Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Growth boost is likely to prove short-lived

- Weaker growth will drive Treasury yields lower

- Still cautious on equities near term

Happy Labor Day! This weekend marks the ‘unofficial end’ to summer – the last weekend to squeeze in another summer getaway! And there has been no shortage of summer excursions as this marked the second consecutive year of blockbuster summer travel. While many of us were having fun in the sun, the economy and markets, unfortunately, did not take a vacation. And there was plenty that happened this summer – from travel and leisure boosting growth to the S&P 500 defying performance myths to the bond market dealing with another U.S. credit downgrade. As investors prepare for the stretch run to year end, we summarize the key events that occurred during the summer and give our latest thoughts as we move forward.

- Summer of revenge travel II temporarily boosts growth | The resilient consumer has kept the economy afloat. While consumers have gotten more discerning with their spending (as highlighted by a number of companies in their 2Q earnings calls), their insatiable demand for travel has not wavered. Just as we forecasted, the ‘Summer of Revenge Travel – Part II’ was on full display with TSA screenings at record levels, hotel occupancy back to pre-COVID levels, and the cruise industry experiencing a summertime boom. It wasn’t just travel either as other events such as movies (e.g., Barbie, Oppenheimer), concerts (e.g., Taylor Swift and Beyoncé) and sporting events (e.g., Messi) provided a strong one-time boost to economic activity. This resilient consumer spending has led the consensus to pull back its recession calls, with fewer than 50% expecting a recession in the next 12 months.

- Our view | We expect the summertime boost to growth to be short-lived as headwinds are building. With the summer travel season winding down, excess savings depleted, student loan payments restarting, job growth slowing, and higher borrowing costs (i.e., credit card, mortgage, auto loans) weighing on the consumer, it is likely consumer spending will become challenged. Our expectation of a small retrenchment in consumer spending should push the U.S. economy into a mild recession in 1Q24.

- Rising Treasury yields turns performance negative again | Despite the steady deceleration in inflation, bond yields climbed throughout the summer in response to stronger than expected economic data and Fitch’s U.S. debt-rating downgrade. In fact, the ~80 bps rise in the 10-year Treasury yield since the April 6 low has pushed its performance into negative territory for the second year in a row during the summer (defined as Memorial Day to Labor Day). This is the first time on record we have seen back-to-back declines during this period. Consensus sentiment on interest rates has also soured as the higher-for-longer narrative gains momentum with some analysts suggesting the 10-year Treasury bond yield will move to ~5% and stay there for a while.

- Our view | We disagree with the call for higher interest rates and believe the path forward for yields will be lower over the next 12 months, primarily driven by our expectation of a slowing economy, a further deceleration in inflation, and the Fed ending its tightening cycle soon. Hints of a slowdown in job growth (i.e., declining JOLTS job openings, downward revisions to payrolls), falling consumer confidence and depleted excess savings will likely cause a ‘growth scare’ by year end.

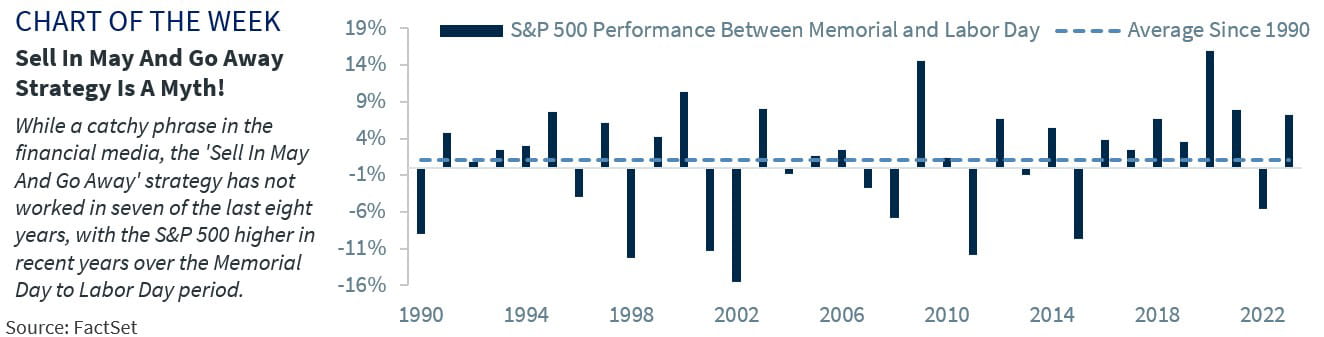

- Solid summer performance from the equity markets | The ‘Sell in May and Go Away’ myth proved to be just that – a myth. Stronger than expected economic data, slowing inflation and hopes that the Fed is nearing the end of its tightening cycle put the S&P 500 on track for a 7% gain this summer. This is the seventh time in the last eight years that the S&P 500 was higher during the summer (Memorial Day to Labor Day). In addition, the mega caps weren’t the only names driving the market higher as there was a broadening of performance. In fact, 10 of 11 sectors were in positive territory with select cyclicals, such as Energy, Consumer Discretionary and Industrials leading the way. Second quarter earnings were better than feared although the S&P 500 posted its third consecutive quarter of negative earnings growth. One bright spot: Positive corporate guidance saw earnings for 2023 and 2024 inflect higher which fundamentally supports recent gains. While volatility did increase throughout August, the S&P 500 narrowly avoided a 5% pullback. In fact, the -4.8% peak to trough decline this summer was just over half the typical summertime pullback (-8.5%). Consensus optimism continues to grow for the S&P 500 with many Wall Street strategists lifting their S&P 500 targets.

- Our view | While the S&P 500 delivered solid performance this summer, we remain cautious in the near term given the Index remains modestly above our year-end target of 4,400. In addition to September being the seasonally weakest month of the year, if the economy starts to weaken (as we expect), growth concerns could weigh on the earnings outlook and investor sentiment again. Despite our cautious near-term outlook, we remain optimistic longer term (S&P 500 12-month target: 4,600) as still solid corporate fundamentals, lower interest rates and a more accommodative Fed should provide solid underpinnings to the market.

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Raymond James

Read more commentaries by Raymond James