Global investors face more years of a protracted low yield environment, as central banks slash interest rates to combat the coronavirus-led recession. The low yields have left many investors with insufficient returns to meet their goals, prompting some to look further out along the risk scale, often beyond their preferred risk tolerance. At PIMCO, we believe this is not necessary, as parts of some asset classes, such as credit, may still compensate for risk. Overall, however, we remain cautious on credit, given the economic slowdown and recent spread tightening, favoring high quality issuers. We highlight below where and why we see potential opportunities:

1) With a little help from the Fed

- Using experience gained during the 2008 global financial crisis, major central banks have sought to rescue financial markets in periods of extreme volatility. From the European Central Bank’s (ECB) asset purchase program in June 2016 to the U.S. Federal Reserve’s (Fed) record-breaking measures announced in March 2020, central bank support has helped smooth markets, triggering a shift in investment flows. As shown in the chart, many investors are returning to investment grade and high yield credit markets.

- This ongoing monetary support, combined with near-record-low government yields, may lead investors to seek income in traditional income-producing asset classes, such as credit.

- This major central bank support does not mean, of course, that exposure to credit sectors cannot generate losses for investors, particularly in the short term. Amid the COVID recession, investors need to be vigilant of the risks, particularly at the lower end of the credit spectrum.

2) Implied versus real defaults: an opportunity for active investors

- Markets tend to exaggerate certain situations, turning unexpected events into panic or euphoria that eventually wane as fears and hypes calm down. At present, the uncertainty around the effects of the COVID-19 crisis on the global economy still weighs on credit, as much of the recovery depends on whether a vaccine will be ready, and when. This has made some investors price in a pessimistic scenario, which might actually be far worse than what time brings.

- As seen in the chart, current spread levels imply that more than 12% of the outstanding U.S. investment grade companies will default (fail to meet payments) over the next five years. This is much worse than the worst historical five-year cumulative default rate of 2% for the asset class. In other words: Things have never been as bad as what the market is implying. Europe offers a similar scenario.

- Active investors who can focus on the highest-quality and most resilient companies may benefit from any spread tightening that may happen if real default rates are lower than what markets expect.

- Assuming a 40% recovery rate, current investment grade credit spreads imply default rates of more than 10% in both Europe and the U.S.

- This far exceeds the worst actual 5-year cumulative default rates experienced in investment grade corporate credit.

3) Improving market conditions

After the sharp equity and credit sell-off in March, when volatility reached 2008–2009 levels, markets have calmed down, following record central bank action. The unprecedented levels of support from the Fed, the ECB, and the Bank of Japan (BOJ) have helped markets recover in three key areas:

-

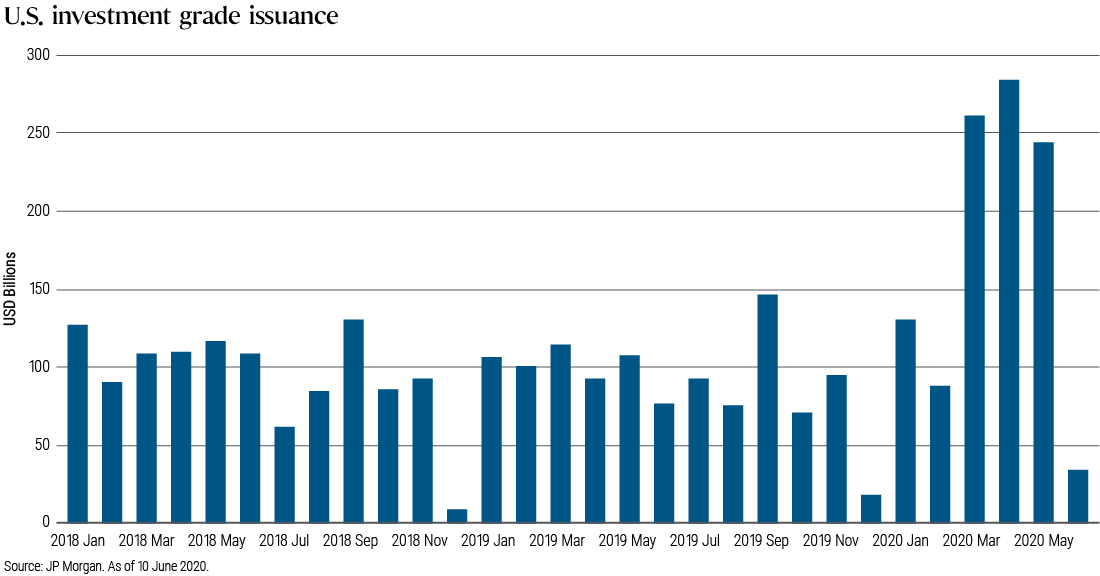

Primary issuance is back: In 2020 year to date, investment grade companies have raised $1 trillion, and high yield firms, $140 billion, following a sharp increase in May, as seen in the chart.

-

Narrowing basis: The difference between cash bonds and the derivative contracts that investors use to replicate those cash bonds is called the basis. In theory, this difference should be close to zero, but it is often negative (a median of −19 basis points (bps) for investment grade over the past 15 years) as buying exposure to credit risk through bonds is cheaper than through the more liquid derivatives market. In March, the basis widened substantially to around −200 bps, before narrowing again, following the support measures announced by major central banks. This narrowing is a sign that the market is improving.

-

Improved liquidity: The difference between the bid and ask prices (how much investors are willing to pay and how much sellers are willing to offer) is also narrowing, a sign of improved liquidity. The bid-ask spread spiked in March 2020 to levels not seen since the 2008–2009 financial crisis, but then declined significantly after the announcements of central bank support.

4) The power of coupons

- Bonds have been providing income to investors for centuries. While bondholders no longer need to literally clip and cash their coupons, the concept is the same: An issuer’s commitment to pay interest may absorb part of the price losses derived from a company-specific problem, or an external event that roils markets.

- As seen in the chart, bond returns are made up of three major components: coupons, price, and others (for instance, foreign currency moves). Plotting these components alongside the total return of the Bloomberg Barclays Global Aggregate Corporate Index (of investment grade securities only), we note how the index has delivered losses in four of the past 15 years, while the price component of the index fell in eight of those years – meaning in four of those eight years, the coupon helped absorb and more than offset those price losses.

- While it is usually the lowest-rated companies that tend to pay the highest coupons to lure buyers, investors should be cautious and assess risk, choosing the optimal level of income for the risk assumed.

5) Spread levels: are we nearly there?

- The extreme market turbulence in February and March drove credit spreads (the premium that investors pay to compensate for credit risk) to levels not seen since 2008–2009. In some markets, the panic sell-off indiscriminately affected most companies, including those with solid fundamentals.

- Following the unprecedented support measures unveiled by major central banks, spread levels have tightened again, but still remain above long-term averages, as shown in the chart (dotted lines).

- While there is no guarantee that spread levels will mean-revert to those long-term averages, we believe that some high-quality companies will be more resilient to the economic slowdown and therefore should see their risk premiums narrow as economies improve. Against this backdrop, active investors with deep resources to analyze companies and markets will be better placed to find opportunity.

© PIMCO

www.pimco.com

© PIMCO

Read more commentaries by PIMCO