While inflation fears remain high, it is likely that we are past peak inflation and the largest interest rate increases are behind us.

The Federal Reserve (Fed) continued its aggressive battle against inflation, raising the federal funds rate another 0.75% at its July meeting – the fourth rate bump this year. We’re now in a neutral 2.25% to 2.5% range, and the central bankers are on track to raise rates to a mildly restrictive 3% to 3.5% range by the end of the year. While inflation fears remain high, it is likely that we are past peak inflation and the largest interest rate increases are behind us, explains Raymond James Chief Investment Officer Larry Adam, echoing Fed Chair Jerome Powell.

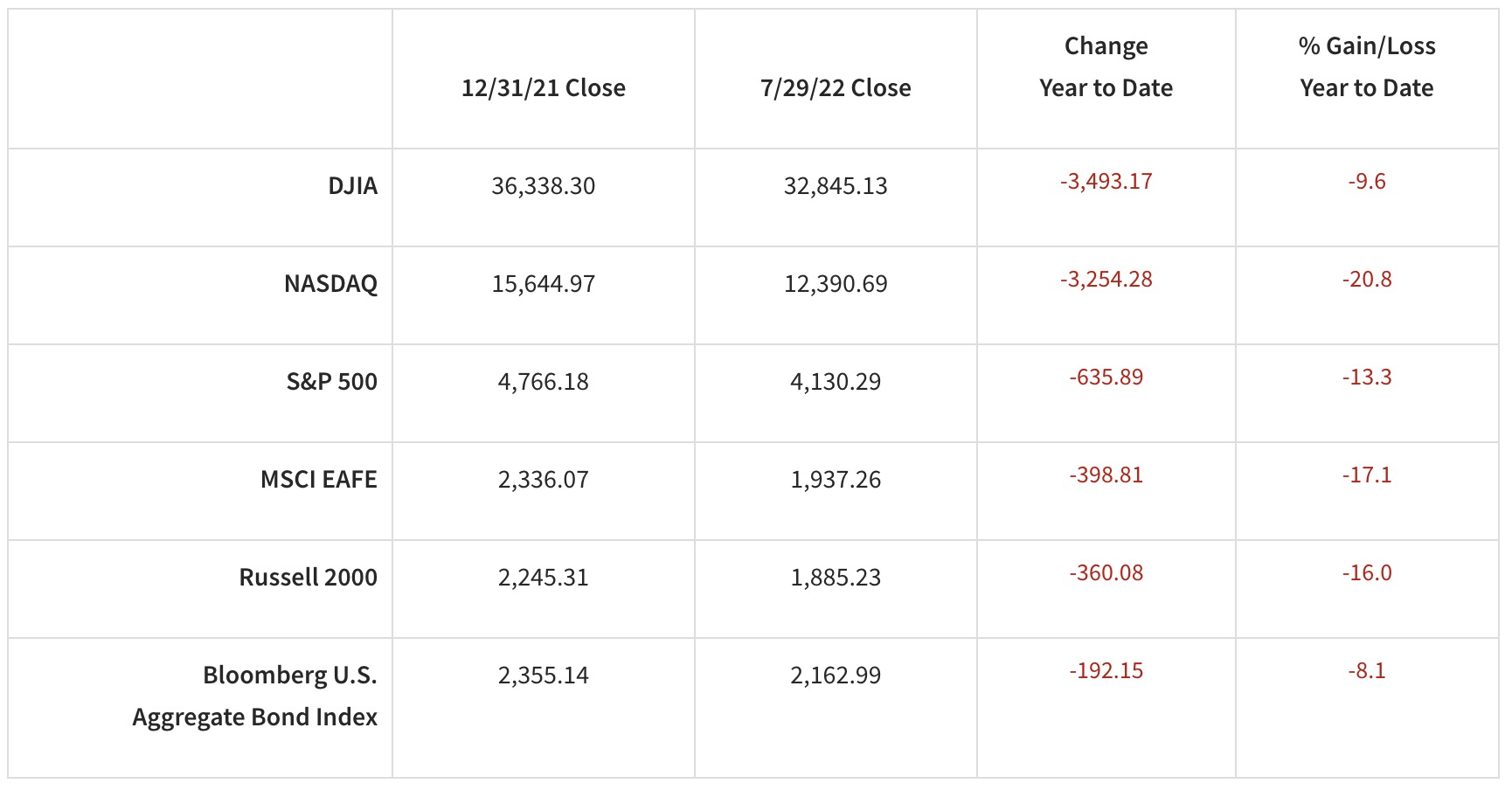

The domestic equity markets anticipated the rate change and appeared to appreciate the Fed’s firm stance. The S&P 500 climbed around 9% for the month – the highest monthly increase since November 2020. This is in contrast to the worst start to the year since 1970 that had the S&P 500 down 20% through June and the Bloomberg U.S. Aggregate Bond Index down 10%.

July’s reprieve came with declining oil prices (and the subsequent impact on inflation) and slowing economic activity – the second consecutive quarter of negative GDP growth, which helped spur the bond market as longer-term interest rates declined meaningfully.

None of this eliminates the possibility of a mild, short-lived recession, notes Chief Economist Eugenio J. Alemán, Ph.D. Investors should expect some challenging months ahead as we navigate uncertainty around global inflationary pressures coming from the continuing pandemic; Chinese lockdowns, which could constrain supply chains further; the Russia-Ukraine war and its implications on energy; as well as “noisy” data. For example, existing home sales weakened in the second quarter, but their prices are still climbing, just not at the pace they had in recent quarters. Meanwhile, new home sales declined to their pre-pandemic levels.

The Bureau of Economic Analysis reported that second-quarter real gross domestic product came in at ‑0.9% following a 1.6% decline in the first quarter. On the other hand, corporate earnings season appears to be robust thus far, buoyed by relentless consumer spending. Personal consumption expenditures, which account for almost 70% of the economy, grew by 1% during the quarter. It seems U.S. companies and consumers remain relatively healthy for now.

Performance reflects price returns as of market close on July 29, 2022.

Inside D.C.

The CHIPS and Science Act heads to President Biden’s desk for approval, codifying incentives for domestic semiconductor manufacturers and suppliers. They could see billions in grants and investment tax credits toward the expansion and construction of U.S.-based manufacturing facilities.

A reconciliation bill focused on climate/energy, corporate tax changes and healthcare policy (mainly lowering costs of drug prices and an extension of health insurance subsidies) also could become law prior to the August congressional recess. While there are no energy-related mandates or other “sticks” in this reconciliation bill, there are plenty of “carrots” for clean energy technologies in the form of tax incentives. Political factors led to significant priorities being dropped from both bills, namely broader (and more hawkish) China-oriented policy provisions as well as individual tax adjustments targeting higher incomes. But that doesn’t preclude Congress from tackling China-related economic and investment policies in the future, notes Washington Policy Analyst Ed Mills.

The global outlook

The outlook for the global economy continues to weaken, and forecasts for economic activity outside the U.S. reflect persistent inflationary pressures, supply chain disruptions and tightening financial conditions. Downside trade pressures and higher energy prices are having an outsized effect, one that’s particularly acute in Europe and in the United Kingdom. Ongoing concerns regarding the continent’s gas supply have served to emphasize regional vulnerabilities. Russia cut its exports of natural gas to Europe, which had a ripple effect on natural gas prices – both liquefied and non-liquefied.

Global headline inflationary pressures may have peaked, which would provide some much welcome stability to global stock and bond markets after a tough first half of the year. Recent survey data indicates that prolonged supply chain difficulties may have eased somewhat, and we may see inflationary pressures subside in the months ahead.

The bottom line

We likely have more weakness to endure, but Joey Madere, senior portfolio strategist, Equity Portfolio & Technical Strategy, says investors can expect positive returns over the next 12 months and beyond, given the view that economic weakness should be relatively mild and inflation will moderate. Long-term investors should anticipate an eventual rally on the other side of this weak trend and take advantage of potential buying opportunities. Bear markets go down 20% to 35% on average, but bull markets average roughly 150% returns.

While volatility feels uncomfortable, experience suggests that adaptability and a cool head will help weather any market environment and position for the future.

Your financial advisor can help address questions about how current conditions may impact your holistic plan.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Raymond James Chief Investment Office and are subject to change. There is no assurance the trends mentioned will continue or that the forecasts discussed will be realized. Past performance may not be indicative of future results. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australia, Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. The performance mentioned does not include fees and charges which would reduce an investor’s returns. Small cap securities generally involve greater risks. International investing is subject to additional risks such as currency fluctuations, different financial accounting standards by country, and possible political and economic risks. These risks may be greater in emerging markets. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

© Raymond James

Read more commentaries by Raymond James