The Fed could give the economy a powerful boost by maintaining the mix of assets on its balance sheet.

Following the Federal Reserve's 50-basis-point rate cut on 3 March, the fed funds target range stood at 1.0%−1.25%. The financial markets continued to be volatile, and U.S. stock markets declined on concern that the rate cut may not be enough to offset the economic impact of COVID-19. But with the policy rate so low, an important question now is, what more can the Fed do?

We have seen an incredible disruption to both financial markets and lives as people look to protect themselves from the physical spread and the potential economic impact of the coronavirus. Amid dramatic market volatility, U.S. Treasuries have rallied and equities have plunged. Over the past week, a chorus of participants called on the Fed to act immediately, and it responded by cutting the policy rate.

Clearly, leadership at the Fed is concerned about the ramifications of the coronavirus. After equities plummeted for a week, Fed Chair Jerome Powell on 28 February let investors know in a statement of just one paragraph that the Fed will “use our tools and act as appropriate to support the economy.”

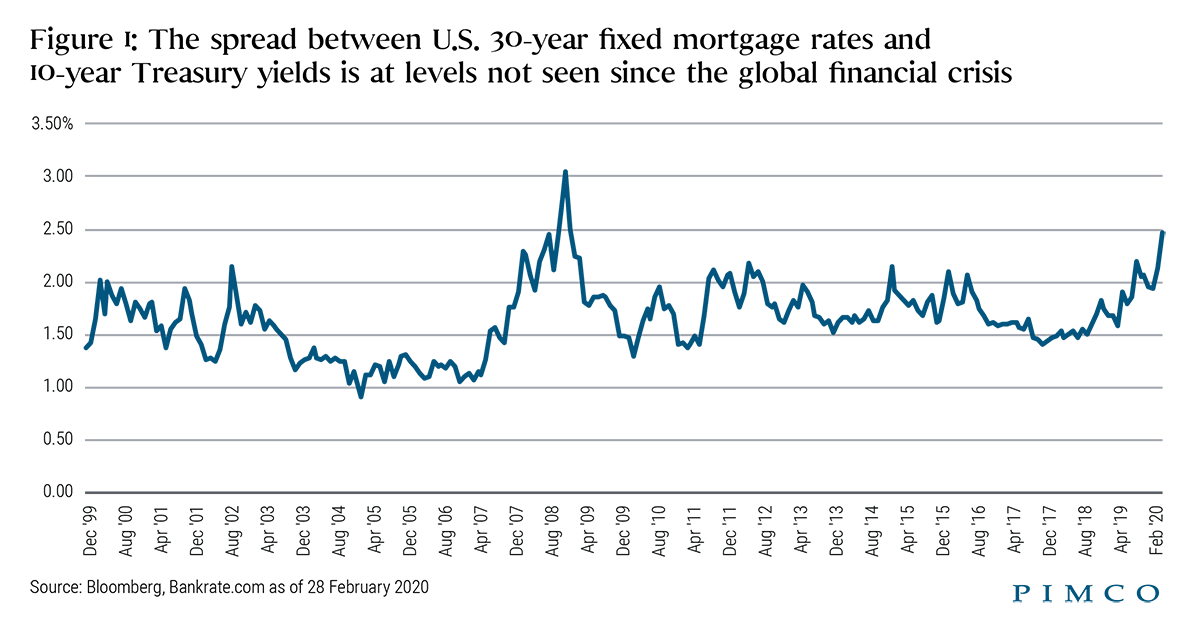

Indeed, since 2019 the Fed has been easing through a combination of rate cuts and balance sheet expansion via purchases of short-maturity Treasuries. Offsetting some of this easing, the Fed has been simultaneously tightening by selling (running off) $20 billion of mortgages per month. We believe this monetary policy “tool” of directing the size of the Fed’s balance sheet is potentially more powerful than cutting the policy rate, and with a far lower likelihood of unintended consequences.