Decelerating economic growth and lowering inflation suggests the central bank is near the end of its tightening cycle.

Though equities have proven resilient, more of the long-expected effects of the Federal Reserve’s (the Fed’s) rapid interest rate-raising policy arrived in April.

“After nearly 500 basis points of tightening, cracks in the labor market and economy are starting to show,” said Raymond James Chief Investment Officer Larry Adam. “This combination of decelerating economic growth and lowering inflation suggests the Fed is near the end of its most aggressive tightening cycle in over 40 years.”

With so many major, contrary currents driving the market, this seems like a good opportunity to answer some of the bigger questions:

What’s the market’s consensus on the Fed’s next move?

It’s expected the interest rate-setting committee will raise rates by about 0.25 percentage points in May, bringing it to 5.25%.

What is the story on inflation?

It continued to recede through April as it has for the prior nine months and is at 5.0% on a year-over-year basis.

Are we still expecting a recession?

The Fed projects a shallow recession will begin in the third quarter. Economic growth slowed in the first quarter, credit continues to tighten and new hire numbers are strongly diminished compared to last year. Though far from painless, the Fed’s expectation is that a recession may be an antidote to the declining, but still persistently high, inflation rate.

Are more banks at risk?

The Fed’s interest rate policy has created challenges for some regional banks as depositors seek better yields from short-term, government-backed Treasury bills and other types of funds. On May 1, First Republic Bank became the third bank to fail in two months and was purchased by JPMorgan in a deal brokered by the Federal Deposit Insurance Corporation. Expect this to be a continuing area of concern, though not at the level of threat feared in March.

Will the Fed lower interest rates if the economy slumps?

This is a central question. “Hike and hold” may be the Fed’s strategy to avoid the “stop and go” strategy that may have prolonged the inflation crisis of the 1970s, but this doesn’t appear to be the market’s prevailing opinion.

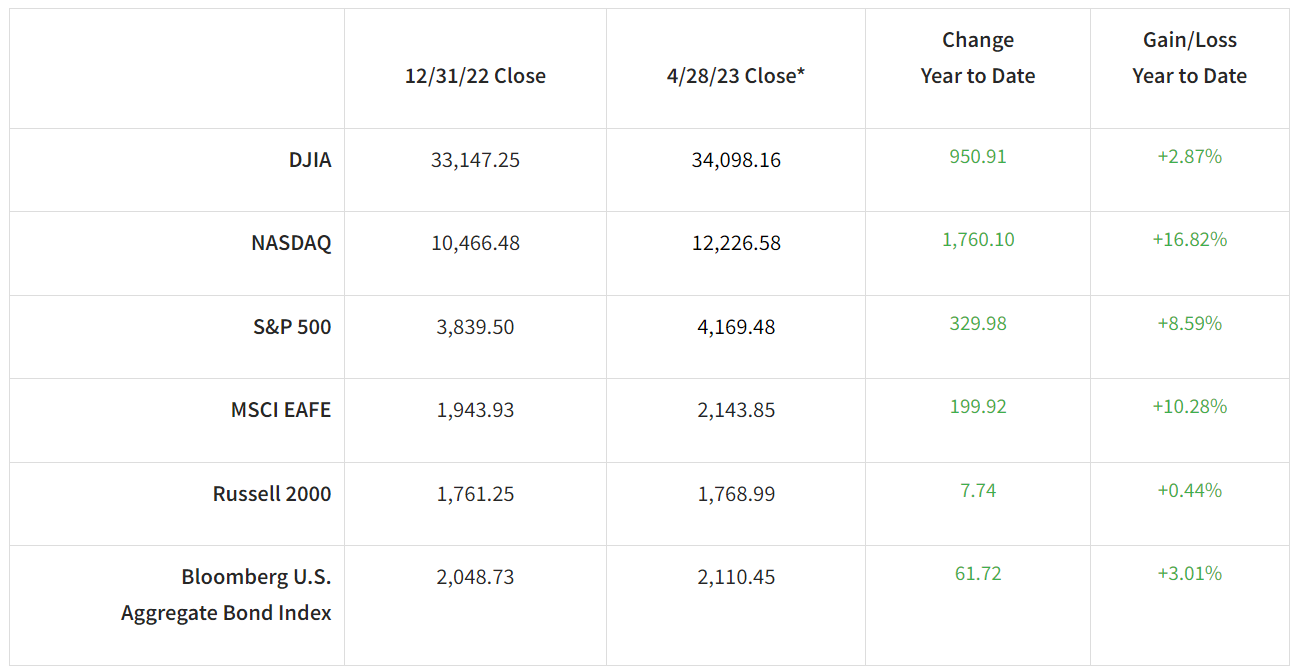

Let’s look at the major indices so far this year and dive into some other areas of interest.

*Performance reflects index values as of market close on April 28, 2023.

Inversion at a historic scale

With short-term rates higher and intermediate-term to long-term rates down, the Treasury yield curve – comparing 10-year and 3-month notes – peaked in April at a -172 basis point inversion. During the Great Recession, the curve inverted -64 basis points at its peak. This has contributed to the challenges facing small banks.

The current yield inversion has persisted for 184 days, nearing the length of the inversion prior to the 2001 recession. However, it is still far shorter in term than the inversion preceding the Great Recession, which lasted 337 days.

Debt limit approaches "X-date"

With the limit of the Treasury’s “extraordinary measures” to pay the nation’s debts projected to come as early as June, House Republicans passed a legislative package that would suspend the debt limit through March 2024, or by $1.5 trillion, whichever comes first. The bill, which sets spending cuts, budget growth caps, regulatory easing for energy producers and the reversal of several key Biden administration priorities has little chance in the Senate, but it does represent an opening of negotiations so as to avoid major damage to the U.S. economy and creditworthiness if a deal is not reached.

Germany goes non-nuclear

Germany shut down its last three nuclear power plants in April, completing a wind-down plan enacted in 2011 and ending a 60-year run of production. Worth noting is that concurrently, Germany disentangled itself from Russian natural gas, which prior to Russia’s invasion of Ukraine had been seen as the Kremlin’s geopolitical trump card.

The U.K. inflation problem

March consumer price data, released in April, confirmed that the U.K. economy is enduring a rate of inflation comfortably, well in excess of that of Western Europe and further above that of the United States than at any time since data in its current iteration began in 1989. Further, it has proven “stickier” than in other nations. Though tight labor markets are not unique to the U.K., its difference in result may be ascribed to the lingering effects of Brexit, with migrant workers returning home, and the lingering effects of the pandemic.

The bottom line

The Fed’s goal of reducing inflation by slowing the economy has been expected to induce a recession, though its arrival has been delayed by market and economic resilience, as well as wage growth and a tight labor market.

If April is an indication, however, we may be on track to see the third-quarter arrival estimate come to fruition. Still, despite layoffs and slowing economic growth and hiring, high wage growth remains a counterpoint.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the authors and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australasia and Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small-cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges, which would reduce an investor’s returns. Investing in the energy sector involves special risks, including the potential adverse effects of state and federal regulation, and may not be suitable for all investors. Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising. International investing involves special risks, including currency fluctuations, differing financial accounting standards, and possible political and economic volatility. U.S. Treasury securities are guaranteed by the U.S. government and if held to maturity offer a fixed rate of return and guaranteed principal value.

© Raymond James

Read more commentaries by Raymond James