Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

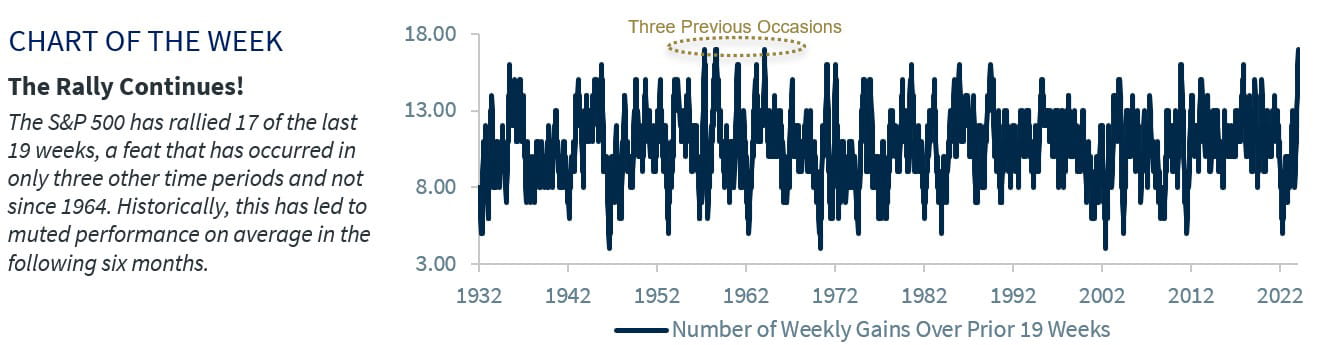

- Strong rally suggests muted gains going forward

- Elevated valuations suggest market priced to perfection

- Investor sentiment becoming increasingly optimistic

Don’t forget to turn your clocks forward early Sunday morning! That’s right, this weekend most of the nation (except Arizona and Hawaii) will follow the twice a year ritual of adjusting the clocks forward or backward. The second Sunday in March, when we 'spring forward,' is always bittersweet. The good news: we add an extra hour of sunlight to our days. The bad news: we lose an hour of sleep. And speaking of daylight savings time, our view on the equity market follows similar patterns – where we expect a short-term 'fall back' after the market’s recent gains but remain optimistic that equities can 'spring forward' over the long term given the market’s solid fundamental underpinnings. Here are reasons the equity market is vulnerable to a near-term pullback, but should move higher over the next 12 months:

- Strong rally suggests muted forward gains | The move higher in the S&P 500 has been historic. In fact, the S&P 500 has climbed ~17% over the last four months and is on pace to rally 17 of the last 19 weeks. A run of this magnitude has only occurred three other times in history and not since 1964. Historically, when a rally of this duration has taken place, it has led to more muted forward performance as the S&P 500 was flat on average in the following six months. This suggests that the market may see a period of consolidation or a pullback in the near term as it looks to digest these gains. This would be consistent with history, as the S&P 500 has seen 90 trading days without a 5% pullback, nearly 2x times the historical average. And remember, the S&P 500 typically experiences 3-4 pullbacks of 5% or more, on average, each year, so a pullback would not only be normal, but healthy for the market. While near-term caution is warranted, we would use pullbacks as opportunities to add to positioning as the bull market is still in its infancy – currently 1.4 years versus an average duration of 5.5 years.

- Elevated valuations pose a near-term risk | The recent run-up in stock prices has pushed valuations to elevated levels. In fact, on a trailing twelve-month basis, the S&P 500’s price-earnings ratio has climbed to 23.0x – its highest level since 2002 (ex-COVID). Enthusiasm around AI and the mega-cap names have been the main drivers behind the move. With the S&P 500’s valuations trading in the 92nd percentile, the market is priced to perfection. The problem: any hint of disappointing news (whether macro or earnings related) could lead to a negative reaction. Case in point: news headlines this week around Apple’s China sales plunging 24% in the first six weeks of the year. Not only did the news weigh on Apple’s stock price, but it also dragged the S&P 500’s Info Tech sector down 2.2% on the day – a prime example of what can happen when optimism meets disappointment. And while the market’s top-heavy names can cause price swings in the overall Index, we expect the broader market to participate in the months ahead as the overall macro backdrop remains positive.

- Investor sentiment is optimistic | With the S&P 500 notching its 18th record high for the year, investors have become increasingly optimistic this year. The relentless rally and stronger than expected economic data over the last few months has caused many Wall Street strategists to ratchet up their S&P 500 targets for the year – which is ironically the mirror opposite of the set-up at the start of 2023 when most Wall Street analysts were expecting a down year. In fact, the bears (i.e., those who think the stock market is going to fall) have gone into hibernation, at least according to the latest AAII sentiment survey. While investor sentiment is just below its recent maximum bullishness, bearish sentiment is extremely low (21.3%) relative to the past historical patterns. The overwhelming positive sentiment on stocks has carried over to consumers too. The latest Conference Board report revealed that consumers are the most optimistic on the stock market since February 2020. And from a contrarian standpoint, we are taking note. With these sentiment indicators moving more toward extreme bullishness, a near-term consolidation seems likely. However, over the longer term, fundamentals (such as earnings which are improving) should win out.