Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Over optimism flagged near-term pullback

- Volatility is a normal feature of long-term investing

- Pockets of weakness are not overly concerning

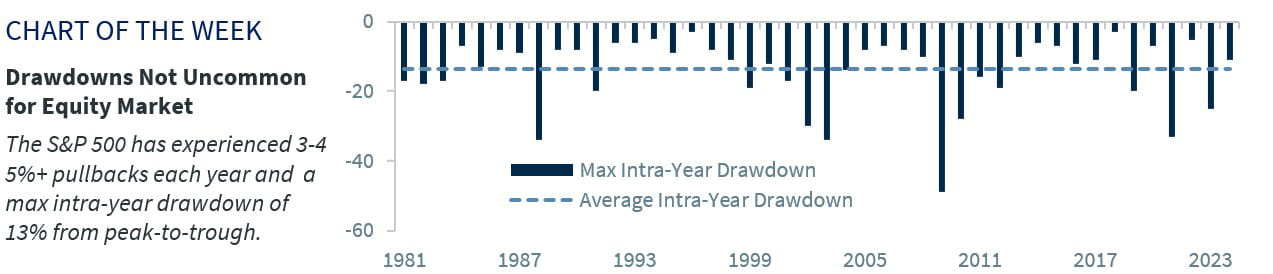

Keep Calm and Carry On! The recent burst of volatility after a prolonged period of calm has captured the market’s attention and temporarily halted the S&P 500’s recent winning streak. While market gyrations can be concerning, remember not to panic – pullbacks and interim spikes in volatility are quite common. Below we put the recent market movements in perspective, which have been driven by time (it has been a while since we had a 5%+ pullback), overly optimistic, complacent market sentiment, and higher Treasury yields amid persistent inflationary pressures and signs of a more patient Fed. However, we reiterate our positive long-term view and suggest using periods of weakness opportunistically.

Bottom line | The biggest question on investors’ minds is whether the current drawdown is normal or the start of something more severe (i.e., a bear market)? Our answer: given we have been calling for a pullback, this is likely a consolidation phase to digest the recent gains and not the end of this bull market. But how much further downside can be expected? Well, given the historical average drawdown has been ~14% a year, further downside cannot be ruled out. One area of support – although this is unlikely as uber optimism has already begun to wane – would be the 200-day moving average (~4,670), which reflects 10% downside from recent highs or an additional 5% from current levels. However, even if this were to occur, it would not change our long-term positive equity view as corporate fundamentals remain on solid footing and earnings are trending upwards. While interest rates have moved higher, it is for the right reason—stronger economic growth. Stronger economic growth leads to upside for corporate earnings—the indicator with the strongest predictive power for future equity returns. As a result, we reiterate our year-end S&P 500 target of 5,200 and would use periods of weakness to add to our favorite areas of the market—Info Tech, Industrials, Health Care, and Energy.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Raymond James

Read more commentaries by Raymond James