In a widely expected outcome, the Federal Reserve announced no change to the Fed funds rate but did leave open the possibility of a rate hike next year. Also, they committed to stopping “Quantitative Tightening (or Q.T.)” by the end of September.

The key language from yesterday’s announcement was:

“Information received since the Federal Open Market Committee met in January indicates that the labor market remains strong but that growth of economic activity has slowed from its solid rate in the fourth quarter. Payroll employment was little changed in February, but job gains have been solid, on average, in recent months, and the unemployment rate has remained low.

Recent indicators point to slower growth of household spending and business fixed investment in the first quarter. On a 12-month basis, overall inflation has declined, largely as a result of lower energy prices; inflation for items other than food and energy remains near 2 percent. On balance, market-based measures of inflation compensation have remained low in recent months, and survey-based measures of longer-term inflation expectations are little changed.”

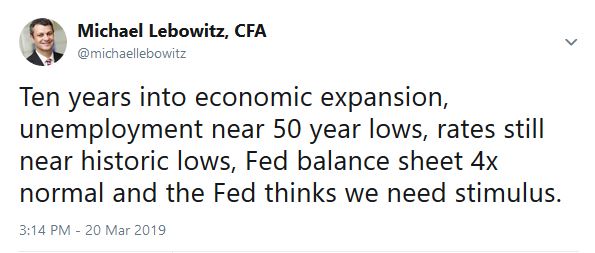

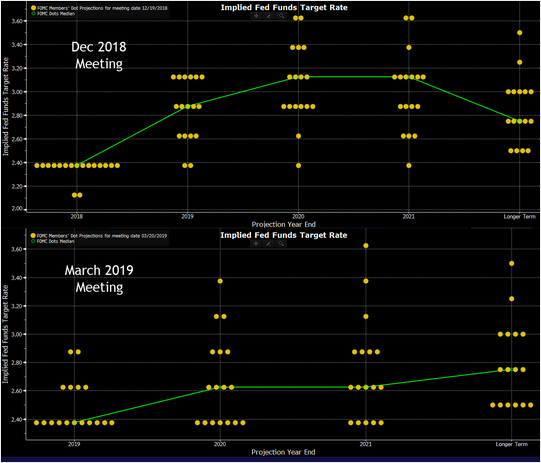

What is interesting is that despite the language that “all is okay with the economy,” the Fed has completely reversed course on monetary tightening by reducing the rate of balance sheet reductions in coming months and ending them entirely by September. At the same time, all but one future rate hike has disappeared, and the Fed discussed the economy might need easing in the near future. To wit, my colleague Michael Lebowitz posted the following Tweet after the Fed meeting:

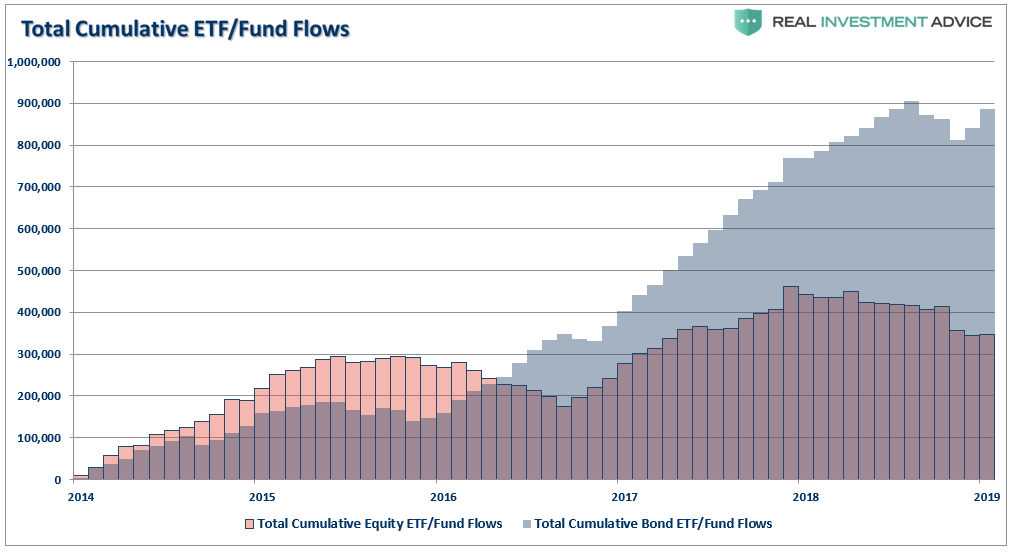

This assessment of a weak economy is not good for corporate profitability or the stock market. However, it seems as if investors have already gotten the “message” despite consistent headline droning about the benefits of chasing equities. Over the last several years investors have continued to chase “safety” and “yield.” The chart below shows the cumulative flows of both ETF’s and Mutual Funds in equities and fixed income.

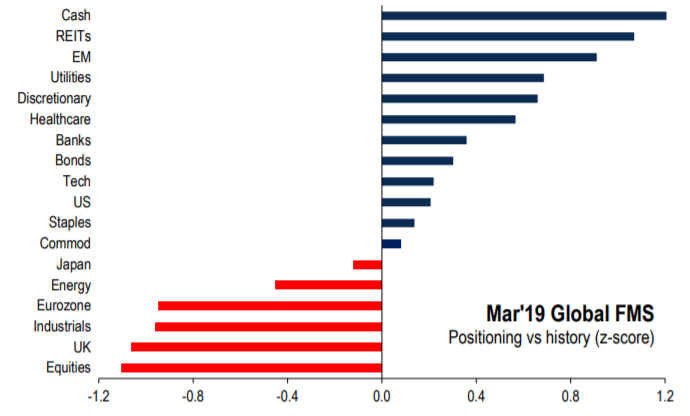

This chase for “yield” over “return” is also seen in the global investor positing report for March.

Clearly, investors have continued to pile into fixed income and safer equity income assets over the last few years despite the sharp ramp up in asset prices. This demand for “yield” and “safety” has been one of the reasons we have remained staunchly bullish on bonds in recent years despite continued calls for the “Death of the Bond Bull Market.”

The Reason The Bond Bull Lives

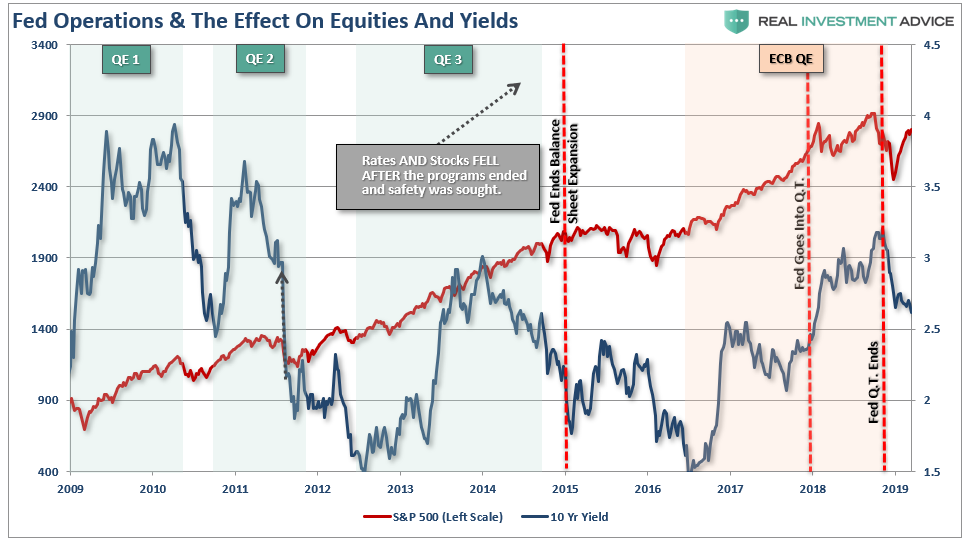

Importantly, one of the key reasons we have remained bullish on bonds is that, as shown below, it is when the Fed is out of the “Q.E” game that rates fall. This, of course, was the complete opposite effect of what was supposed to happen.

Of course, the reasoning is simple enough and should be concerning to investors longer-term. Without “Q.E”support, economic growth stumbles which negatively impacts asset prices pushing investors into the “safety” of bonds.

As the Fed now readily admits, their pivot to a more “dovish” stance is due to the global downturn in economic growth, and the bond market has been screaming that message in recent months. As Doug Kass noted on Tuesday:

“Which brings me to today’s fundamental message of the fixed income markets – which are likely being ignored and could be presaging weakening economic and profit growth relative to consensus expectationsand, even (now here is a novel notion) that could lead to lower stock prices. That message is undeniable – economic and profit growth is slowing relative to expectations as financial asset prices move uninterruptedly higher.

- The yield on the 10 year U.S. note has dropped below 2.60% this morning. (I have long had a low 2.25% forecast for 2019)

- The (yield curve and) difference between 2s and 10s is down to only 14 basis points.

- High-frequency economic statistics (e.g. Cass Freight Index) continue to point to slowing domestic growth.

- Auto sales and U.S. residential activity are clearly rolling over.

- PMIs and other data are disappointing.

- Fixed business investment is weakening.

- No country is an economic island – not even the U.S.

- Europe is approaching recession and China is overstating its economic activity (despite an injection of massive amounts of liquidity).”

He is correct, yields continue to tell us an important story.

First, three important facts are affecting yields now and in the foreseeable future:

- All interest rates are relative. With more than $10-Trillion in debt globally sporting negative interest rates, the assumption that rates in the U.S. are about to spike higher is likely wrong. Higher yields in U.S. debt attracts flows of capital from countries with negative yields which push rates lower in the U.S. Given the current push by Central Banks globally to suppress interest rates to keep nascent economic growth going, an eventual zero-yield on U.S. debt is not unrealistic.

- The coming budget deficit balloon. Given the lack of fiscal policy controls in Washington, and promises of continued largess in the future, the budget deficit will eclipse $1 Trillion or more in the coming years. This will require more government bond issuance to fund future expenditures which will be magnified during the next recessionary spat as tax revenue falls.

- Central Banks will continue to be a buyer of bonds to maintain the current status quo. As such they will have to be even more aggressive buyers during the next recession. The next QE program by the Fed to offset the next economic recession will likely be $2-4 Trillion and might push the 10-year yield towards zero.

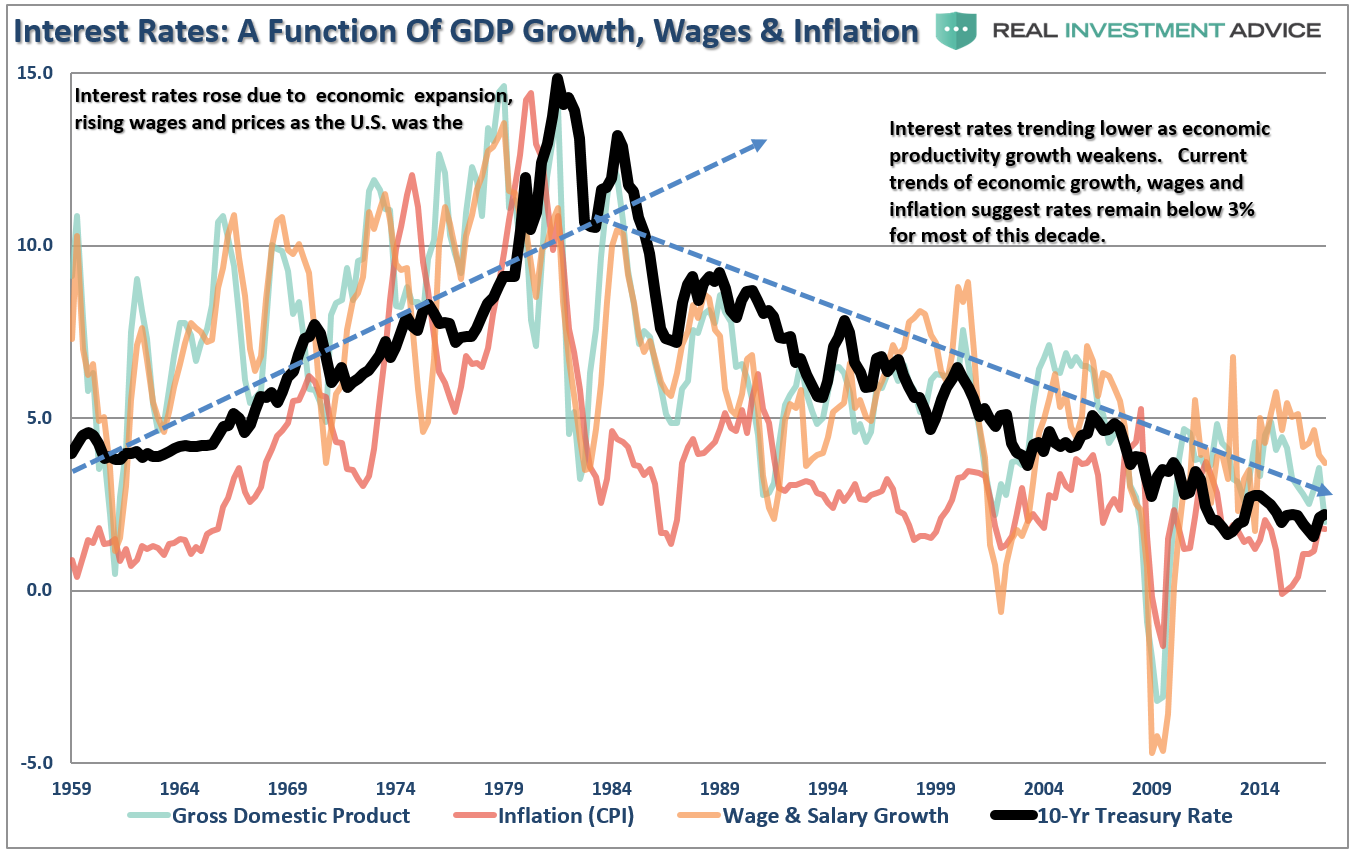

As I have discussed many times in the past, interest rates are a function of three primary factors: economic growth, wage growth, and inflation. The relationship can be clearly seen in the chart below.

Okay…maybe not so clearly.

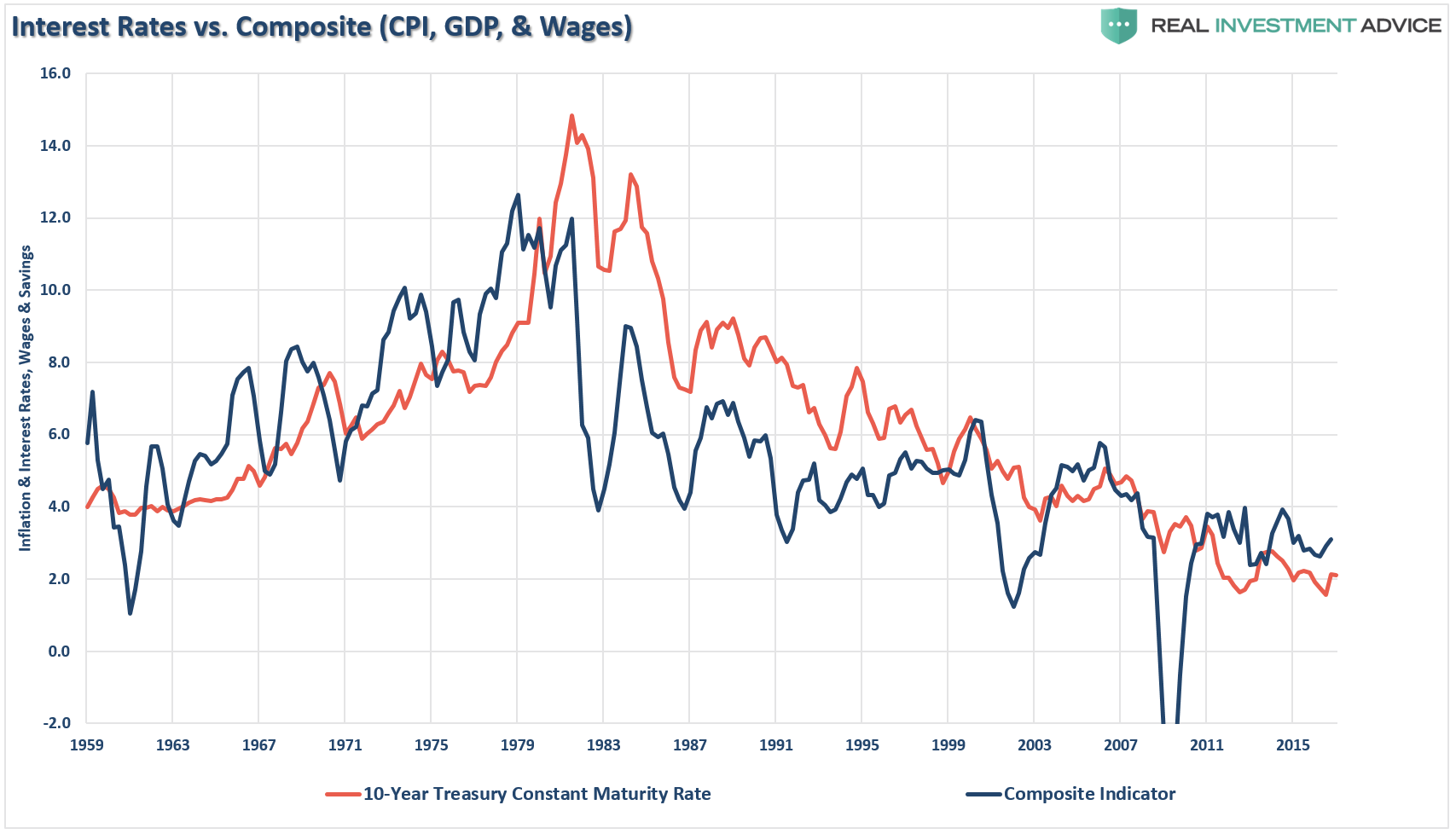

Let me clean this up by combining inflation, wages, and economic growth into a single composite for comparison purposes to the level of the 10-year Treasury rate.

As you can see, the level of interest rates is directly tied to the strength of economic growth, wages and inflation. This should not be surprising given that consumption is roughly 70% of economic growth.

As Doug notes, the credit markets have been right all along the way. At important points in time, when the Fed signaled policy changes, credit markets have correctly interpreted how likely those changes were going to be. A perfect example is the initial rate hike path set out in December 2015 by then Fed Chairman Janet Yellen. This was completely wrong at the time and the credit markets told us so from the beginning.

The credit markets have kept us on the right side of the interest rate argument in repeated posts since 2013. Why, because the credit market continues to tell us an important story if you are only willing to listen.

The bond market is screaming “secular stagnation.”

Since 2009, asset prices have been lofted higher by artificially suppressed interest rates, ongoing liquidity injections, wage and employment suppression, productivity-enhanced operating margins, and continued share buybacks have expanded operating earnings well beyond revenue growth.

As I wrote in mid-2017:

“The Fed has mistakenly believed the artificially supported backdrop they created was actually the reality of a bright economic future. Unfortunately, the Fed and Wall Street still have not recognized the symptoms of the current liquidity trap where short-term interest rates remain near zero and fluctuations in the monetary base fail to translate into higher inflation.

Combine that with an aging demographic, which will further strain the financial system, increasing levels of indebtedness, and lack of fiscal policy, it is unlikely the Fed will be successful in sparking economic growth in excess of 2%. However, by mistakenly hiking interest rates and tightening monetary policy at a very late stage of the current economic cycle, they will likely be successful at creating the next bust in financial assets.”

It didn’t take long for that prediction to come to fruition and change the Fed’s thinking.

On December 24th, 2018, while the S&P 500 was plumbing it’s depths of the 2018 correction, I penned “Why Gundlach Is Still Wrong About Higher Rates:”

“At some point, the Federal Reserve is going to step back in and reverse their policy back to “Quantitative Easing” and lowering Fed Funds back to the zero bound.

When that occurs, rates will not only go to 1.5%, but closer to Zero, and maybe even negative.”

What I didn’t know then was that literally the next day the Fed would reverse course.

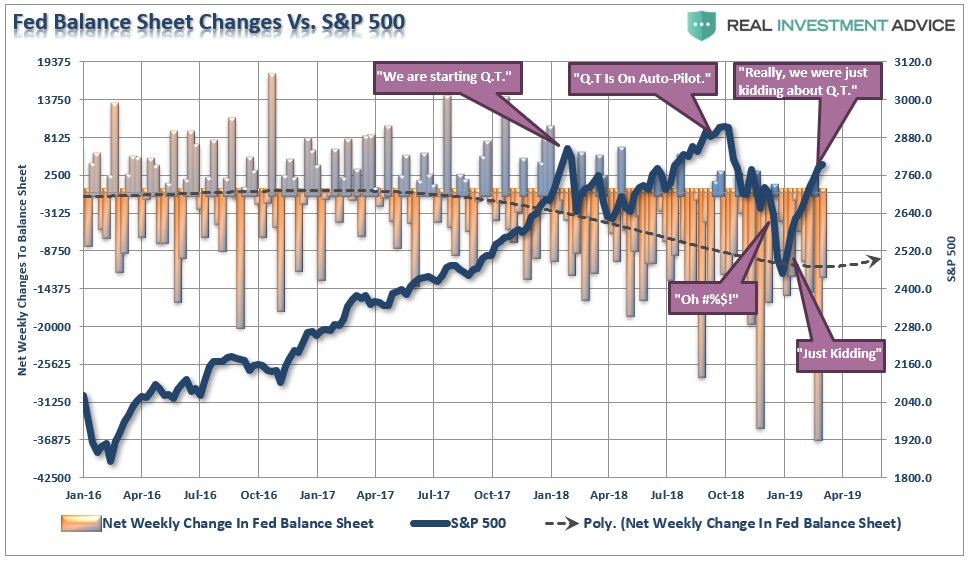

The chart below shows the rolling 4-week change in the Fed’s balance sheet versus the S&P 500.

The issue for the Fed is that they have become “market dependent” by allowing asset prices to dictate policy. What they are missing is that if share prices actually did indicate higher rates of economic growth, not just higher profits due to stock buybacks and accounting gimmickry, then US government bond yields would be rising due to future rate hike expectations as nominal GDP would be boosted by full employment and increased inflation. But that’s not what’s happening at all.

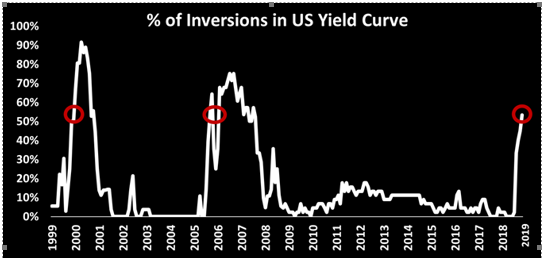

Instead, the US 10-year bond is pretty close to 2.5% and the yield curve is heading into inversion.

Since inversions are symptomatic of weaker economic growth, such would predict future rate hikes by the Fed will be limited. Not surprisingly, that is exactly what is happening now as shown by yesterday’s rapid decline in the Fed’s outlook.

Why?

Let’s go back to that 2017 article:

“However, the issue of rising borrowing costs spreads through the entire financial ecosystem like a virus. The rise and fall of stock prices have very little to do with the average American and their participation in the domestic economy. Interest rates are an entirely different matter.

Since interest rates affect ‘payments,’ increases in rates quickly have negative impacts on consumption, housing, and investment which ultimately deters economic growth.”

All it took was for interest rates to crest 3% and home, auto, and retail sales all hit the skids. Given the current demographic, debt, pension, and valuation headwinds, the future rates of growth are going to be low over the next couple of decades – approaching ZERO.

While there is little left for interest rates to fall in the current environment, there is also not a tremendous amount of room for increases. Therefore, bond investors are going to have to adopt a “trading” strategy in portfolios as rates start to go flat-line over the next decade.

Whether, or not, you agree there is a high degree of complacency in the financial markets is largely irrelevant. The realization of “risk,” when it occurs, will lead to a rapid unwinding of the markets pushing volatility higher and bond yields lower. This is why I continue to acquire bonds on rallies in the markets, which suppresses bond prices, to increase portfolio income and hedge against a future market dislocation.

In other words, I get paid to hedge risk, lower portfolio volatility and protect capital.

Bonds aren’t dead, in fact, they are likely going to be your best investment in the not too distant future.

“I don’t know what the seven wonders of the world are, but the eighth is compound interest.” – Baron Rothschild

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

© Real Investment Advice

© Real Investment Advice

Read more commentaries by Real Investment Advice