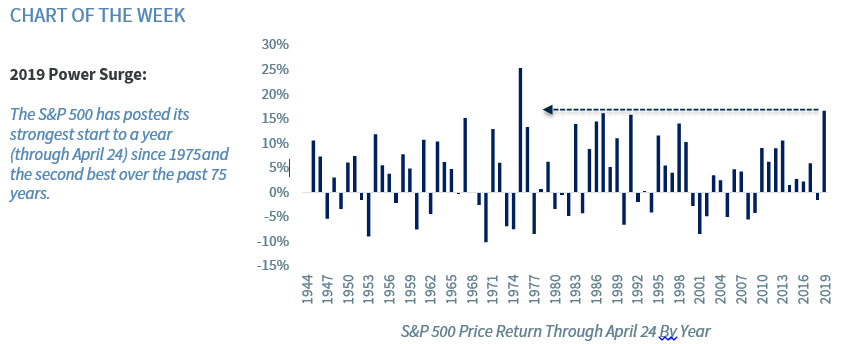

On the back of 1Q19 solid earnings results and healthy economic data releases, the S&P 500 continued its remarkable move higher this week and closed at a record high (2,933) for the first time since September 2018. To put the strength of the rally into perspective, the S&P 500 is now up 17.5% year-to-date through April 24, which marks the best start to a year since 1975 and the second best over the last 75 years. In addition, with the S&P 500 up ~25% since the Christmas Eve bottom, it is in the 99.6 percentile relative to all other time periods over the past 30 years. This means that the S&P 500 has experienced a stronger 87 trading-day rally (the number of trading days between Christmas Eve until present) only 0.4% of the time. Given the robust rally, it would not be surprising to see a near-term pause in the equity rally or a brief consolidation as the 14 day RSI (relative strength index) rose into overbought territory (a level above 70) and to its highest level (73) since January 2017. Despite this, we remain constructive on the equity market longer term and would use any near-term weakness as a buying opportunity for the following five reasons:

- Solid Macro Environment | This morning’s strong reading on 1Q19 GDP* (+3.2%, well above the previous 10 first quarters which averaged +1.1%) and the solid economic data points received thus far for the second quarter (e.g., retail sales and manufacturing surveys) reflect continued above trend economic growth (2019 U.S. GDP forecast: +1.9%) with little risk of recession over the next 12 months. This, in conjunction with the stabilization in global economic momentum following a potential U.S./China trade deal, should provide an attractive environment for equities and risk assets to continue to move higher.

- Fed on the Sideline | The Federal Reserve (Fed) has signaled that it will end its balance sheet run-off process in September and remain on the sideline in 2019 (consistent with our view of zero rate hikes for 2019). In addition, the Fed has insinuated that it may allow both the economy and inflation to run “hotter” before raising interest rates. Lower interest rates should lead to a higher multiple on equity prices and support their upward trajectory.

- Earnings Stabilization | Following the sharp downward revision to future earnings expectations over recent months, 2019 (+4.3%) and 2020 (+11.3%) earnings forecasts have stabilized in recent weeks and have actually started to move higher as we have had a strong start to the 1Q19 earnings season. Record levels of earnings and positive earnings growth going forward should continue to push U.S. equities to all-time highs.

- Favorable Shareholder Activity | After rising ~10% year-over-year (YoY) in 2018, dividends are expected to grow an additional 7% in 2019 to another record high. As the current S&P 500 dividend yield (+1.9%) remains elevated relative to short-term Treasury yields, U.S. equities remain an attractive investment. In addition, following a record amount of corporate buybacks over the last twelve months, buyback activity remains healthy.

- De-Equitization of the Equity Market | S. M&A activity is on pace to post the strongest year on record. As a result, the number of publically-listed U.S. companies is near the lowest level (~4,500) since the 1980s and is down ~50% from its mid-1990s peak. Given that there are now fewer companies for investors to buy, this provides upward pressure on U.S. equity prices. This is referred to as the “de-equitization” of the equity market.