Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- Tech sector was the ‘teacher’s pet’ during rally

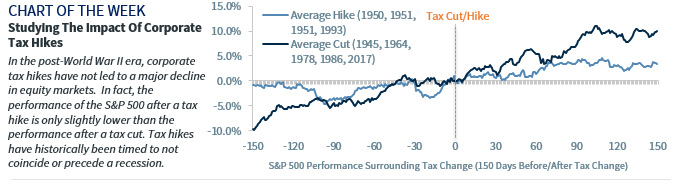

- ‘Studying’ the historical impact of corporate tax hikes

- Big-Pharma ‘doing their homework’ on vaccine safety

School is back in session! Whether it be virtual or in-person, we hope all students had a safe, terrific first week back in the classroom. We also wish a positive, productive academic year to our teachers, all of whom have gone above and beyond to adjust lessons plans in adherence with COVID-19 related guidelines in an effort to ensure that the next generation of thought leaders receives a quality education during this unprecedented time. Any teacher knows that one of the best ways to keep students engaged is to ask questions, and from my own experience as a graduate professor at Loyola University Maryland I know its not only a way to assess learning but also a way to spark curiosity and conversation. For investors, the S&P 500’s recent 7% pullback, the upcoming presidential election, and the announcement of a pause in a late-stage vaccine clinical trial have all sparked concern, so we’re taking the opportunity to address these very important questions that have come to light this week.

-

Is This A Repeat Of The Dot Com Bubble? | The S&P 500 posted its best summer since 2009, but lost steam heading into Labor Day Weekend, and as of Tuesday, had declined ~7% in just three trading days. Heading into this pullback, the Technology sector was the market’s ‘teacher’s pet’ as it outpaced the broad S&P 500 by 28%. But just as Tech led the rally, it also declined the most—falling more than 11% over the same three day period. The speed and magnitude of the decline had investors questioning if history would repeat itself, setting up the recent tech-oriented run-up for a painful reversal akin to the Dot Com bubble bursting in 2000. However, there are several factors that differentiate the current state of the Tech sector from the Dot Com Era.

- Valuations for the Tech sector are elevated from a historical perspective (NTM 26x vs. 20-year average of 18x), but they are well-below the 2000 peak of 57x and are justifiable given the earnings outlook. The sector is expected to see earnings growth of 5% and 14% in 2020 and 2021 respectively—one of only two sectors expected to see positive earnings growth this year. Lower interest rates should also be supportive, given that today’s 10-year Treasury yield of 0.68% is well below the 6.4% yield in 2000.

- Today’s leading tech firms have stronger fundamentals and multiple revenue streams (hardware, software, services, cloud, content, etc.) rather than being one trick ponies focused on a single product or service. Furthermore, the leaders continue to find new applications for existing technologies and invest in future technologies to remain competitive.

- In 2000, tech companies were predominately focused on business demand, compared to today where they are at least equally focused on consumer demand as a growth driver. The roll-out of 5G should also serve as a catalyst for both of these markets.