Breaking a mirror, walking under a ladder, and a black cat crossing your path have all been seen as bad omens. Another one is Friday the 13th, which happens to be when the big banks will kick off earnings season. So, should we fear what’s in store?

The truth is, even as market prices have fallen over the past several weeks, earnings estimates for the year ahead have continued to rise. You could view this dynamic in two ways: (1) that the analysts have confidence in the companies they are following or (2) that the bar has been raised for these companies to try to beat these earnings estimates. I tend to fall in the camp that it’s easier to jump over the small bar, so things will be getting tougher. The good news is the bar for the third quarter remains low, with the S&P 500 expected to see a 0.3 percent decline in earnings year-over-year.

Let’s take a peek behind the curtain.

Scary Expectations?

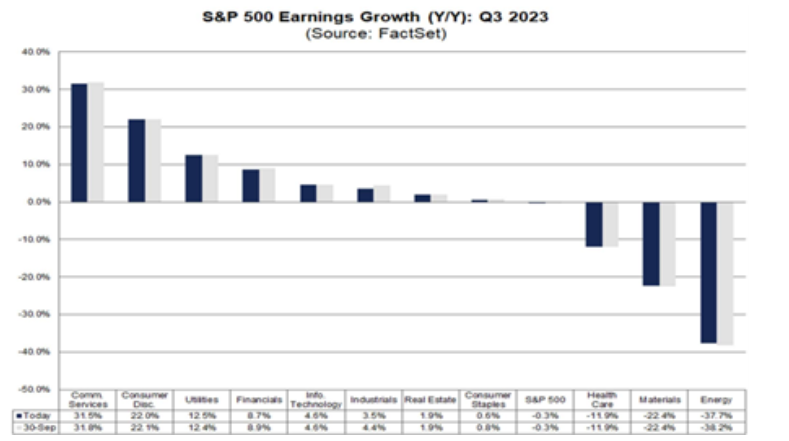

When we look at the drivers of earnings in the third quarter, there are some significant differences in the sectors that are expected to see gains and losses. Despite the expectation for the third straight quarter of year-over-year earnings losses, 8 of 11 sectors in the S&P 500 are expected to see earnings growth this quarter, while 9 of 11 are expected to see revenue gains (see chart below).

Energy and materials are anticipated to see significant earnings declines, as commodity prices have fallen significantly from a year ago despite the rise in oil prices that has occurred more recently. If energy were excluded from the index, the S&P 500 would be expected to see 4.9 percent growth in earnings. If energy prices hold around these levels, it could be supportive of earnings going forward, although higher energy prices could weigh on other sectors.

On the other end of the spectrum, communication services, consumer discretionary, and utilities are all expected to show double-digit gains in earnings. Within communication services, Meta could have a major impact, with earnings expected to more than double from last year. Wireless telecom companies are also expected to see a recovery, with T-Mobile earnings expected to see a 450 percent rise over last Q3. Amazon will be the largest driver of earnings increases in consumer discretionary, while hotels, restaurants, and leisure are still experiencing a strong recovery, with an expected 92 percent growth in earnings.

The “magnificent seven” (i.e., Apple, Microsoft, Amazon, Alphabet, Nvidia, Meta, and Tesla), which have been driving returns this year and are dominated by tech names, will still have a major impact on the earnings season. But the tech sector as a whole is expected to see middling growth in earnings at 4.4 percent, despite the fact that tech firms are valued at a 36 percent premium to their 20-year average.

Look into the Crystal Ball

With interest rates rising, the job market remaining tight, and inflation continuing to cool, it will become more difficult for companies to pass on cost increases to consumers. At some point, every price increase can’t be blamed on inflation, and consumers will look for cheaper alternatives as budgets become stressed.

I’ll be paying close attention to profit margins in the third quarter and beyond. Net profit margins are expected to fall from 11.9 percent a year ago to 11.7 percent in the third quarter. Whether companies can maintain high margins will be key in supporting the 8.2 percent earnings growth expected in the fourth quarter and the 12.2 percent growth expected in 2024. These come with revenue growth expectations of only 4.6 percent in the fourth quarter and 5.5 percent in 2024.

While companies may be able to beat the easy expectations for the third quarter, the guidance they provide for the future will be key to supporting S&P 500 valuations, which are still slightly above their long-term averages.

Danger Ahead?

Overall, we might be in store for some spooky occurrences this October. But the Q3 earnings season shouldn’t be much to fear—just be sure to look out for the signs of what’s to come.

Disclosure

The information on this website is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets.

The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. All indices are unmanaged and investors cannot invest directly in an index.

The MSCI EAFE (Europe, Australia, Far East) Index is a free float‐adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. and Canada. The MSCI EAFE Index consists of 21 developed market country indices.

One basis point (bp) is equal to 1/100th of 1 percent, or 0.01 percent.

Third-party links are provided to you as a courtesy. We make no representation as to the completeness or accuracy of information provided on these websites. Information on such sites, including third-party links contained within, should not be construed as an endorsement or adoption by Commonwealth of any kind. You should consult with a financial advisor regarding your specific situation.

Member FINRA, SIPC

Please review our Terms of Use.

Commonwealth Financial Network®

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Commonwealth Financial Network

Read more commentaries by Commonwealth Financial Network