In Part I of this report, we reviewed the history of Japanese-Korean relations over the last several centuries, highlighting the Japanese invasions of Korea in the 1590s and 1890s, Japan’s assassination of a Korean queen in 1895, and Japan’s colonization of Korea from 1910 to 1945. We also showed how Japanese attitudes have been colored by Korea’s assimilation of Chinese culture and its close geographical proximity to the Japanese homeland. As a result, we argued that the enmity between these two ancient peoples is probably much worse than most observers realize, even if their mutual dislike was subsumed under the hegemonic leadership of the United States after World War II. Key to that process was U.S. pressure on Japan and South Korea to sign their Treaty on Basic Relations in 1965, under which Japan gave $500 million in aid to South Korea in order to settle all claims related to its colonization of the peninsula. This week, in Part II, we’ll explain why Japanese-Korean hostilities have suddenly broken out into the open again. We’ll conclude by discussing the implications of the dispute for the countries’ economies and for investors.

The Fateful Court Case

Japanese-Korean tensions may have been frozen under U.S. hegemony, but they never disappeared completely. As recently as the 1990s, for example, South Korea banned imports of Japanese videos and comic books. There certainly have been periods of warming, as when Japanese prime ministers formally apologized for the country’s colonial behavior. In 2015, Japan also agreed to contribute to a foundation to compensate Korean “comfort women” who had been forced into sexual slavery for the Japanese military during the war. However, many Koreans refuse to believe the Japanese are truly sorry for their behavior before and during World War II, and many consider such compensation to be grossly inadequate.

The proximate roots of the current dispute stem from two actions by the South Korean government last year. In November 2018, South Korean President Moon Jae-in dissolved the comfort women foundation on the grounds that the 2015 agreement didn’t reflect the victims’ actual desire and didn’t require the Japanese government to admit guilt. More importantly, the South Korean Supreme Court ruled last October that the Treaty on Basic Relations of 1965 only resolved state-level claims for diplomatic purposes, rather than individual claims based on pain and suffering. That decision has allowed thousands of South Korean citizens to sue dozens of large, well-known Japanese firms for damages related to forced labor before and during the war. Subsequent court decisions have also allowed those citizens to seize the assets of the Japanese companies.

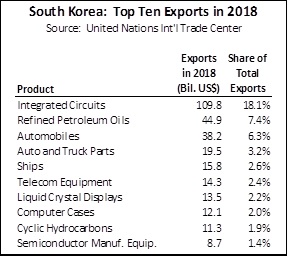

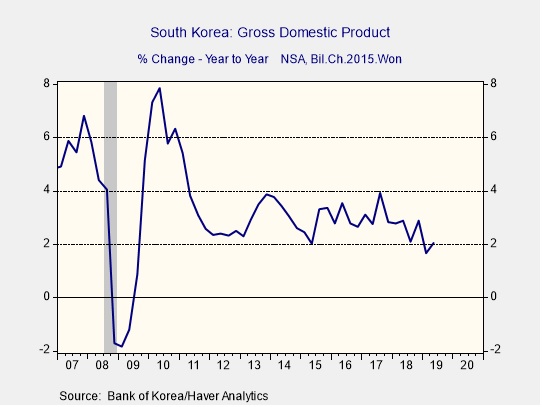

Japan has vehemently protested the South Korean court decisions on the grounds that the 1965 treaty was meant to be the final, decisive adjudication of its colonial behavior. When those protests proved ineffective, the Japanese decided to take more forceful action this summer. The government of Prime Minister Shinzo Abe announced tough new export licensing requirements for three key chemicals sold to South Korean semiconductor manufacturers. The Abe government has justified the restrictions on national security grounds, claiming South Korea was allowing them to be re-exported to North Korea. However, the move is widely seen as direct punishment for the court decision allowing damage suits against Japanese companies. Given the importance of semiconductor manufacturing to the South Korean economy (see Table 1) and Japan’s near-monopoly on producing the chemicals, Abe’s move has the potential to cause serious damage. Along with additional export restrictions imposed in August and the removal of South Korea from Japan’s “white list” of nations that are allowed easier export procedures, the situation is likely to exacerbate a recent slowdown in South Korean trade and overall economic growth (see Figures 1 and 2).

South Korea has responded to the Japanese measures with its own trade restrictions, but it has less economic leverage than Japan. South Korea’s main economic response has been some loosely organized boycotts by Korean firms and individuals. In late August, however, it expanded the dispute by pulling out of a U.S.-brokered agreement to share intelligence on North Korea with Japan. With little hope of imposing serious economic costs on Japan, the move aimed to punish Japan by weakening its national defense.

The Problem of the Weary Hegemon

The current Japan-South Korea dispute is a fascinating example of how historical consciousness of conflicts from centuries ago can color a society’s approach to modern conflicts. Society, as a whole, has a longer memory than you might think. If a population is large enough, it will probably always include at least some individuals dedicated to keeping alive the memory of past traumas and nursing grudges over past wrongs. During times of national stress or conflict, those individuals have a ready explanation for their country’s troubles. They know exactly who to blame. Since the Global Financial Crisis, immigrants have been among the most convenient scapegoats for the crisis and slow recovery of many countries. In the conflict between Japan and South Korea, it’s easier for each side to see their villain across the Strait of Korea.

Table 1.

Figure 1.

It’s just as important to remember that such history-laden conflicts can be suppressed and frozen by the great powers we know as hegemons. For a great power like the United States, which exercised hegemony over the non-communist world from World War II up to the recent past, it is vital to maintain order, security, free trade and free capital flows. The hegemon therefore works hard to control such internecine conflicts. Indeed, it was the U.S. that pressured Japan and South Korea to bury the hatchet with their 1965 treaty, and it was the U.S. that pushed South Korea to start sharing its intelligence on North Korea with the Japanese. The hegemon’s vital interest is to keep such conflicts buried. The hegemon’s pressure to keep those conflicts under wraps helps provide stability and prosperity for those that would otherwise be in conflict, but tensions can remain dormant “just under the surface.”

Figure 2.

This Japan-South Korea dispute shows what can happen when a hegemon grows weary. As fewer U.S. citizens remember the great dangers that were faced and overcome during World War II and the Cold War, the expenditure of blood and treasure for the sake of hegemony has naturally lost support. Those who argue for the immediate self-interest of the nation have gained greater sway in the public conversation. President Trump’s “America First” policy is in the ascendency, and the administration has begun to expend fewer resources on maintaining hegemony and controlling disputes like the one between Tokyo and Seoul. Other than a few expressions of concern, the U.S. government has shown little inclination to invest time, energy or resources into quieting the dispute. Consequently, the conflict festers with no sign of healing in the near term.

More broadly, we see the Japan-South Korea dispute as just the latest of many such international conflicts that were previously frozen under U.S. hegemony but are now thawing again. For example, Britain’s pullback from its engagement with continental Europe has depended largely on the acquiescence and encouragement of the Trump administration.[1] Similarly, after decades in which the U.S. was able to tamp down the historical animosities between Greece and Turkey in the interests of strengthening the North Atlantic Treaty Organization against the threat from Russia, the Turkish government has recently angered the Greek government by stepping up exploration for natural gas off the divided island of Cyprus. Even outside its network of Cold War alliances, the U.S. is stepping back from its role as global policeman. In India, the government was emboldened enough to eliminate the special autonomy previously granted to the Muslim-majority state of Kashmir.[2] The common thread in all these developments is that the U.S., weary of the costs of global leadership and weakened by domestic disagreements, has decided to devote less time and energy into batting down the conflicts.

Ramifications

Because of China’s dominance in Asian trade and investment, we think Japanese and South Korean stocks in the near term will continue to be driven mostly by the ups and downs of the U.S.-China trade war. All the same, Japan and South Korea trade a lot with each other, so if the current dispute continues or worsens, many companies in each country could face decreased export opportunities, severed supply chains, boycotts, and the like. Without seeing a catalyst for improved relations in the near term, we think the dispute will continue to fester. We believe Japanese and South Korean stocks will continue to face headwinds on top of the impact from the U.S.-China trade war. To the extent that the economic risks remain and equities are still challenged, Asian and global bonds are likely to benefit from safe-haven buying.

For commodities, we see a similar dynamic. Basic materials ranging from crude oil to copper are likely to remain under pressure in the near term primarily because of the negative impact of the U.S.-China trade war, which has undermined confidence, slowed investment and reduced manufacturing activity worldwide. If the Japan-South Korea trade conflict worsens and adds to that dynamic, we would expect to see further negative impact on demand for most commodities. The main exception would probably be precious metals. Although weaker Asian prospects could help keep the dollar strong, which would tend to weigh on precious metals prices, that would likely be offset by safe-haven buying and increased attractiveness of the metals as rising bond prices drive interest rates lower.

Patrick Fearon-Hernandez, CFA

October 7, 2019

This report was prepared by Patrick Fearon-Hernandez of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

1See WGR, When Hegemons Fade (4/8/19)

2 See WGR, A Kashmir Sweater (9/9/19)

© Confluence Investment Management

Read more commentaries by Confluence Investment Management