Inflation should resume its downward trend | While the April inflation report moved in the right direction after a string of hotter than expected inflation reports, there are still lingering concerns about the persistence of inflation.

- Core inflation likely to decelerate—Why? Because rent inflation should slow as asking rents normalize following the pandemic housing boom. In fact, Redfin reported that some areas that saw the biggest booms (Austin, Nashville, Tampa) are seeing the steepest drops in rents over the last year. Given the lags in this data, further disinflation is likely in the pipeline.

- Consumers pushing back on price increases—companies like Walmart and Target are reducing prices on everyday items to lure customers back into the stores. Fast food and casual restaurants are rolling out value meals to cater to budget-strapped consumers. These disinflationary tailwinds should persist over the summer in both goods and services prices.

-

Positive earnings streak to continue | Earnings have been better than expected thus far this year as 2024 S&P 500 earnings have been stable (current consensus: $243) and have not exhibited the typical downward revision trend.

- 2Q24 earnings season—believe it or not, it is just seven weeks away with the big banks reporting in early July. Earnings growth is expected to be positive (~10% YoY) for the fourth consecutive quarter, led by Comm. Services and Health Care.

- Mega-cap tech—likely to remain strong once again, with MAGMAN expected to see ~29% YoY earnings growth.

- Broadening of EPS growth—after the Index ex-MAGMAN (i.e., the other 494 companies) notched its first quarter of positive growth since 4Q22, earnings for this group are expected to accelerate to ~7% YoY, signaling the broadening of earnings.

- Earnings need to deliver—while economic activity is expected to moderate, earnings growth will have to remain robust and trend higher to support the already elevated P/E multiple (which is in its 92nd percentile over the last 30 years).

-

Expect some election volatility | Volatility tends to pick up during the summer in election years. A few potential drivers:

- Former President Trump’s NY legal case—will go to the jury next week with a conviction potentially hampering some of his support versus an acquittal (or hung jury) potentially solidifying his support.

- Presidential debate(s)—the first debate (on June 27) is the first debate ever held before both parties’ conventions. The second debate is not until September 10. Market topics of importance: the economy, inflation, tariffs, taxes, and regulations.

- Political conventions—the Republican National Convention (in Milwaukee) is July 15-18 while the Democratic National Convention (in Chicago) is August 19-22. Prior to the GOP National Convention, President Trump will select his VP candidate.

-

AI trends in focus | Evidenced by the attention to developer conferences from OpenAI, Alphabet and Microsoft over the last few weeks, investors remain keenly focused on AI and its continued development.

- Apple’s worldwide developers conference—the second largest company in the S&P 500 will host its conference June 10-14 where it is expected to reveal its plans within the AI space. This should continue to drive investment within AI and be a tailwind for earnings. However, with lofty expectations for the industry growing, any disappointments will lead to volatility.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

A message from Advisor Perspectives and VettaFi: Dive into alternative investment opportunities at our upcoming Alternatives Symposium on May 30, and gain insights into diversifying portfolios beyond traditional equities and fixed income.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All