Ned Davis wrote the book “Being Right or Making Money” in 1991. We mention it this morning, because we are doing a conference call today with Ned at 10:00 a.m. (register here). As most of you know, Ned is one of the best on Wall Street. The book resides on my desk, because I often refer to it. In the introduction Ned writes (referring to himself):

"If you are so smart, why aren’t you rich? It was at about that time (1978-1980) that I began to realize that smarts, hard work, and even a burning desire to 'be right' were really not my problem, nor the solution to my problem. What I realized was that my real problems were a failure to cut losses short, an inability to be disciplined, difficulty admitting mistakes, fear and greed, and a lack of risk management, none of which had much to do with being right in the stock market world. It was thus a lack of proper investment strategy, not forecasting, that was holding me back. So I set out to get a computer and a good program, and started building timing models that I felt would give me the objectivity, discipline, flexibility, and risk management that I needed to make consistent profits. And since 1980, my company Ned Davis Research, Inc. has been dedicated to building timing models that do not forecast, are designed to make money."

Gosh, if that sounds like me, it should, because that is what I try to do. As my father used to tell me, "Son, if you think the stock market is going up, be bullish. If you think it is going down, be bearish. But for gosh sakes make a call, because there too many pundits in this business that talk out of both sides of their mouths so that no matter what the stock market does they can say, “See I told you that was going to happen.”

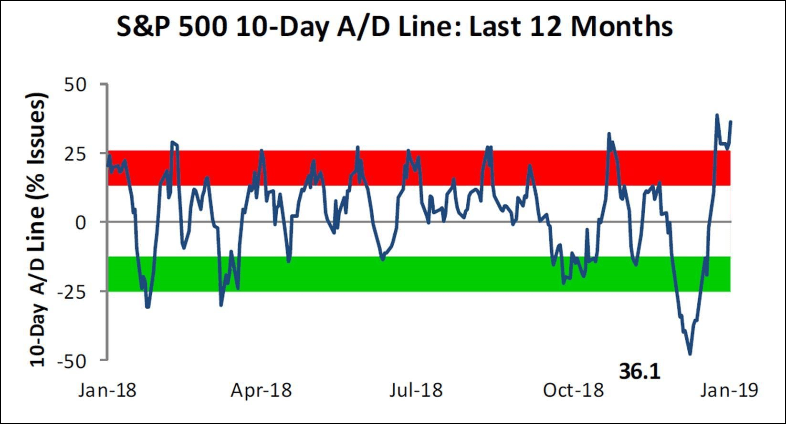

Ladies and gentlemen, if you draw a line in the sand, and make a call, you are going to be wrong and a lot more often than you think. To that point, I have been bullish since the selling climax low of December 24. My initial upside short-term target zone for the S&P 500 (SPX/2670.71) was 2600-2650, which I did not think would be eclipse on the current rally. I was wrong, as the evidential good news on the Chinese trade talk vaulted the SPX above 2670 last Friday. The “buying stampede” is now on session 18 in what is typically a 17-25 session upside skein with only one- to three-session pauses/pullbacks. The rally has left a number of finger-to-wallet ratios pretty overbought in the near term (Chart 1, page 2).

So how do you invest for 2019? To that point, our Chief Investment Officer, Larry Adam, conducted an excellent webinar last week on 10 Investment Themes for 2019. To wit:

-

- The Economy. [The] expansion to notch record duration in July and continue to grow at an (albeit slower) above-trend growth pace.

- Fed Policy. [The] Fed will remain data-dependent and flexible as inflation is contained and growth challenges mount.

- Increased Volatility. The low probability of a recession should provide more opportunities for risk assets investors and more chances for active managers to outperform.

- Bond Market. While a healthy economy and “quantitative tightening” should place upward pressure on interest rates, higher yields and spreads make bonds incrementally more attractive. The 10-year Treasury is unlikely to achieve a sustainable yield above 3.5%. With short-term rates likely to move higher, cash is now a viable alternative.

- Equities. U.S. corporate earnings should move higher on the back of modest economic growth, solid corporate confidence, and buybacks.

- Sector Selection. Leverage to economic growth, superior earnings growth, attractive valuations, higher shareholder value dynamics (e.g., dividend growth and buybacks) and less sensitivity to rising interest rates encourage us to continue to favor cyclical sectors.

- International Intrigue. While attractively valued, developed international markets may continue to struggle as political drama intensifies. EM markets, particularly Asian EM, could benefit from a trade deal, less aggressive Fed policy, and the stabilization of the dollar.

- Dollar Direction. A less aggressive Fed, less upside surprise potential of the U.S. economy, and the fading of some European political risks favor a more stable euro.

- Oil. The recent pullback in oil prices should begin to reduce output as producers become disincentivized. Market forecasted to become undersupplied.

The call for this week: According to the astute Lowry’s Research:

"Prior commentaries have noted that the advance from the December 24th 2018 market low has included several rare events that have, historically, been associated with very strong rallies. Up Volume on the initial rally off the December 24th low, on December 26th, was 96.4% of total Up/Down Volume, while Points Gained was 98% of total Points Gained/Points Lost. This was the first 90% Up Day since November 2016 and suggested a level of Demand historically associated with the start of important rallies. The rebound was further augmented by another 90% Up Day on January 4th 2019. This is where the truly rare market events began."

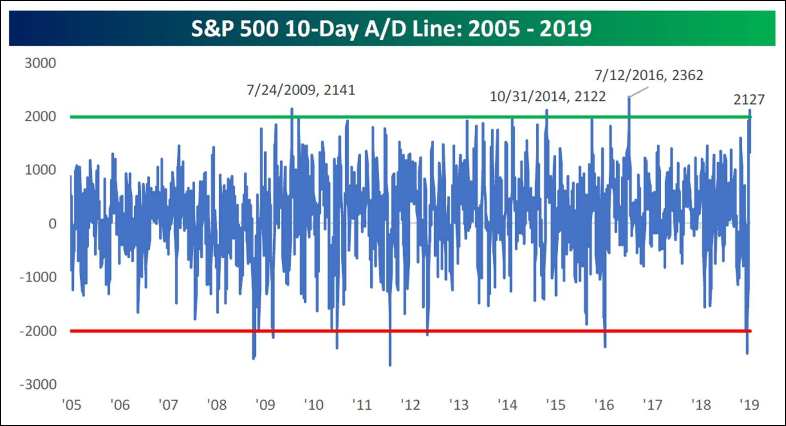

That said, in the short term, the equity markets have gone from extremely oversold to extremely overbought in one of the shortest times in history (Chart 2, page 3). Therefore, even though the SPX has exceeded our upside target range (2600-2650), we are sticking with our more cautious investment stance at these levels. You will hear more about this on today’s conference call with Ned Davis.

Chart 1

Click here to enlarge

Source: Bespoke Investment Group, Inc.

Chart 2

Click here to enlarge

Source: Bespoke Investment Group, Inc.

Additional information is available on request. This document may not be reprinted without permission.

Raymond James & Associates may make a market in stocks mentioned in this report and may have managed/co-managed a public/follow-on offering of these shares or otherwise provided investment banking services to companies mentioned in this report in the past three years.

RJ&A or its officers, employees, or affiliates may 1) currently own shares, options, rights or warrants and/or 2) execute transactions in the securities mentioned in this report that may or may not be consistent with this report’s conclusions.

The opinions offered by Mr. Saut should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your Raymond James Financial Advisor.

All expressions of opinion reflect the judgment of the Equity Research Department of Raymond James & Associates at this time and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the material presented is accurate or that it provides a complete description of the securities, markets or developments mentioned. Other Raymond James departments may have information that is not available to the Equity Research Department about companies mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this presentation’s conclusions. We may perform investment banking or other services for, or solicit investment banking business from, any company mentioned. Investments mentioned are subject to availability and market conditions. All yields represent past performance and may not be indicative of future results. Raymond James & Associates, Raymond James Financial Services and Raymond James Ltd. are wholly-owned subsidiaries of Raymond James Financial.

International securities involve additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

Investors should consider the investment objectives, risks, and charges and expenses of mutual funds carefully before investing. The prospectus contains this and other information about mutual funds. The prospectus is available from your financial advisor and should be read carefully before investing.

© Raymond James

© Raymond James

Read more commentaries by Raymond James