Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Fed completes the third consecutive 0.75% rate hike

- Increased probability of a recession in 2023

- Recession is not expected to be severe in nature

Since the August Jackson Hole Symposium, the Fed has cautioned that the tightening cycle was far from over and that “some pain” would be ahead for the economy. If that message hadn’t been fully received, Wednesday’s Fed proceedings made it crystal clear. Even though the narrative of the FOMC (Federal Open Market Committee) statement shifted only slightly, it was the increase in the terminal rate (e.g., potential peak) forecasts for 2022 and 2023 from 3.4% and 3.8% to 4.4% and 4.6% respectively that got the markets’ attention. These adjusted projections not only signaled that rates will move well into restrictive territory, but that the rate hike story will extend into 2023. As we stated last week, taking rates to 4.5% or higher would increase the probability of a mild recession next year. Here are our areas of concern:

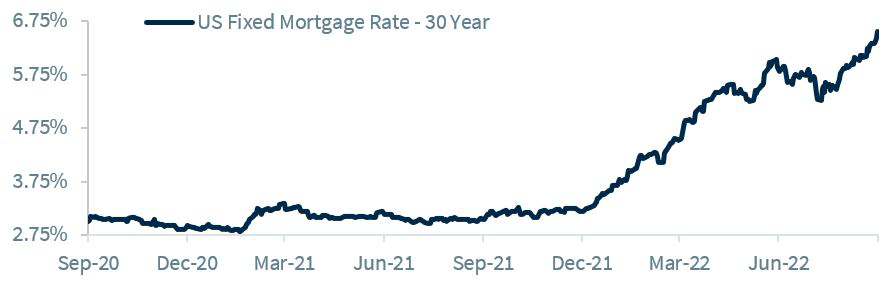

- Housing Market Headed For A Slowdown | In the aggregate, tighter monetary policy typically acts on a lag. But for the more interest-rate sensitive sectors of the economy such as the housing market, signs of a slowdown are already occurring. The days of bidding wars, all cash offers, and purchases of homes sight unseen are fading as the 30-year fixed mortgage rate has soared above 6.5% for the first time since 2008. As interest rates climb, builder sentiment continues to decline. In fact, building permits just experienced the largest decline since the pandemic, reaching the lowest levels since June 2020. From the Fed’s vantage point, some of this bad news is good news, as it shows that higher rates are cooling the once exceedingly hot housing market. Shelter costs, which have been a culprit of persistent inflation and traditionally lag home prices, should ease in the year ahead. But while this may all be welcomed news for the Fed, it is not a positive for GDP. Think about all the spending that accompanies the purchase of a home, or what are called the indirect effects generated by the housing market: realtor costs, repairs, enhancements, furniture, electronics, etc. While we do not foresee a housing correction the likes of the Great Recession due to the higher quality of outstanding mortgages, the contraction in housing activity will likely weigh on the economy.

- Setbacks From A Stronger Dollar | The euro, yen, and pound are at the weakest levels relative to the US dollar since 2002, 1998, and 1985 respectively. For Europe and the UK, this has exacerbated elevated energy costs as key commodities such as oil are priced in dollars. For Japan, its central bank was forced to intervene in the foreign exchange markets to prop up the yen for the first time since the Asian Financial Crisis. But while a stronger dollar complicates economic circumstances for these developed nations, it is not without consequence in the US. Yes, the strength of the dollar greatly reduces the cost of imports, which in turn helps abate inflation. However, it hampers our export activity as our goods become more expensive overseas. It also poses a challenge to multinational corporations, especially those who derive a substantial portion of their revenues overseas. Already, many large tech firms have indicated that earnings would take a greater than previously expected hit due to exchange rates. Since the US economy remains stronger on a relative basis, the dollar’s strength should remain intact in the months ahead.