The Beginning of the End?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsRecessions are rare animals when financial conditions are favorable and private sector domestic imbalances are hard to find. The synchronized global expansion, which shifted into higher gear last year, will therefore almost certainly enter its 10th year this June and is unlikely to derail over our cyclical six- to 12-month horizon.

However, while continued solid growth in 2018 is a near certainty, the causes of the stronger expansion are more uncertain: Is this just a cyclical sugar rush fueled by easy financial conditions, fiscal expansion in the U.S. and a recovery in many emerging markets? Or are we witnessing the early stages of a supply-side productivity renaissance leading to higher trend growth and helped by lower marginal tax rates, deregulation and animal spirits? In other words, is this the beginning of the end of the global expansion … or of The New Neutral?

Needless to say, the two scenarios have very different implications for the durability of the global expansion beyond 2018 and for inflation and monetary policy, and thus for financial markets as well. While our base case hypothesis remains that solid current economic growth is more demand-led and cyclical than supply-driven, careful portfolio construction will have to acknowledge the considerable uncertainty around this key question.

Goldilocks extended, but seeing signs of peak growth

When PIMCO’s investment professionals from around the globe gathered for the quarterly Cyclical Forum earlier this month, we quickly coalesced around our macroeconomic team’s updated forecast of continued synchronized above-trend growth and moderately rising inflation over the cyclical horizon. While there are some early signs in business surveys that the global trade and manufacturing cycle may have peaked around the turn of the year, and despite a bout of volatility in asset prices in February, still-favorable financial conditions and fiscal support suggest that rumors of a sudden death of Goldilocks are exaggerated.

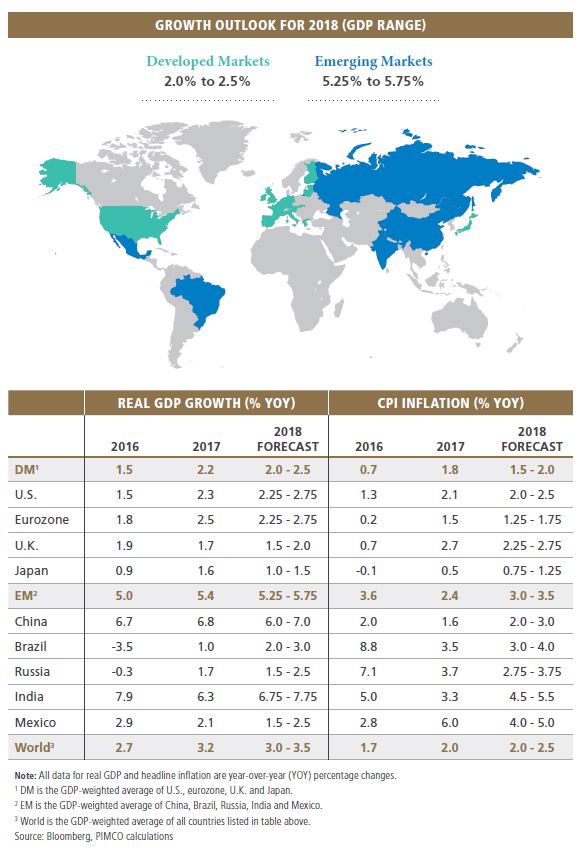

Compared with our December forecasts, we now foresee marginally higher 2018 GDP growth in the U.S., eurozone, U.K. and China, while we lowered our estimates for Mexico and India. On net, this should leave the world economy in the 3.0% to 3.5% growth channel for 2018 that we envisaged in December, compared with an outcome for 2017 in the middle of the same range.

Our inflation forecasts have been nudged slightly higher in response to a higher oil price trajectory, but we continue to expect both headline and core inflation to end the year below target in the U.S. (just), the eurozone and Japan.

It is important to note that both our benign growth and inflation forecasts are broadly in line with consensus (for more regional details, see the section on our regional forecasts) and appear to be baked into asset prices. This implies that there may be little room for error if economic growth would disappoint on the downside or inflation on the upside – another reason for relatively cautious portfolio positioning.

U.S. politics: Dr. Jekyll or Mr. Hyde?

Given that the cyclical outlook for growth and inflation was relatively uncontroversial at our forum, we quickly moved on to discussing the lower-probability but higher-impact right and left tail risks to markets and the economy emanating from the Trump administration’s current policy agenda. Libby Cantrill, PIMCO’s head of public policy, and our advisor Gene Sperling, former director of the National Economic Council (NEC) for Presidents Clinton and Obama, kicked off a broader debate by discussing the policy agenda post tax reform and budget deal, in particular infrastructure – the potential right tail – and trade policy – the potential left tail.

The administration’s infrastructure plan envisages $200 billion of federal spending aimed at sparking up $1.3 trillion of additional state, municipal and private infrastructure investment. It’s eye-catching, but we concluded that there is only a low probability that this would pass Congress over our cyclical horizon. Moreover, our municipal bond team argued that, if the plan were to be enacted, the take-up from the states, who do the bulk of infrastructure spending in the U.S., would likely be significantly smaller than the blueprint anticipates given a lack of fiscal space in many state coffers.

As regards trade policy, we expect the impact of the broad tariffs on steel and aluminum that the president announced earlier this month will be watered down further: Important trading partners such as Canada and Mexico have already been exempted, and we expect a few others to be exempted, too, in return for concessions in other areas. Moreover, potential tariff retaliation by Europe and others is likely to be proportional within the WTO guidelines and, like the steel and aluminum tariffs, would thus affect only a small part of overall trade.

A bigger concern would be broader protectionist action aimed at China in the area of intellectual property rights under Section 301, which is in the making. However, our China analysts believe that China would not respond aggressively, thus sparking a trade war, but rather aim at de-escalation and negotiations.

Overall, we concluded that both right and left tail risks from U.S. politics bear watching but are unlikely to cause major near-term positive or negative surprises that would significantly alter our cyclical baseline.

Emerging markets: how much room to run?

Another key topic for investors is the further path of emerging markets (EM), now that the recovery from a major slowdown or, in the cases of Brazil and Russia, a deep recession is firmly established. Pramol Dhawan and Lupin Rahman from our Emerging Markets Portfolio Committee, along with our distinguished advisor Nobel laureate Michael Spence, helped us think through and debate both the optimists’ and the pessimists’ cases for EM economies and asset markets.

The case for further EM outperformance rests on an expected further widening of the EM versus DM (developed market) growth differential, the emergence of new drivers of growth – in particular consumption – to replace the commodity supercycle, the more structural elements of the inflation decline, and much lower external imbalances than in the past.

Against this, we note the EM cyclical recovery may be more advanced than the consensus believes: Potential growth is slowing due to deteriorating demographics, the policy space for further stimulus is now more limited, political risks abound as major EM economies such as Mexico and Brazil will have elections with populist candidates polling strongly, and external conditions may turn less favorable with DM monetary policy heading toward the exit and protectionist sentiment on the rise.

On balance, our macro baseline for EM remains cautiously optimistic, but we are mindful of the risks and the fact that valuations have become less compelling.

Testing our New Neutral thesis

In the broad general discussion that followed our working sessions on these specific hotspots, we quickly zoomed in on the question whether our long-standing New Neutral thesis of low equilibrium interest rates (r*) caused by the confluence of low productivity growth, lower than historical credit growth, a continued imbalance between saving and investment (due to demographics, rising inequality and new capital-saving technologies) and elevated debt levels should still be the guiding paradigm for our investment stance. To be sure, this is a secular theme that we will revisit in more detail at our upcoming Secular Forum in May. However, with markets and, potentially, central bankers romancing a higher r* in the face of the step-up in the pace of global growth and a shift toward fiscal expansion, the relevance of this secular, longer-term question even for the cyclical outlook is obvious.

While overall we remain confident that expectations for low policy rates – compared with the pre-2008 old normal – will continue, we acknowledged both a more uncertain cyclical outlook and the secular question of whether post-crisis healing and the possibility of rising productivity growth could mean a sustained rise in r*. That said, a decade after the onset of the global financial crisis, the stock of public and private sector debt outstanding in the global economy remains at a record high level. Also, we continue to think that, in spite of the post-crisis recovery, economies will need lower rates than in the pre-crisis period in order to maintain growth. Finally, the demographic factors depressing the neutral rate have not changed and, on balance, we do not see the temporary effects of the U.S. tax cuts as having a sustained impact on the economy.

Therefore, while the uncertainty in the outlook has increased and we must continue to test and re-test our priors, we continue to see The New Neutral – that is, the expectation of a real neutral policy rate in the U.S. in the range of 0% to 1% – as an appropriate framework and an anchor for fixed income valuations. In this context we think the recent rise in yields has largely priced in the late stage fiscal expansion and the associated U.S. Treasury supply shock. While there remains some upside risk to global yields, and we expect to maintain duration underweight positions, we do not think that we are at the start of a secular bear market for bonds. In a poll of forum participants, all but a few expected the 10-year Treasury yield to remain in a broad range of 2.5%–3.5% this year, consistent with the New Neutral framework.

The neutral policy rate is of course an anchor and not a floor or a ceiling. In that regard, U.S. fiscal expansion at such a late stage in the economic cycle has significantly increased the uncertainty in the outlook and the difficulty of the task facing the new Federal Reserve Chairman Jerome Powell. The tax cuts and hurricane-related spending have increased the chances of the U.S. economy overheating at a time when unemployment is already at a very low level. The Fed may have to react – pushing the policy rate above neutral to outright restrictive – and the market may certainly factor in those expectations. While we forecast U.S. inflation getting to close to 2% on the Fed’s preferred PCE (personal consumption expenditures) measure, the upside risks have been increased by the late cycle fiscal boost. But again, we see the potential for a near-term cyclical overshoot rather than a major secular shift at this stage.

This is reinforced by our expectation that a U.S. recession is likely at some stage over our secular three- to five-year horizon – and indeed may be more likely if the fiscal expansion prompts the Fed to tighten policy more aggressively than expected. The neutral rate and the terminal rate are not the same thing. That said, it is probable that the U.S. will enter the next recession with fairly limited capacity for conventional monetary policy, compared with historical experience, as well as a large fiscal deficit.

Investment implications

We continue to emphasize caution, preferring to grind out alpha with bottom-up positions rather than big top-down macro risk positions, and maintaining flexibility to deploy the risk budget when opportunities present themselves. We continue to think that central bank tightening will lead to higher levels of volatility more sustained and widely felt than the February equity volatility spike.

In an environment of increasing volatility and tight valuations we want to be cautious in our overall portfolio positioning, looking to generate carry from a broad range of sources, without direct reliance on corporate credit risk. We seek to be prepared and flexible.

Duration

We expect to maintain modest duration underweights. We believe the rise in real rates in the U.S. has largely priced in the big increase in U.S. Treasury supply, but – as discussed above – the increased uncertainty in the outlook and the risk that markets will romance higher inflation, even if that is not our forecast, mean that it makes sense to maintain the duration underweights and a modest curve steepening bias at current valuations, with an underweight to the long end of the curve.

We expect to maintain a modest overweight in Treasury Inflation-Protected Securities (TIPS), reflecting reasonable valuations and the useful hedge in the event of upside U.S. inflation surprises.

We continue to see an underweight to Japan duration as an asymmetric opportunity, given the likelihood of a shift in the yield curve control regime over time and the inherent hedge against an unexpected significant rise in global yields that would, with a lag, be reflected in Japan.

We do not expect to have large positions in European peripheral government debt at current prices, with the positive cyclical economic outlook balanced by valuation, Italian political risk and secular concerns over the sustainability of the eurozone in the next recession.

Credit

We tend to avoid generic investment grade and high yield corporate bonds, emphasizing instead a broad range of short-dated “bend-but-don’t-break” positions in corporate credit and structured products. In corporate credit, we expect to find attractive bottom-up opportunities and new issues based on the analysis of our global team of credit portfolio managers and research analysts.

We continue to see non-agency mortgages as a high conviction spread position based upon our positive view on the U.S. housing market, their defensive qualities and attractive risk premia for liquidity, complexity and uncertainty over the timing of cash flows. We also see agency mortgage-backed securities (MBS) as reasonably priced and a good source of carry away from credit. We will also look, very selectively, for opportunities in commercial mortgage-backed securities and in corporate-loan-backed CLOs (collateralized debt obligations).

Emerging markets

We expect to find good opportunities in emerging market local and external debt. However, outside of our dedicated EM portfolios, we continue to see a diversified basket of EM currencies as the best way to express a positive view on EM fundamentals and to generate income.

Equities

More broadly, on asset allocation, we have a neutral outlook on U.S. equities given that currently the market almost fully prices in the expected tax benefits – with earnings per share growth expected at around 18% and limited room for further upgrades. Japan stands out positively with prospects for 20%-plus earnings growth this year and relatively cheap valuations, in our view.

Commodities

We expect to be modestly overweight commodities in our asset allocation portfolios, due to both their stand-alone return prospects and their potential diversification benefits should the global economy accelerate, elevating realized inflation. We are most positive on energy and base metals, which should be supported by global growth momentum.

Regional economic forecasts

U.S.

We expect above-trend real GDP growth in a 2.25% to 2.75% range in 2018. Household and corporate tax cuts should boost growth by 0.3 percentage points in 2018, with another 0.3 percentage points coming from higher federal government spending resulting from the two-year budget deal.

With the unemployment rate likely to drop below 4%, we expect some upward pressure on wage growth and consumer price inflation, with core CPI inflation rising above 2% in the course of the year. Core PCE inflation, the Fed’s preferred measure, should rise as well, to 1.8% from 1.5% currently, making some limited progress toward the 2% objective.

Under new leadership, the Fed is likely to continue to push the fed funds rate gradually higher as slack in the economy erodes. We expect at least three rate hikes in 2018, with a fourth hike likely if economic and financial conditions remain favorable throughout the year.

Eurozone

With growth momentum strong and financial conditions favorable, we expect eurozone GDP growth of between 2.25%–2.75% this year, about the same pace as 2017. A key feature of the current expansion is that the recovery is now broad-based across the region, with much less dispersion in member states’ growth rates than in earlier years.

Another key feature of this expansion is that core inflation has been and is expected to remain very low, creeping only marginally above 1% in the course of this year. Remaining slack, past labor market reforms and persistent competitiveness gaps among member states are holding wage pressures down. Moreover, the appreciation of the euro over the past year will likely damp consumer price inflation during 2018.

European Central Bank policy remains on autopilot for now, with net asset purchases running at €30 billion per month until September. We expect the purchase program to end then or, after a short taper, by December, though maturing bonds will be reinvested for an extended period of time. We don’t expect the first rate increase until around mid-2019.

U.K.

Our above-consensus forecast of 1.5% to 2% real GDP growth this year is based on the expectation that a deal on a transitional arrangement to smooth the U.K. separation from the EU will be struck in the near future. If this happens, we expect growth to reaccelerate as confidence picks up and some pent-up business investment is approved. Also, following seven years of austerity, we see some scope for stronger government spending.

Inflation should fall back toward the 2% target by the end of 2018 as the import price effect from last year’s sterling depreciation fades and there are still no signs of second-round effects on consumer prices. We expect the Bank of England (BOE) to continue with a gradual path of interest rate rises, with our central expectation of two hikes over 2018. That is predicated on relatively smooth negotiations between the U.K. and EU over Brexit. While it’s not our expectation, if the talks do break down it is still possible that the BOE leaves rates unchanged.

Japan

Our base case scenario for Japan foresees a continuation of firm growth in a 1% to 1.5% channel in 2018. Fiscal policy remains supportive ahead of the planned value-added tax hike in late 2019. With the unemployment rate below 3% and growth of (better-paid) full-time jobs accelerating, wage growth should pick up further, which should help core inflation to rise in the course of the year to slightly below 1%.

With the yen climbing higher and providing disinflationary headwinds and the newly appointed deputy governors tilting the Bank of Japan leadership somewhat more dovish, the Bank of Japan may not start to tweak its yield curve control policy until 2019.

China

With much of the credit and infrastructure stimulus having peaked, we expect a controlled deceleration of China’s GDP growth toward the midpoint of our 6% to 7% range for 2018, from 6.8% last year. The authorities’ focus is likely to be on controlling financial excesses, particularly in the shadow banking system, and on some fiscal consolidation, chiefly by local governments.

We expect inflation to accelerate on stronger core inflation and higher oil prices. This should induce the People’s Bank of China to tighten policy by raising official interest rates, versus consensus expectations for no hikes. We are broadly neutral on the currency and expect the authorities to continue to control capital flows tightly in order to keep exchange rate volatility low.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Collateralized Loan Obligations (CLOs) may involve a high degree of risk and are intended for sale to qualified investors only. Investors may lose some or all of the investment and there may be periods where no cash flow distributions are received. CLOs are exposed to risks such as credit, default, liquidity, management, volatility, interest rate and credit risk. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Diversification does not ensure against loss.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

The terms “cheap” and “rich” as used herein generally refer to a security or asset class that is deemed to be substantially under- or overpriced compared to both its historical average as well as to the investment manager’s future expectations. There is no guarantee of future results or that a security’s valuation will ensure a profit or protect against a loss.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes. Forecasts, estimates and certain information contained herein are based upon proprietary research only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL is a trademark of Pacific Investment Management Company LLC in the United States and throughout the world.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All