Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

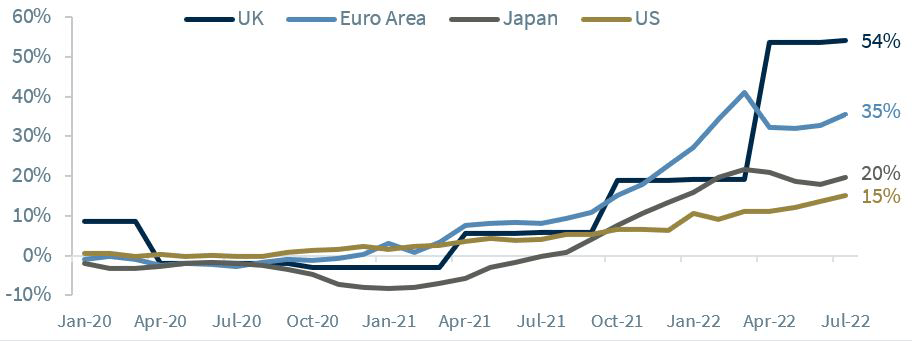

- Weaker euro compounds pricing pressures

- Energy prices prolonging Europe’s inflation peak

- European economy inching closer to a recession

Traffic signs provide critical information to drivers—indicating what to expect up ahead, creating order on roadways, and hopefully ensuring safety. For much of this year, the global economy has seemed to be at a ‘Recession Crossroad,’ with the weight of inflation and central banks’ responses to escalating price pressures leading many to conclude that a recession was the near-term destination for many developed economies. While we never merged with these expectations when it came to the US economy, recession risks loom in Europe as there are a number of hazards (e.g., weakened euro, still soaring inflation and an ongoing energy crisis) on the region’s route. In light of these challenges, below outlines why investors should exercise caution when investing in European equities in the months ahead.

Bottom Line – There Are Uneven Lanes In The Global Economy | For as much concern that has been voiced over the US economy, the situation is more dire in Europe. Next Wednesday, the euro zone will release economic sentiment, PMI manufacturing, and the all-important inflation report just ahead of the ECB’s next meeting on September 8. With energy prices yet to peak, Europe’s inflation reading is likely to set another multi-decade record and weigh further on consumer sentiment and business outlooks. As such, we continue to favor the US over Europe and other developed regions due to better economic prospects (e.g., a tightening cycle closer to completion, less sensitivity to the energy surge), evidence of corporations that are more resilient in times of distress, favorable profitability metrics, and more visibility in earnings forecasts.

Click here to enlarge

View as PDF

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

© Raymond James

Read more commentaries by Raymond James