SUMMARY

- Our baseline expectation of a recession in the U.S. over our secular horizon makes for a concerning backdrop for Canada’s economy, but the rudest awakening facing Canada is likely a domestic one: Over-indebted consumers, no longer supported by ever-rising home prices, may cease to be the driver of real GDP growth.

- That said, we do not expect a U.S.-style housing correction in Canada, given our view that mortgage underwriting is much stronger than it was in the U.S. before the crisis and that Canada has not overbuilt relative to growth in household formation.

- If consumption and residential investment lag consensus forecasts (our base case), we believe terminal levels of interest rates will be lower than in past business cycles.

- We expect to see steeper Canadian yield curves, as the front end remains anchored by the Bank of Canada, but term rates may rise for some time as U.S. rates respond to Fed moves and deficit-financed fiscal stimulus.

What do the next three to five years have in store for Canada’s economy? PIMCO’s recent 2018 Secular Outlook, “Rude Awakenings,” summarizes our global outlook over this horizon – including our baseline expectation of a recession in the U.S. We believe a recession would likely be shallower than a standard post-World War II recession, as there are few signs of overinvestment and overconsumption in the U.S. economy. But it may well be longer and riskier, as lower starting levels of interest rates, a bloated central bank balance sheet and larger fiscal deficit limit the policy space to fight it.

This makes for a concerning backdrop, given that the U.S. is Canada’s largest trading partner, accounting for about 25% of Canadian GDP. Yet we believe the rudest awakening facing Canada is likely a domestic one: Over-indebted consumers, no longer supported by ever-rising home prices, may cease to be the driver of real GDP growth in Canada.

Is Canada’s growth engine breaking down?

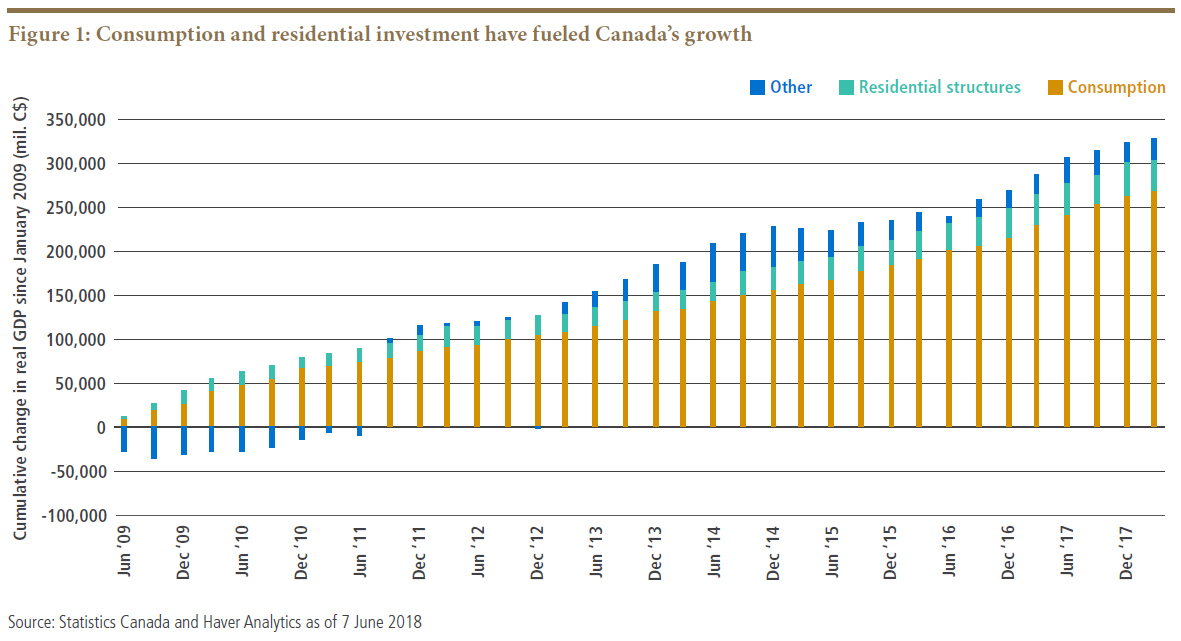

Consumption and residential investment have accounted for more than 92% of Canada’s real GDP growth since the global financial crisis (see Figure 1), against an average of approximately 80% for the previous 25 years. By borrowing more and more money at ever-lower interest rates, over-indebted consumers have propelled the Canadian economy forward.

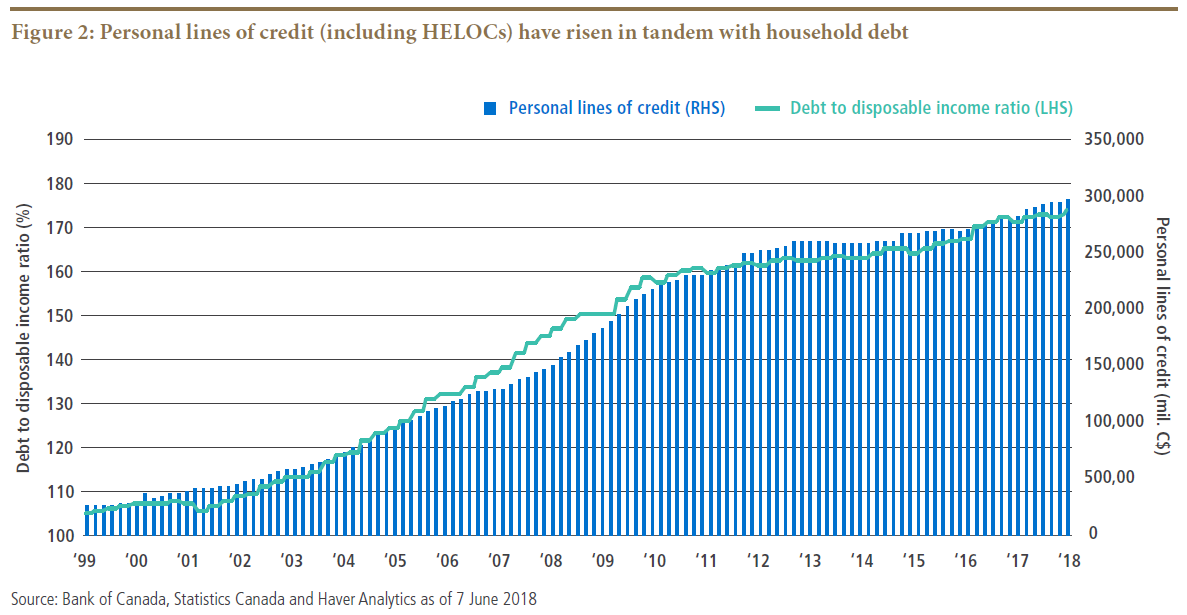

Looking out over our three- to five-year secular horizon, we do not believe this growth model is sustainable. Just as our American friends did before the crisis, Canadians have essentially used their homes like piggy banks (if not to the same degree, or in exactly the same way) by refinancing their mortgages and taking out home equity lines of credit (HELOCs) (see Figure 2). For example, by converting a standard 25-year amortizing, five-year fixed-rate mortgage at 3.29% to an interest-only HELOC at 3.95%, a borrower can reduce the monthly payment by over 30% (the monthly payment on a $100,000 mortgage would drop from C$489 per month to C$329 in this scenario). So, banks get higher rates on their loans, and consumers have more disposable income to spend – but borrowers generally do not pay down the loans, leaving them less prepared for their retirement. No wonder HELOCs have become so popular while at the same time raising concerns among policymakers.

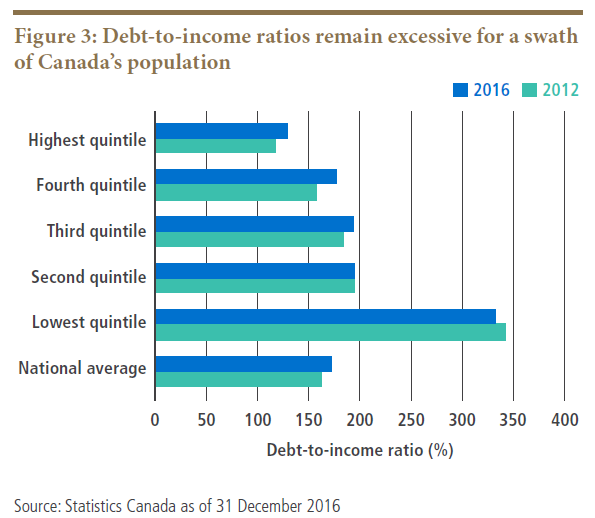

This increased debt burden has fueled higher home prices and consumption. To be clear, not all Canadians embody this trend. However, the Bank of Canada has found that for 20% of Canadians, debt exceeded annual income by more than three times in 2016 (see Figure 3). While this number has improved slightly since 2012, these vulnerable Canadians are likely still not prepared for the shock to their income that could result either from a U.S. recession (and its impact on many parts of the Canadian economy), or from a sharp rise in interest rates and debt servicing costs. Unlike in the U.S., where most borrowers lock in interest rates for 30 years, Canadians must refinance their mortgages every five years, thus resetting their interest payments.

This is the main reason we believe the Bank of Canada, despite a likely desire to cool an overheating market, may not be able to normalize (i.e., hike) interest rates to the same degree and pace as the U.S. Federal Reserve. Our consumers and housing markets simply cannot handle substantially higher interest rates. It is also why the bank has focused on macroprudential measures, such as the Office of the Superintendent of Financial Institutions (OSFI) B-20 rules implemented recently, aimed to tighten and improve credit underwriting.

Canada should sidestep a U.S.-style housing bust

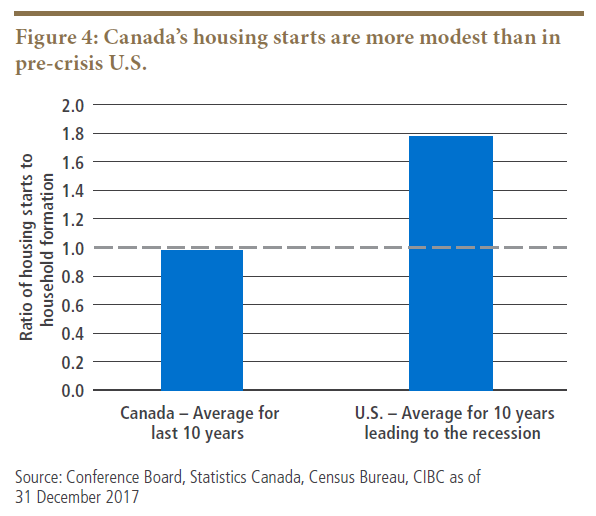

All this being said, we do not expect a U.S.-style housing correction, for two main reasons. One, we view underwriting for the Canadian mortgage market in 2018 as much stronger than it was for the U.S. market in 2006 and 2007: There is no widespread mortgage fraud, most loans have recourse, and so forth. Two, Canada has not over-built relative to growth in household formation, as the U.S. did (see Figure 4).

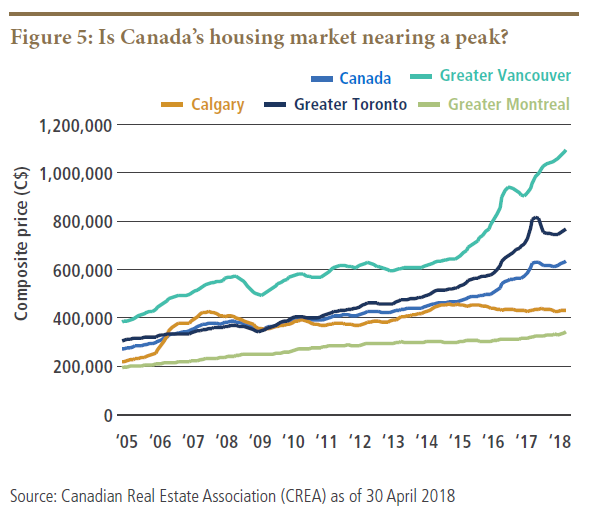

Some readers may recall that we thought Canadian housing prices (see Figure 5) were close to peaking back in 2011. That is a fair point: Calling the top of a market is tough. The main factor upending our view then was that rates did not gently rise, as we had expected, but in fact fell 150 basis points over the subsequent five years. Meanwhile, in the past two years, five-year rates have risen over 150 basis points, which should start to influence consumers as they face higher monthly payments at first refinancing. Moreover, policymakers are now being more aggressive about tightening mortgage credit, with stress-test rules that have started to cut into the amount of borrowing in 2018.

A more muted baseline view over the secular horizon

As a result of these many headwinds, our secular base case view for growth is more muted than the 2.0%–2.5% range we have witnessed over the past several years. Indeed, if the contribution of consumption and residential investment alone were to revert to long-term averages, it would imply a reduction of about a quarter to a half point from growth annually, relative to the recent past. The deceleration could be even greater if we were to see a period of below-trend activity as households consolidate their balance sheets.

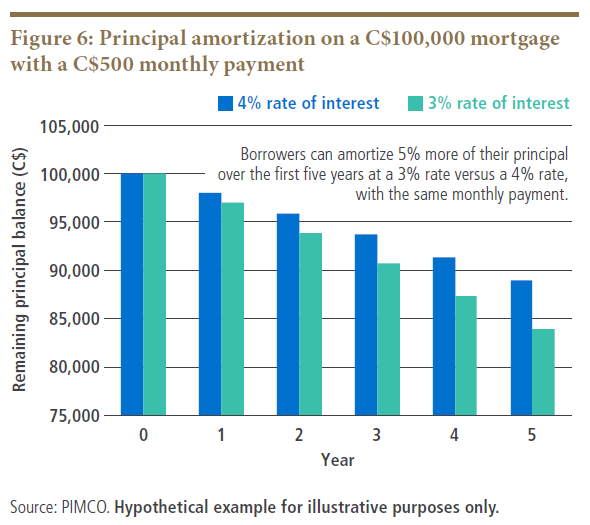

With all baseline forecasts, there are risks on both sides. The upside risks for the Canadian economy are that growing investment leads to job growth and higher incomes, which in turn offset the cost of paying higher interest rates. A relatively tight labor market seems to be firming up wages. Moreover, commodity prices, especially oil, have risen substantially from 2016 levels and are supporting stronger nonresidential investment in certain sectors of the economy. Additionally, one key benefit of the low rates of the past few years is that borrowers have been paying down their loans faster than when rates were higher (see Figure 6). This can help offset home price declines.

The downside risks to our base case seem a bit more severe. They include economic shocks arising from a severe housing price correction (which would exacerbate the trends noted above) or emanating from trade and geopolitical events.

Investment implications

We believe the Bank of Canada understands the consumer debt issues facing the country and will be very cautious during the current rate-hiking cycle. If consumption and residential investment lag consensus forecasts (our base case), we believe terminal levels of interest rates will be lower than in past business cycles. Lower Canadian interest rates would likely put some pressure on the Canadian dollar, which is also likely to face short-term pressure from trade uncertainty. Moreover, we expect to see steeper Canadian yield curves, as the front end remains anchored by the Bank of Canada, but term rates may rise for some time as U.S. rates respond to Fed moves and deficit-financed fiscal stimulus.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. There is no guarantee that results will be achieved.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

This material contains the current opinions of the manager and such opinions are subject to change without notice. This material is distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

© PIMCO

© PIMCO

Read more commentaries by PIMCO