In Part I, we began our analysis with a discussion of Mundell’s Impossible Trinity. We also covered the gold standard model and Bretton Woods model. This week, we will examine the Treasury/dollar standard and introduce what could be called Bretton Woods II. Finally, we will conclude with market ramifications.

The Dollar/Treasury Standard

The flaws of the Bretton Woods system led President Nixon to close the gold window in August 1971. In terms of the Impossible Trinity, we had the following:

- Floating exchange rate

- Independent monetary policy

- Open capital account

The third element didn’t occur immediately, but, as the anecdotes in Part I about the advent of currency futures and the Eurodollar market suggest, the owners of capital were agitating for the ability to leave the Bretton Woods straitjacket on foreign investment. In the years following 1971, restrictions on foreign investing steadily declined.

The dollar/Treasury standard effectively replaced gold as a reserve asset. As foreign economies acquired dollars for reserve purposes, they would now hold Treasuries as the primary reserve asset. Although this change, in theory, didn’t eliminate the Triffin Dilemma, in practice, it did. Foreign nations needed a currency to conduct trade and investment and the willingness of the U.S. to act as importer of last resort overcame concerns about America’s creditworthiness. As long as foreign dollar holders remained confident, the U.S. could expand the reserve asset (Treasuries) almost without limit.

The lack of constraint on Treasury supply led to two outcomes. First, foreign nations that wanted to develop economically could use export promotion as a model. In this model, the developing nation restricts consumption through low deposit rates, capital controls and an undervalued exchange rate. These constraints lead to high levels of domestic saving, creating liquidity for investment. What isn’t invested, however, must find a home and that home, based on basic macroeconomics, is either a government fiscal deficit or a trade surplus.

Most nations opted for a trade surplus. The trade surplus had the additional benefit in that it allowed for the accumulation of foreign reserves; holding dollars eased the purchase of commodities and built a “war chest” to prevent potential banking crises.

For the U.S., this behavior led to persistent current account deficits and fiscal deficits.

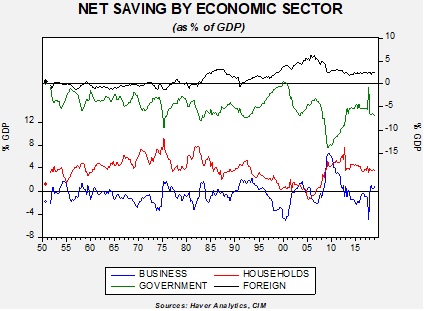

This chart shows net saving for the U.S.; each category is scaled by GDP. Note that from 1950 into 1980, household saving tended to fund government and business dissaving. Foreign saving, the inverse of the U.S. current account, was mostly balanced prior to 1980. As foreign saving rose (the current account became a larger deficit), household saving began to decline. In effect, as foreign saving poured into the U.S. economy through the current account deficit, households were forced to consume more imports. This process, a key element of globalization, depressed inflation (which was rampant in the 1970s) at the cost of depressing wages. To maintain their spending in the face of falling wages, household borrowing rose, facilitated by foreign saving.

Globalization has contributed to rising inequality which was masked by the rise in household debt.

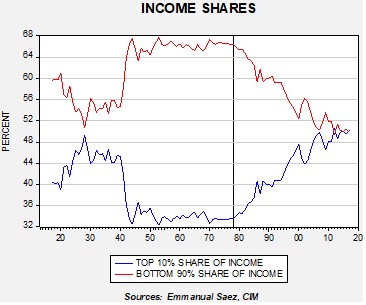

This chart shows the share of national income captured by the bottom 90% of households compared to the top 10%. Since globalization accelerated, shown by the vertical line on the chart, the top 10% are now capturing about the same level of income as the bottom 90%. Now that households are deleveraging, political tensions triggered by rising inequality have increased. One of the ways these tensions have manifested themselves is through populism and rising economic nationalism.

Bretton Woods II or Weaponizing the Dollar

President Trump has called for a return of economic nationalism. He has aggressively implemented tariffs, arguably in the most aggressive fashion since the 1920s.

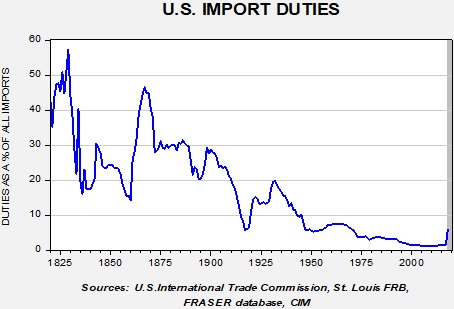

This chart shows that tariffs have become less popular over time; the decline in U.S. tariffs is consistent with other industrialized nations.1 However, it is worth noting that tariffs fell in the 1970s after currencies started to float. A big reason for this change was that tariffs are less effective under floating exchange rates because the tariff can be offset by adjustments in exchange rates. In other words, the country applying the tariff will usually see its currency appreciate; the level of appreciation will weaken the impact of the tariff on trade flows.

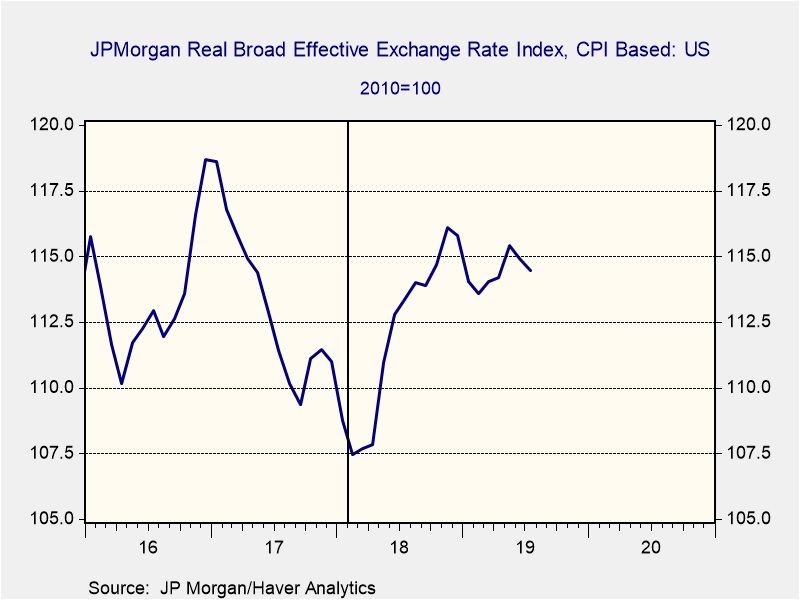

In late January 2018, the Trump administration implemented new tariffs on washing machines and solar panels and signaled that further action was likely. Note how the dollar has appreciated since this action has taken place, represented by the vertical line on the chart below.

As the dollar has risen, the White House has become actively opposed to dollar strength and has vigorously “jawboned” for a weaker dollar. However, these comments have not been able, so far, to bring a weaker greenback.

The president has made it clear that he wants to reduce the level of globalization and improve the lot of middle-class workers who have tended to bear the brunt of trade competition. However, for the reserve currency nation, this goal is difficult to achieve because the whole world has an incentive to run a trade surplus with it to gain dollars. Faced with trade impediments, these countries will reduce their profit margins and depreciate their currencies to maintain market share.

There has been a steady chorus questioning the suitability of floating exchange rates coming from supply-side economists in the administration. Also notable is that Judy Shelton, one of the candidates for Federal Reserve governor, seems to support a return to fixed exchange rates. At the same time, the president has been sharply and publicly criticizing the Federal Reserve’s monetary policy, calling for a large drop in interest rates. It is not uncommon for presidents to be critical of monetary policy; the Federal Reserve represents career risk for presidents in that overly tight monetary policy usually results in recessions. As noted last week, the last incumbent party or president to win during a recession was Calvin Coolidge.

However, it is arguable that talk of returning to fixed exchange rates and easier monetary policy have a common theme. Again, returning to the Impossible Trinity, what could be developing is Bretton Woods II:

- Fixed exchange rates

- Regulated central bank

- Open capital markets

There are no signs that the administration is considering capital controls. If the White House wants fixed exchange rates and open capital markets, the only workable resolution is to end Federal Reserve independence.

If this policy were to be implemented, the dollar would be fixed against a basket of currencies and the central bank’s only goal would be to maintain that peg. The central bank’s balance sheet would either expand or contract based upon whatever was necessary to maintain the peg.

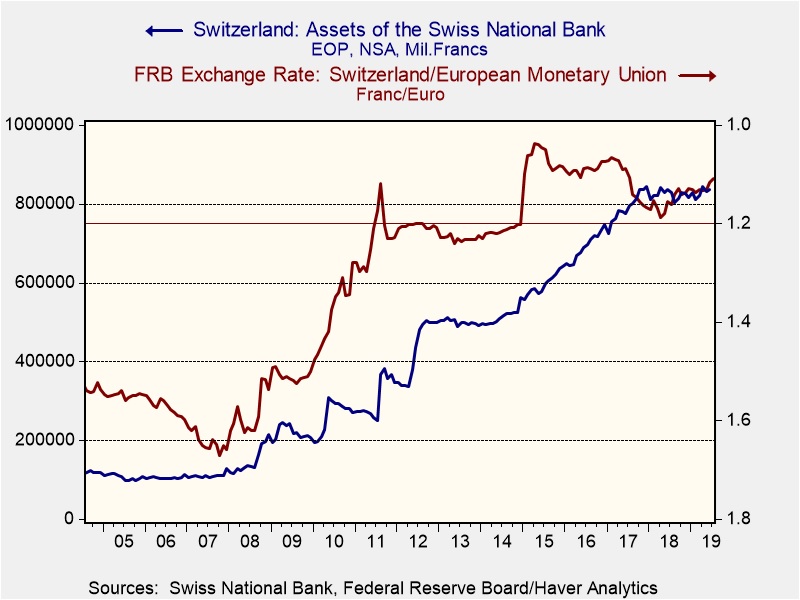

Although this situation may seem far-fetched, this is what the Swiss National Bank (SNB) did from 2011 into 2014. Alarmed at the steady appreciation of the CHF caused by flight-to-safety buying during the PIIGS2 debt crisis in 2010, Swiss authorities became concerned that the strength of the currency would adversely affect export competitiveness. As a result, on September 6, 2011, the SNB announced it would set a floor of 1.20 CHF/EUR. Essentially, the SNB would buy EUR with no limit until the exchange rate weakened.

When the policy was initially implemented, the balance sheet expanded rapidly. However, as credibility in the peg rose, the SNB was able to maintain both balance sheet and exchange rate stability. Over time, it became politically untenable to support balance sheet expansion and the peg was lifted without warning in 2014, leading to a spike in the CHF/EUR exchange rate. A massive expansion of the balance sheet has been necessary to gradually weaken the exchange rate.

Obviously, if the U.S. were to implement a similar system, there would be two important issues to contend with. First, what would be the level of the peg(s)? If the goal is to narrow the trade deficit, to be effective, the peg will need to be low enough to prompt this change. Second, it is likely that foreign nations will react to this peg by attempting to lower their own interest rates and undermine the effectiveness of U.S. policy. Such a situation would create a “race to the bottom” in terms of monetary policy. Another likely reaction would be retaliatory trade barriers in the form of tariffs and quotas.

To some extent, such an exchange rate regime change would seem to be nearly impossible to implement unilaterally. But, if any nation is in a position to execute such a policy, the U.S. could. Because the dollar is the reserve currency and the U.S. Treasury is the reserve asset of choice, the rest of the world lacks an alternative. Therefore, to quote President Nixon’s Treasury Secretary John Connally, who was facing criticism for the weaker dollar after the closing of the gold window:

“It’s our currency but it’s your problem.”

Ramifications

The market ramifications from this action would be significant. An engineered depreciation would tend to boost inflation and there would be the potential for a rapid rise in long-duration interest rates since the Federal Reserve would no longer lean against rising prices. On the other hand, credit spreads might narrow due to the availability of credit. Gold prices would also likely benefit as would commodity prices, in general.

We would expect such policies to be popular, at least initially. Rising price levels would probably lead to nominal wage increases and faster spending. In addition, we would expect other nations to attempt to limit imports themselves; the disruption of foreign markets could be devastating to firms that have built their market success on managing long supply chains, but it could be very beneficial for companies that primarily focus on the domestic market.

What is the likelihood of such an outcome? It is difficult to determine but the chances appear to be rising. Political elites need to respond to the rise of populism and wide inequality. The change in policy we have described would force the Federal Reserve into aggressive stimulation.

There are clear downsides to this policy change. If inflation expectations become unanchored, inflation will be hard to contain. And, if the dollar loses its reserve status, the Federal Reserve could find itself in a situation where it is being forced to tighten monetary policy to maintain what looked like initially depressed peg levels. Once confidence in the dollar is lost, stabilizing the economy could become very difficult. This policy change is risky, but what is currently in place isn’t politically sustainable. In this report, we have attempted to offer a potential path for resolving the inequality issue.

Bill O’Grady

August 19, 2019

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

1 The gray area of the chart represents the estimate if the tariffs on all Chinese imports are implemented. https://twitter.com/samro/status/1016467951254458368

2 Portugal, Ireland, Italy, Greece and Spain.

© Confluence Investment Management

More Alternative Investments Topics >