The International Monetary Fund (IMF) publishes a wealth of information during its spring meetings, which took place earlier this month in Washington. The lion’s share of attention goes to the World Economic Outlook, the release of which is marketed heavily.

By contrast, the IMF’s Fiscal Monitor is low-key. But the most recent edition was worth reading. It focused, in part, on the increasing application of industrial policy around the world. This trend will have important consequences for growth, inflation and debt.

In classical economics, an “invisible hand” steers resources to their best use. Capital and labor migrate naturally to industries and occupations where opportunities are the best. Any attempt to interfere in the process creates “wedges,” areas of inefficiency which are costly to societies. Nonetheless, all governments engage in some steering of their economies.

The degree of government intervention in markets has escalated substantially since the pandemic. Centrally-directed efforts were critical to dealing with COVID-19: subsidies for medical research, testing and vaccination were essential to corralling the virus. Developments in this space might certainly have progressed naturally without Federal direction, but coordination proved much better than competition in speeding response.

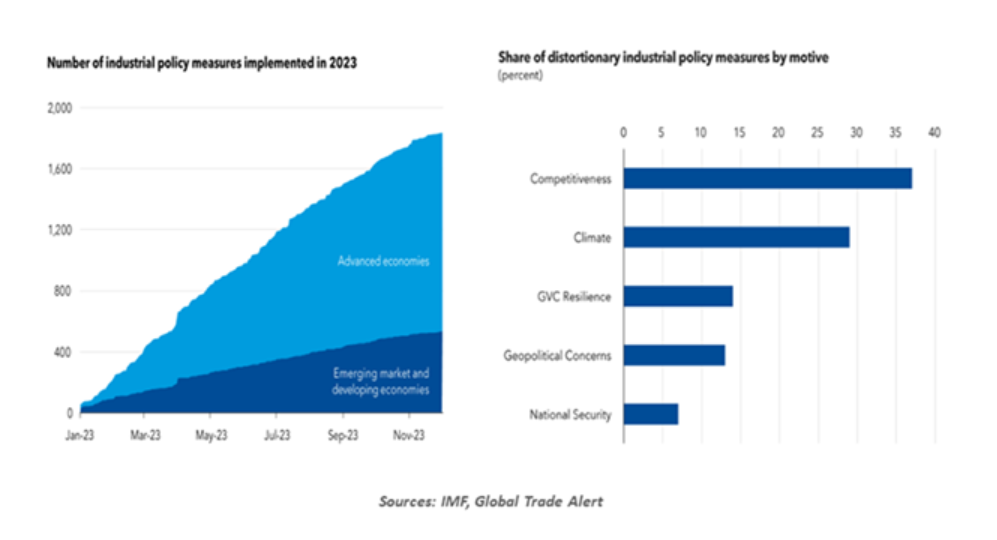

The post-pandemic era has provided new openings for the broader application of industrial policy. Problems with far-away supply chains prompted a desire for more proximate options. Increasing stress between Beijing and the West has prompted the latter to reduce reliance on China. Governments have become heavily involved in “re-shoring” efforts.

Security has become more tenuous in the wake of wars in Ukraine and the Middle East. This has always been an area where government involvement is common, even desired. Policy support for the defense sector is increasing, and advancing investment in microchip fabrication has strategic as well as civilian foundations.

Finally, industrial policy may be justified on the basis of competitiveness. If trading partners are supporting key industries, then nations feel more justified in responding. China’s state-sponsorship of key sectors is the most substantial example of this, but not the only one. Creating national champions as opposed to trusting external channels seems to be the order of the day.

However sensible all of these initiatives may seem, they have increased fragmentation between countries. Battles over subsidies and sponsorship have become common; reversing anti-competitive behavior is difficult, given the challenges facing the World Trade Organization. The result is an industrial arms race that will almost certainly result in global overcapacity. Smaller economies are at a disadvantage to larger ones in promoting their industries, narrowing their paths to development and making it more difficult for them to handle their debts.

GOVERNMENT DIRECTION OF ECONOMIES SHOULD BE VIEWED WITH APPREHENSION.

Further, the execution of industrial policy invites a host of potential hazards. Governments may not be the ideal agents to determine which sectors are worthy of special emphasis; dulling the influence of markets in directing capital risks inefficient allocations. Even if sector selection is prescient, identifying the “winning” providers is not easy. Government involvement invites politics into the process, which may not be aligned with maximizing efficiency. This can be an especially powerful distortion during election years.

Governments rarely get the full returns on their investment in industrial policy. The public provides capital through the national budgeting process, but the rewards for success (if achieved) accrue primarily to the private sector. Tax regimes rarely return sufficient revenue to defray costs, leaving budget deficits enlarged.

Debate over industrial policy is active in both academic and political circles. Some studies hail its benefits, while others illustrate substantial downsides. Only one thing is clear: countries are looking out for themselves more than they used to, which weakens the global order. And that has both economic and diplomatic costs.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust