Incremental Progress Emerging in the Banking Sector Fallout

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsCIO Larry Adam outlines the positive events that are outweighing negative developments and looks at dynamics to focus on in the week ahead.

While the financial markets and headlines remain volatile, there has been some incremental positive momentum. Review below some of the positive events that outweigh the negative developments over the last few days, as well as some dynamics to focus on in the week ahead.

Positive events

• Global financial contagion averted | Over the weekend, UBS agreed to buy the troubled bank, Credit Suisse, for more than $3 billion. The last-minute deal prevented the bankruptcy of a global systematically important bank and should lay the foundation for greater stability in the banking sector globally amid the current crisis.

• China cutting interest rates | China’s 0.25% reduction in the reserve requirement ratio is another indication that the country’s economic cycle is very different from that of the rest of the world. As the rest of the world has continued to increase interest rates, the Chinese central bank has reduced rates to support Chinese economic activity after the abandonment of the country’s “zero COVID” policy. China stimulating global growth is encouraging to offset any potential weakness in growth in the developed world.

• Central banks enhance liquidity provisions | Over the weekend, the Federal Reserve (Fed) plus the central banks of Canada, England, Japan, the ECB and the Swiss National Bank agreed on a “coordinated action to enhance the provision of liquidity via the standing U.S. dollar liquidity swap line arrangements.” The new measure increases the frequency of “seven-day maturity operations from weekly to daily.” With this new daily frequency, the central banks will be better equipped to deal with global funding issues across the global economy. Increased liquidity for the markets is constructive.

• Lifting of FDIC insurance limit rhetoric | There is growing momentum for allowing the FDIC to either backstop all deposits in the U.S. banking system and/or allow the FDIC to increase deposit insurance from the current $250,000 to a higher level. The first sign appeared over the weekend with an association of mid-sized banks requesting the FDIC to insure all deposits at mid-sized banks for two years to reduce the flow of deposits from smaller banks to larger banks. In addition, on the Sunday talk show circuit, no less than four Congressional leaders – Senator Elizabeth Warren (D), Senator Mike Rounds (R), Senator Chris Van Hollen (D), and Representative Patrick McHenry (R) – suggested the need to revisit the ‘adequacy’ of the current levels. The significance is that this appears to be bipartisan to fully protect depositors and reduce the probability of bank runs.

• Banks helping banks | Last Thursday, eleven of the biggest US banks designed a $30 billion deposit package to help solidify ailing First Republic bank. These uninsured deposits are required to stay for 120 days and are intended to show solidarity and confidence in the U.S. banking system. The participation is notable as the consortium included all five diversified banks, the top two investment banks, and the top two regional banks in the S&P 500 based on GICS sub-industries.

• Falling bank share prices drawing interest | Over the weekend it was leaked that Warren Buffett was in discussions with the Biden administration to help shore up the regional banking sector. As of this writing there has been no news on Buffett making a move, but value-oriented investors appear to be looking for opportunities. Remember that Buffett became a high-profile investor during the 2008 financial crisis and helped build further confidence in the banking sector. In addition, it was announced that the failed Signature Bank was to be purchased by New York Community Bank for $2.7 billion. The point is that the stress-induced declines in several of these institutions are starting to attract high-profile investors, which could lead to further investment and the building of confidence.

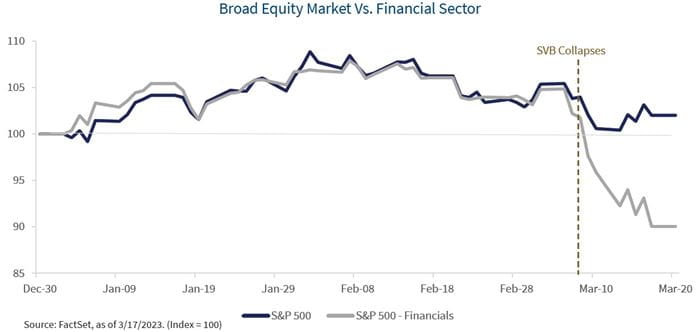

• Market holding up (some sectors rallying) | The overall market has been resilient since the start of this banking crisis on March 8. During this period three sectors have been positive with Communication Services and Information Technology leading on the expectation of lower interest rates. Three additional sectors are down less than a percent, including both consumer sectors. The losses have been focused on Financials, particularly regional banks and Energy, as the price of oil dropped. The positive interventions over the last week helped the S&P 500 finish in the green for the week with 7 of 11 sectors and 15 of 25 industry groups positive.

• Long-term interest rates declining | The root of the problem, high interest rates, is already being addressed as high interest rates are already coming down. Lower interest rates will actually increase the value of bank long-term Treasury holdings and improve their financial wellbeing. In addition, with the 10-year Treasury yield having already fallen 60 bps from its recent high, mortgage rates should fall and that will help stabilize the housing market.

• Oil prices falling | As oil prices have fallen 17.7% year-to-date (to ~$66/barrel), lower gasoline prices for consumers are likely on the horizon. Falling gasoline prices should not only provide relief to consumers but should also provide a catalyst for further deceleration in inflationary pressures – a helpful dynamic to support the Fed in ending its tightening cycle sooner.

Negative developments

• Downgrading of banking sector and individual banks | Moody’s lowered its outlook on the U.S. banking system to negative from stable mid-last week and placed six banks under review for possible downgrades. By week’s end, Moody’s, and other credit rating agencies (S&P and Fitch), downgraded First Republic Bank’s credit rating to junk status. Even though First Republic received a $30 billion cash infusion of deposits last Friday, its credit rating downgrade will make it even more challenging for the bank to raise capital to shore up its finances.

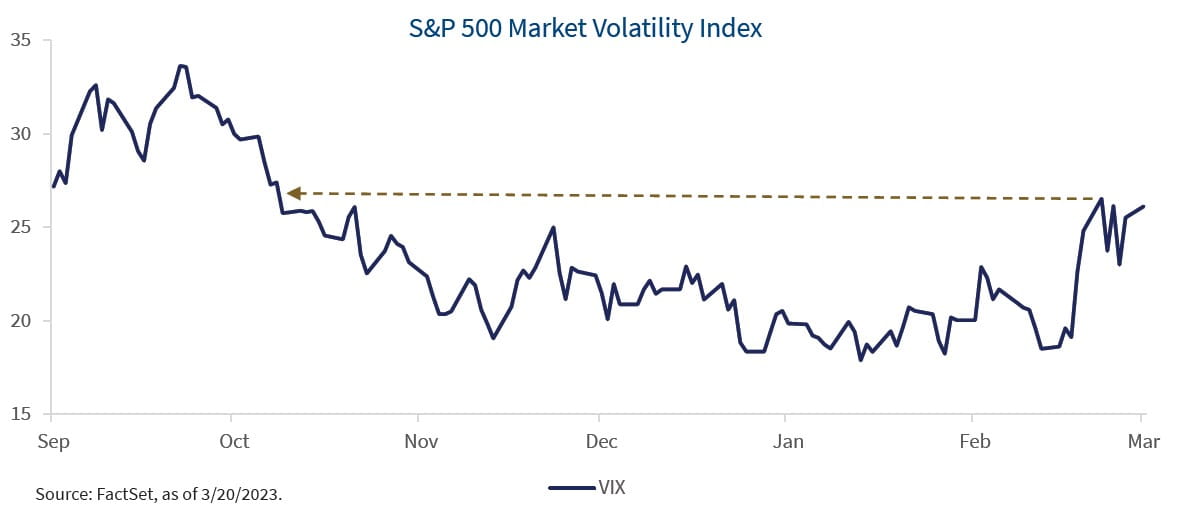

• Elevated uncertainty and volatility | The velocity of news during this banking crisis has led to an increased level of uncertainty and rapidly changing market conditions. The VIX, a measure of S&P 500 volatility, is up nearly 40% since the start of this crisis, finishing at 25.50 on Friday. This week the 2-year Treasury yield hit both 3.71% and 4.53%, the widest weekly dispersion since 2008. This upcoming Wednesday, we will have one of the most uncertain Fed meetings in the post-Alan Greenspan history. This close to the meeting the outcome is typically priced in and very well-choreographed, but currently, the probability of a 0.25% hike is ~60% while no cut is ~40%. Potentially even more impactful will be the comments, which can go in many different directions at this stage. The markets prefer clarity, not uncertainty.

• Growing Fed balance sheet | The ~$300 billion increase in the Fed’s balance sheet will have limited impact on economic activity other than helping stabilize the financial market during a time of stress. This increase in bank borrowing from the Fed is improving banks’ liquidity to regulatory levels rather than creating the potential for banks to increase lending.

• Investors not unscathed | Equity and bond investors have lost money with the recent crisis. In the U.S., several regional banks have suffered significant declines. Overseas, Credit Suisse equity investors have seen their stock price decline over 80% month-to-date and 99% from its peak in 2007. In addition, as part of the UBS’ takeover, the value of Credit Suisse’s $17b ‘CoCo’ bonds were written down to zero by the Swiss regulators, leaving bond holders with a complete loss on their investment. Moves by regulators have targeted stabilizing the financial stability of banks, not the investments of equity and bond holders. Selectivity within the financial market remains imperative.

Bottom line

We remain optimistic that the equity market (S&P 500) will move higher by year end and that interest rates (10-year Treasury yield) will move gradually lower. Overall, there have been some positive developments in dealing with the potential banking crisis. While the positives outweigh the negatives over the last week, that does not mean we are ‘out of the woods’ yet. Watching the funding rates and deposit flows of banks will remain critical drivers of the market and pressure points worth monitoring.

With the rapid rise in interest rates a major contributing factor to deteriorating fundamentals of some banks, focus will be on the Fed’s FOMC meeting this Tuesday and Wednesday. While the Fed is still likely to raise interest rates by 0.25% (to 4.75% - 5.00%), it is a close call as there is the potential it could decide to pause. Although the Fed’s main roles are price stability, i.e., low inflation, and low unemployment, it is also responsible for financial stability in the U.S.. Thus, it will have to weigh the importance of each one of these roles and come up with a decision regarding interest rates.

The Fed has plenty of instruments to deal with financial stability but only one to deal with inflation, the federal funds rate. Thus, it could decide to continue to increase interest rates and at the same time guarantee the stability of the U.S. financial system. However, the recent banking issues are tightening monetary conditions in the U.S. so the Fed may be inclined to err on the side of pausing. In the end, the message from Fed officials will determine the path it is going to choose.

While the rise in interest rates is important, it may take a backseat to the Fed’s new updated forecasts and the guidance it provides for monetary policy going forward. Some key questions include: How many more hikes are projected in the Fed’s forecast? If the Fed does raise interest rates, are there any dissents? Does the Fed believe the ‘disinflationary process’ is still underway? How strong or fragile is the overall banking system? The confidence, or lack thereof, that the Fed exudes in the economy, inflation and banking system will likely affect the direction of the markets.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Group, but not necessarily those of Raymond James & Associates, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital. Material is provided for informational purposes only and does not constitute a recommendation. Diversification and asset allocation do not ensure a profit or protect against a loss.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

INTERNATIONAL INVESTING | International investing involves additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

OIL | Investing in oil involves special risks, including the potential adverse effects of state and federal regulation and may not be suitable for all investors.

The Consumer Price Index (CPI) | is a measure of inflation compiled by the US bureau of Labor Studies.

Personal Consumption Expenditure Price Index | The PCE is a measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services.

DESIGNATIONS

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP® and CERTIFIED FINANCIAL PLANNER™ in the U.S.

Investments & Wealth InstituteTM (The Institute) is the owner of the certification marks “CIMA” and “Certified Investment Management Analyst.” Use of CIMA and/or Certified Investment Management Analyst signifies that the user has successfully completed The Institute’s initial and ongoing credentialing requirements for investment management professionals.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

FIXED INCOME DEFINITION

AGGREGATE BOND | Bloomberg US Agg Bond Total Return Index: The index is a measure of the investment grade, fixed-rate, taxable bond market of roughly 6,000 SEC-registered securities with intermediate maturities averaging approximately 10 years. The index includes bonds from the Treasury, Government-Related, Corporate, MBS, ABS, and CMBS sectors.

HIGH YIELD | Bloomberg US Corporate High Yield Total Return Index: The index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below.

S&P 500 | The S&P Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

BLOOMBERG CAPITAL AGGREGATE BOND TOTAL RETURN INDEX ! This index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. The index is designed to minimize concentration in any one commodity or sector. It currently has 22 commodity futures in seven sectors. No one commodity can compose less than 2% or more than 15% of the index, and no sector can represent more than 33% of the index (as of the annual weightings of the components).

INTERNATIONAL DISCLOSURES FOR CLIENTS IN THE UNITED KINGDOM | For clients of Raymond James Financial International Limited (RJFI): This document and any investment to which this document relates is intended for the sole use of the persons to whom it is addressed, being persons who are Eligible Counter parties or Professional Clients as described in the FCA rules or persons described in Articles 19(5) (Investment professionals) or 49(2) (high net worth companies, unincorporated associations, etc.) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended)or any other person to whom this promotion may lawfully be directed. It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons and may not be relied upon by such persons and is, therefore, not intended for private individuals or those who would be classified as Retail Clients.

FOR CLIENTS OF RAYMOND JAMES INVESTMENT SERVICES, LTD.: This document is for the use of professional investment advisers and managers and is not intended for use by clients.

FOR CLIENTS IN FRANCE | This document and any investment to which this document relates is intended for the sole use of the persons to whom it is addressed, being persons who are Eligible Counterparties or Professional Clients as described in “Code Monetaire et Financier” and Reglement General de l’Autorite des marches Financiers. It is not intended to be distributed or passed on, directly or indirectly, to any other class of persons and may not berelied upon by such persons and is, therefore, not intended for private individuals or those who would be classified as Retail Clients.

FOR CLIENTS OF RAYMOND JAMES EURO EQUITIES | Raymond James Euro Equities is authorised and regulated by the Autorite de Controle Prudentiel et de Resolution and the Autorite des Marches Financiers.

FOR INSTITUTIONAL CLIENTS IN THE EUROPEAN ECONOMIC AREA (EE) OUTSIDE OF THE UNITED KINGDOM | This document (and any attachments or exhibits hereto) is intended only for EEA institutional clients or others to whom it may lawfully be submitted.

FOR CANADIAN CLIENTS | This document is not prepared subject to Canadian disclosure requirements, unless a Canadian has contributed to the content of the document. In the case where there is Canadian contribution, the document meets all applicable IIROC disclosure requirements.

Source: FactSet, as of 3/20/2023

INTERNATIONAL HEADQUARTERS: THE RAYMOND JAMES FINANCIAL CENTER 880 CARILLON PARKWAY // ST. PETERSBURG, FL 33716 // 800.248.8863 RAYMONDJAMES.COM

© 2023 Raymond James & Associates, Inc., member New York Stock Exchange/SIPC. © 2023 Raymond James Financial Services, Inc., member FINRA/SIPC. Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits