Whether Pause or Pivot, Look to Bonds

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsAn allocation to fixed income may help investors navigate a potential recession as well as uncertainty around the Federal Reserve’s policy trajectory.

EXECUTIVE SUMMARY

• In its effort to tame inflation, the U.S. Federal Reserve is likely to pause at the top of

its interest rate cycle rather than quickly pivot toward rate cuts. But in either scenario,

history suggests fixed income can offer attractive return potential, especially relative

to equities.

• We favor bonds for their diversification, capital preservation, and upside opportunities.

Starting yields appear competitive and we favor high-quality duration and liquid credit

exposures, as well as U.S. agency mortgage-backed securities.

• We believe the overall resilience seen in equity markets in 2023 would diminish in a

downturn. Earnings expectations appear too high, and valuations too rich. We are

underweight equities in multi-asset portfolios.

Through this year’s changing market narratives – soft landing, overheating, and credit crunch – the underlying macro conditions have pointed steadily toward the same fundamental theme: Bonds are back.

Elevated macro uncertainty, a likely economic downturn, and higher yields that bolster return potential all may support a shift in allocation toward fixed income. Restrictive monetary policies are affecting global economies after long and variable lags, credit is tightening, and signs of breakage have started to appear in the financial sector. PIMCO’s business cycle models forecast a recession in the U.S. later this year. How different asset classes will perform is likely to depend heavily on the severity of the recession (when or if it happens) and, crucially, on central bank behavior.

As credit tightening reduces the need for monetary tightening, we believe the U.S. Federal Reserve (Fed) is likely close to the end of its hiking cycle, and that it will keep interest rates high while the U.S. economy slips into recession. What does this mean for portfolios? Our analysis of historical returns across asset classes amid Fed policy shifts provides a useful framework for portfolio positioning over the next 12 months.

Over the cyclical horizon, we believe bonds will meaningfully outperform equities. Yet equity markets have remained resilient thus far this year even as the earnings outlook has deteriorated. In our view, earnings expectations for the second half of 2023 and 2024 are still too high, and equity valuations appear rich across every metric we track. This reinforces our stance that investors should aim to be underweight equities, seek quality, and take advantage of the diversification, capital preservation, and upside opportunities available in bonds.

Macro backdrop: Approaching the end of the hiking cycle

Several trends could reduce the need for more restrictive monetary policy to rein in inflation. Loan growth, which was already slowing prior to the collapse of Silicon Valley Bank, is poised to decelerate further. Lending standards are likely to tighten most at regional banks, disproportionately affecting small business activity. In turn, this could put downward pressure on job creation – nearly half of U.S. workers are employed by small businesses with fewer than 500 employees (source: U.S. Small Business Administration as of August 2022).

Additionally, a host of U.S. macro indicators are moderating, including retail sales, manufacturing production, and both services and manufacturing purchasing managers’ indices (PMIs). Indeed, the current business cycle seems to be unfolding in line with historical experience: Our analysis across 70 years in 14 developed markets indicates that increases in recession and unemployment have usually begun around 2 to 2.5 years after the start of a hiking cycle. (For more on this, read our latest Cyclical Outlook, Fractured Markets, Strong Bonds.”) The current hiking cycle began just over a year ago in March 2022, but the rapid pace and extent of subsequent hikes may increase the risk that recession and higher unemployment happen sooner than the historical average time frame.

Still, U.S. inflation remains well above the Fed’s target. A key question for asset allocators is whether the Fed will end this hiking cycle with a long pause at the top in order to subdue sticky inflation or pivot to an easing cycle this year to bolster growth amid tighter credit and greater disinflation. Asset classes could fare very differently under these two scenarios.

Long pause or quick pivot: Investment implications of early recession monetary decisions

We’ve conducted a historical analysis of asset class returns under various scenarios for Fed policy and U.S. growth since 1950. If our base case scenario for 2023 comes to pass – i.e., the Fed pauses at its peak rate for at least six months and the U.S. slides into recession – then history suggests 12-month returns following the final rate hike could be flat for 10-year U.S. Treasuries, while the S&P 500 could sell off sharply (see Figure 1). If the Fed pivots more quickly and cuts rates within six months of its last hike, then history suggests equities could rally in the 12 months following the final rate hike – but bonds could still outperform equities.

This historical analysis suggests a recessionary environment generally calls for cautious positioning even after a hiking cycle ends. While averaging across all growth outcomes shows that equities have tended to rally after the fed funds rate peaks, they nevertheless have also tended to sell off as the economy nears recession.

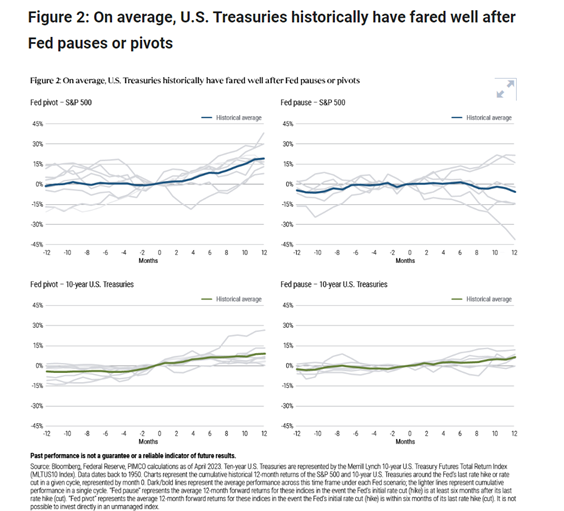

Within these broader observations, the results have varied significantly. In a data set going back to 1950, U.S. equity performance (as measured by the S&P 500) 12 months after interest rates peak has ranged from −41% to +38% – see Figure 2. Among years in which the Fed paused, stocks saw significant gains over the ensuing 12-month period in 2006 and 2019, but in 1981, when inflation was sky-high and a recession materialized, the S&P 500 fell while bond returns were positive. We use the 10-year U.S. Treasury yield as a proxy for bond performance in this figure, but we note U.S. duration tended to perform relatively well across different curve segments.

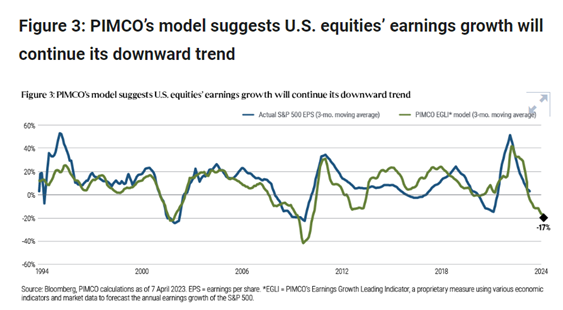

Further, given that earnings per share (EPS) estimates historically have declined by an average of 15% during recessions, current consensus expectations for S&P earnings growth of 1.2% in 2023 and 12% in 2024 appear decidedly optimistic. Indeed, PIMCO’s Earnings Growth Leading Indicator (see Figure 3) has continued to decline and now suggests −17% earnings growth looking forward 12 months. At a forward P/E of 18.4x at the time of this writing, the S&P 500 is also trading well above the 14x–16x level that our historical analysis suggests is consistent with recession. In short, we don’t believe equities are poised to deliver on consensus expectations.

Within specific sectors, defensive equities such as healthcare and consumer staples tend to outperform consumer discretionary and information technology during recessionary pauses, but returns are negative for almost all sectors.

Finally, stock-bond correlations have been generally stable to slightly negative during peak Fed pauses, meaning the two asset classes have tended to move in opposite directions. With a pause as our base case, we believe a multi-asset portfolio would tend to benefit from the diversifying properties of fixed income.

Portfolio positioning implications

In our previous Asset Allocation Outlook, "Risk Off, Yield On," we emphasized that we were moving away from a “TINA” world (where “there is no alternative” to equities) to one in which bonds look cheap relative to equities. Now, bonds also appear attractive due to the current stage of the economic cycle.

Given our base case of a recession in the U.S. with a Fed pause, as well as the range of possible outcomes on either side of that base case, we look to bonds to bolster portfolios. Specifically, we prefer to add high-quality duration at attractive levels, especially during sell-offs if inflation fears resurface. Starting yields historically have tended to be good indicators of future returns in fixed income, and the current levels make duration competitive with equity yields. If the Fed reverses policy more swiftly, the duration could still outperform equities, according to our historical analysis.

We maintain our underweight in equities and take a cautious approach, with a focus on low-leverage and high-quality stocks, particularly those that can grow earnings through an economic downturn. Looking at traditional equity factors, quality has historically delivered strong risk-adjusted returns relative to other factors both during late-cycle expansions and the initial stages of recession. In an environment prone to rapid change, it is advisable to stay nimble to take advantage of dislocations while expressing thematic views via relative value trades.

In credit, we favor staying liquid via credit default swap indices (CDX) and prefer index exposure over generic individual issuers. We aim to minimize exposure to companies vulnerable to higher interest rates. We retain a preference for structured, securitized products backed by collateral assets, and we believe U.S. agency mortgage-backed securities remain attractive since they are typically very liquid and are backed by a U.S. government or agency guarantee.

Global opportunities in times of uncertainty

With the U.S. likely to enter a recession, investors are asking, are there better opportunities for allocation in global markets? We are selective in our approach.

We are neutral on European stocks as waning global growth, a lack of EPS downgrades, and a rate-hiking cycle that lags that of the U.S. could pressure cyclical and value-oriented European indices. Japan is similarly heavy on cyclical, export-oriented sectors, and faces additional uncertainty from the potential removal of the Bank of Japan’s yield curve control policy.

We look instead to emerging Asian markets for intriguing opportunities. In China, for example, equities may stand out: They remain inexpensive, and positive earnings revisions have been modest despite an improving growth outlook. We also continue to monitor inflection points in the semiconductor cycle as we evaluate potential opportunities in South Korea and Taiwan.

In currency markets, select emerging market currencies remain attractive, buffered by high carry and cheap valuation, with increased potential to close the valuation gap after the Fed ends its hiking cycle.

Key conclusions

In light of our macro and market forecasts, we favor bonds as a portfolio allocation due to their diversification, capital preservation, and upside opportunities. In equities, however, we remain cautious as earnings expectations appear too high, and valuations too rich.

Much depends on the decisions of the Federal Reserve and related macro forces, but as the economy shifts toward recession, fixed income may help portfolios navigate challenges and uncertainty.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All