In a reversal from last year, the U.S. dollar has strengthened against other major currencies in 2018, reflecting rising U.S. rates, expectations of more Federal Reserve rate hikes and recent sluggish economic data outside the U.S. While U.S. dollar strength has broad implications for earnings and markets, it also has a direct impact on the performance of international equity allocations for U.S. investors. Most international equity strategies are unhedged, which generally benefits U.S. investors in periods of dollar weakness but creates a headwind for returns when the dollar is strengthening.

So the dollar’s recent reversal raises an important question: Should investors start to incorporate currency hedging into their international equity allocations?

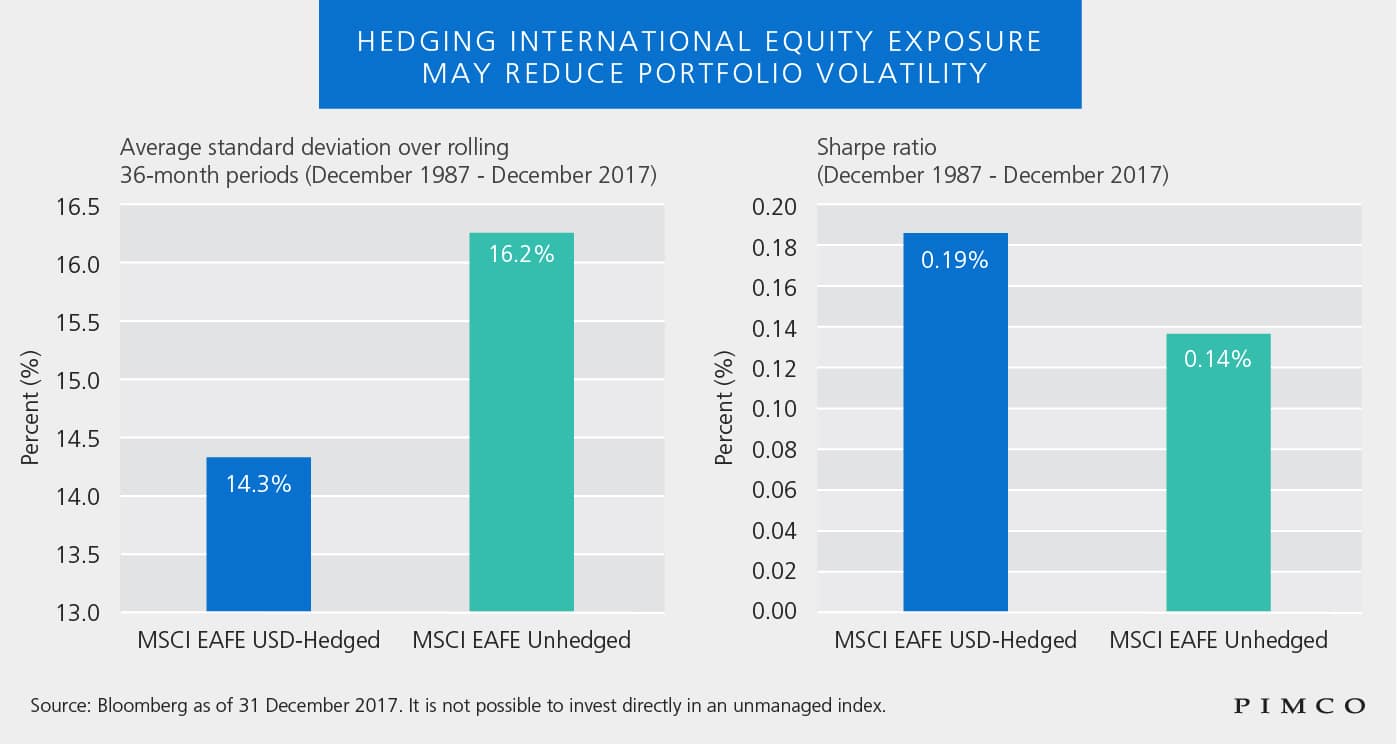

Unhedged versus hedged

Traditional active equity managers often say that their edge is not in forecasting currencies but in stock picking, and currency exposures are a fallout from the stock selection process. How then can investors in international equities incorporate currency hedging into their allocation?

International equities are a strategic investment for most, and attempting to tactically time exposure to the dollar seems inconsistent with a long-term horizon. Indeed, given transaction costs and the difficulty in forecasting currency movements, we would advise against such timing.

However, investors may want to consider a strategic allocation to a U.S. dollar-hedged international equity strategy. A hedged strategy can offer two important long-term benefits. First, when combined with an unhedged equity strategy, a hedged strategy can provide diversification: Hedged portfolios generally benefit from dollar strength and face a headwind in periods of dollar weakness. Second, hedged strategies have historically provided lower volatility and higher risk-adjusted returns, as represented by the index in the chart shown below.

The reason for the lower volatility in dollar-hedged strategies is straightforward: When equity markets decline significantly, investors often flee to high quality assets, and the dollar is one of these “safe havens.” In fact, since 1987 the MSCI EAFE USD-Hedged Index had a 77% downside capture ratio compared with the MSCI EAFE Unhedged Index.

Adding hedged equity exposure

After a very strong run in U.S. equity markets since the financial crisis, many investors are rebalancing into more attractively valued equities outside the U.S. We think the recent rally in the U.S. dollar serves as a useful reminder that currency movements affect the performance of international equity strategies. Allocating a portion of international equity investments to dollar-hedged strategies could provide both valuable diversification and the potential for downside protection.

Andrew Pyne is an equity strategist and a contributor to the PIMCO Blog.

DISCLOSURES

All investments contain risk and may lose value. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Investors should consult their investment professional prior to making an investment decision.

© PIMCO

© PIMCO

Read more commentaries by PIMCO