In Part II, we discussed the principles and consequences of Modern Monetary Theory (MMT). This week’s installment will be devoted to the importance of paradigms. Next week, we will conclude the series with a discussion on the potential flaws of MMT along with market ramifications.

The Importance of Paradigms

Every major shift in the efficiency/equality cycle has coincided with a favored economic theory to promote the change. The following chart from Peter Turchin shows his take on inequality and wellbeing cycles in U.S. history. Although Turchin doesn’t fit his pattern to Arthur Okun’s equality and efficiency tradeoff,[1] we see a strong match between this tradeoff and Turchin’s wellbeing and inequality cycles. During periods where Turchin’s wellbeing line is rising and inequality is falling, the economy is going through an equality cycle. Equality cycles are sometimes characterized by policies that favor labor (which may include high marginal tax rates, easy monetary policy, policies that favor unions and social mores that promote “the common man”[2]).

Usually, equality cycles end when the economy needs to build productive capacity to reduce inflation and thus needs to increase efficiency. These are policies that favor capital, which may include low or non-existent tax rates, reduced regulation, anti-organized labor policies and social mores that lionize wealth.[3]

(Source: Peter Turchin[4])

Our historical analysis suggests there have been four shifts in equality and efficiency and each has been supported by an economic theory that gave intellectual credence to the shift.

Classical Economics and the Industrial Revolution. The Industrial Revolution was the original “move fast and break things.”[5] New technologies were applied to manufacturing, transportation and agriculture. The economics of Adam Smith to Alfred Marshall argued for limited government and suggested that self-interest, left unfettered, would lead to the best outcome for society. For the classical economists, the economy is self-regulating and thus outside influences, such as government, disrupt the natural rhythms of the market. One of the key theoretical constructs was “Say’s Law,” which argued that supply creates its own demand.[6] If prices can rise or fall to their correct level, then everything produced will be consumed. This means that resources will always be fully utilized. The period, which began around 1820 (in England) and continued into the early 20th century (as it spread to continental Europe, the U.S. and Japan), led to the building of the industrial base across the West and Japan. However, it also led to significant social ills and rising inequality.[7] Western nations attempted to deal with the inequality through expanding suffrage, implementing income taxes, child labor laws and antitrust legislation, but inequality remained high. The Great Depression marked the end of the Classical era and the Industrial Revolution.

The Great Depression and Keynesian Economics. The Great Depression led to a theoretical crisis in economics. Classical economists argued that the economy should be left alone, that government intervention was futile. As the downturn deepened, calls to let the market process work lost influence. But, to address what should be done, a new theory had to emerge. John Maynard Keynes developed a new theory,[8] arguing that the economy was not self-regulating because prices and wages were not fully flexible. Thus, Say’s Law didn’t always hold and the Classical theory of market self-regulation was undermined without Say’s Law.[9]

Keynes argued that aggregate demand in the economy can persist at a level less than full employment. He was especially concerned about the variability of investment, which he described as being driven by “animal spirits”[10] that can lead to booms and busts. Under these conditions, the government should step in and spend in order to lift growth during downturns and curtail growth in bubbles.

Keynesian economics changed economic policy. Governments introduced counter-cyclical policies, such as unemployment insurance and income taxes, to stabilize the economy. The Classical theory of an economy that self-regulated was replaced with the idea that the government should be an active participant in managing growth.

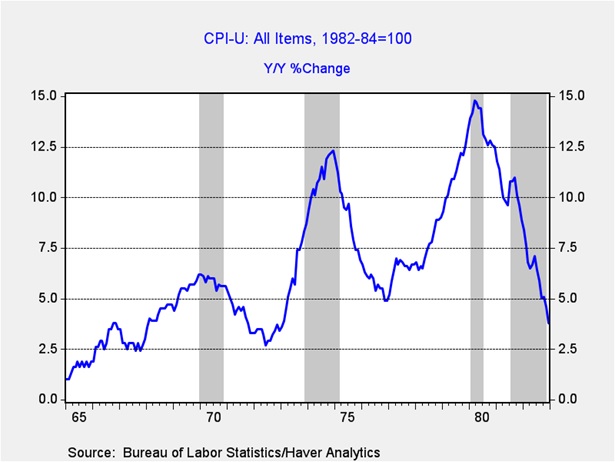

The Stagflation Crisis and Supply-Side Economics. By the mid-1960s, U.S. inflation had begun to rise. By 1971, conditions had deteriorated to the point where President Nixon implemented a price and wage freeze[11] and ended the postwar Bretton Woods arrangement by severing the dollar’s convertibility to gold. Inflation became a persistent problem in the 1970s and led to a crisis of confidence among economists. Stagflation, the combination of weak or declining economic growth and rising inflation, was thought to be impossible in a developed economy.

This chart shows the yearly change in CPI from the mid-1960s into the early 1980s. Note that inflation rose during recessions.

The response to this crisis was a combination of a neo-classical revival and a new economic theory called supply-side economics. Neo-classical economists built an argument called “rational expectations,” which postulated that actors in an economy anticipate policy actions and offset them. Thus, the only way that policy actions work is if they “fool” firms and consumers.

Rational expectations fit into the efficient market hypothesis that came out of academic finance. Essentially, rational expectations, if true, would mean that government policy can’t act to stabilize the economy and the Classical position that predated Keynes was correct after all.

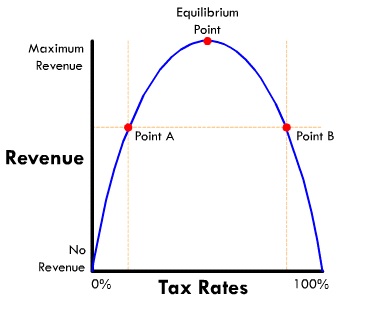

But, supply-side economics is what captured policy. It was a broad set of policies which, in contrast to Keynesian economics, focused on the aggregate supply curve. It suggested the reason stagflation occurred is that regulation had steepened and constrained the aggregate supply curve. The solution was to deregulate, which would help expand the curve (shift it to the right, using a Cartesian coordinate plane) and make the curve more elastic (flatten it). The most controversial part of the policy was that tax cuts were self-funding. Tax cuts would not lead to higher deficits but higher growth, which would boost tax revenue. Arthur Laffer’s tax curve became popular.

(Source: Wikipedia)

Laffer’s argument was that no revenue would be generated at a marginal rate of zero. However, none would be generated at 100% either because no one would work. He postulated that the marginal tax rate of 70% in the late 1970s was probably to the right of equilibrium, perhaps “point B” on the above chart. By cutting tax rates, revenue would increase.

In practice, cutting the marginal rate led to less revenue and higher deficits. But, cutting the marginal rate had other effects that likely did increase supply. Entrepreneurs had incentives to boost activity; there was a flurry of new technology firms that led to a plethora of new products.

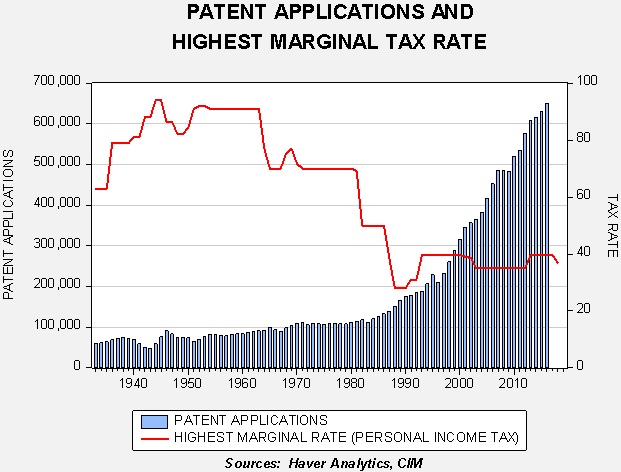

This chart shows patent applications and the highest personal marginal tax rate. Note that patent applications soared as the highest marginal tax rate declined. Essentially, the reward for new ideas increased as tax rates fell. Globalization became part of supply-side economics, which led to further declines in inflation.

The tradeoff with inflation control was a large increase in inequality. Household debt also rose to what became unsustainable levels. These factors contributed to the 2008 Great Financial Crisis (GFC). But, most importantly, the theory has become the rationale for low tax rates.

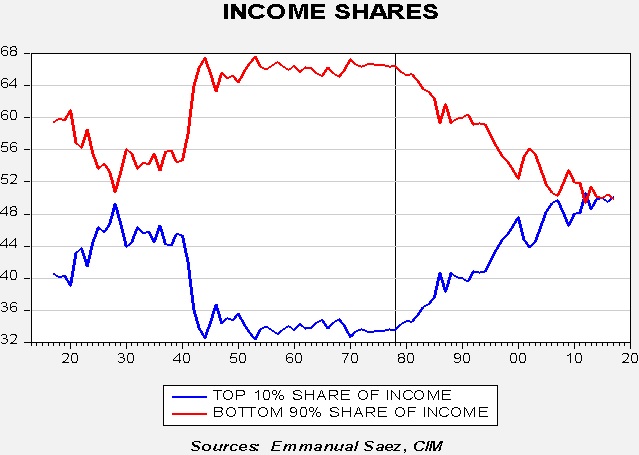

The Current Situation and MMT. There are three graphs that capture the current situation. First, income inequality has reached levels that are probably unsustainable.

This chart shows the shares of income captured by the top 10% of households compared to the bottom 90%. Currently, they are both about equal, meaning that the top 10% currently get about 50.1% of household income, while the bottom 90% get 49.9%. From an economic standpoint, one could argue that as long as the overall size of the economy is growing the distribution shouldn’t matter; however, with this skew, any growth to the bottom 90% is so diffused that the rate of expansion would need to be very strong for the vast majority of households to notice. Unfortunately, since 2008, U.S. economic growth has been sluggish.

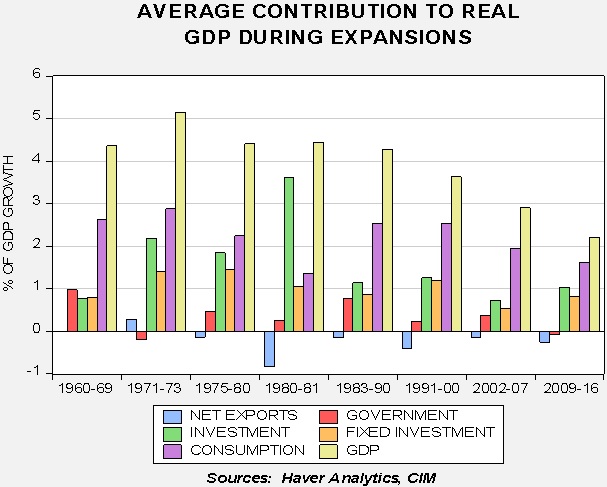

This chart shows the contributions to GDP during this expansion. The bar on the far right shows the average GDP growth during each expansion since 1960. As this chart shows, this has been the weakest growth during an expansion over the past nearly six decades. The other interesting item is that government spending has been a net drag on growth in this expansion, which, outside of war demobilization, is unprecedented during the time period shown.

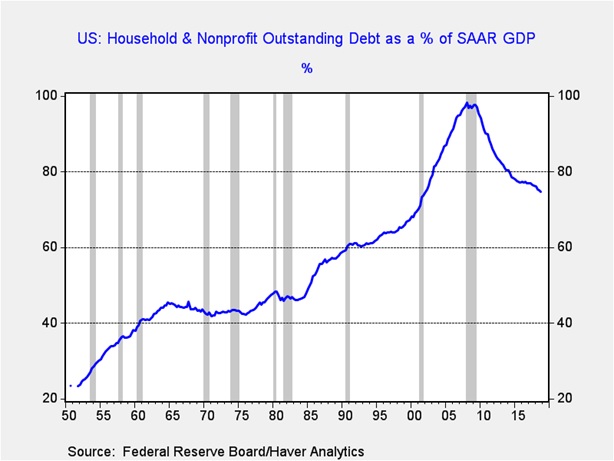

Third, households have been deleveraging during this expansion in the post-GFC period.

This chart shows household debt relative to GDP. During the period of supply-side economics, household debt rose at a rapid pace. There were a number of reasons for this accumulation. Credit deregulation made borrowing more accessible to households. New forms of lending technology, including mortgage securitization, fostered real estate borrowing and refinancing. Foreign desire for dollar reserves meant that foreign flows came into the U.S. Government and business dissaving only partly offset these flows; households steadily dissaved. And, finally, income inequality and easy credit encouraged households to take on debt to maintain lifestyles.

The GFC ended this borrowing. As households have delevered, their spending has fallen and the burden of debt workout has mostly fallen on borrowers. This development has led to social and political upheaval. The elections of both Barack Obama and Donald Trump were attempts by the voting public to address the above situation.

Up until this point, the problem was that both wings of the establishment had, more or less, adopted the supply-side argument. If spending were to increase, there was always the need to “pay” for it. This is where MMT enters the picture. High marginal tax rates on the wealthy are not needed for revenue.[12]

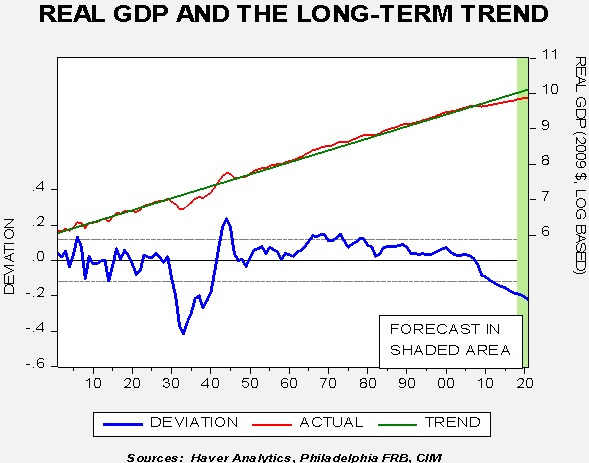

Another way of looking at the equality/ efficiency tradeoff is the trend in long-term GDP.

This chart shows the level of real GDP starting in 1901. We have log-transformed the data and regressed a time trend through it. Note the lower line on the chart which shows the deviation from the long-term trend. We are seeing deviations from trend similar to what we saw during the Great Depression. It should not be surprising that there is a rising trend in populism.

Part IV

Next week, we will conclude this series with an analysis of the flaws of MMT and market ramifications.

Bill O’Grady

March 25, 2019

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

© Confluence Investment Management LLC

|

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

|

|

[1] Okun, Arthur. (1975). Equality and Efficiency: The Big Tradeoff. Washington, D.C.: The Brookings Institution.

[2]https://en.wikipedia.org/wiki/You_Can%27t_Take_It_with_You_(film)

[3]https://www.youtube.com/watch?v=VVxYOQS6ggk

[4] http://peterturchin.com/cliodynamica/the-double-helix-of-inequality-and-well-being/

[5] Taplin, Jonathan. (2017). Move Fast and Break Things: How Facebook, Google, and Amazon Cornered Culture and Undermined Democracy. New York, NY: Little, Brown and Company.

[6]https://www.economicshelp.org/blog/glossary/says-law/

[7] Marx, Karl. Capital (Volume 1). New York, NY: Vintage Books, Random House (see especially chapter 15).

[8] Keynes, John Maynard. (1964). The General Theory of Employment, Interest and Money (First Harbinger Edition, first published 1936). New York, NY: Harcourt Brace Jovanovich.

[9] Ibid., pp.18-22.

[10] Ibid., pp.161-162

[11]https://en.wikisource.org/wiki/Executive_Order_11615

[12]https://www.bloomberg.com/opinion/articles/2019-02-01/rich-must-embrace-deficits-to-escape-taxes Although, as discussed above, they might be necessary in order to change corporate behavior.

© Confluence Investment Management

More Fixed Income Topics >