The Municipal Securities Rulemaking Board (MSRB)’s new “markup disclosure rule” is on track to go into effect in the U.S. in May 2018, as part of a broader move toward greater transparency in the municipal bond market. Approved by the Securities and Exchange Commission (SEC) last year, the MSRB rule will require municipal bond brokers to provide retail customers with a clear breakdown of the fees charged for most trades – a significant change that is likely to spur greater dialogue around the costs associated with retail municipal bond transactions.

Before and after the MSRB rule

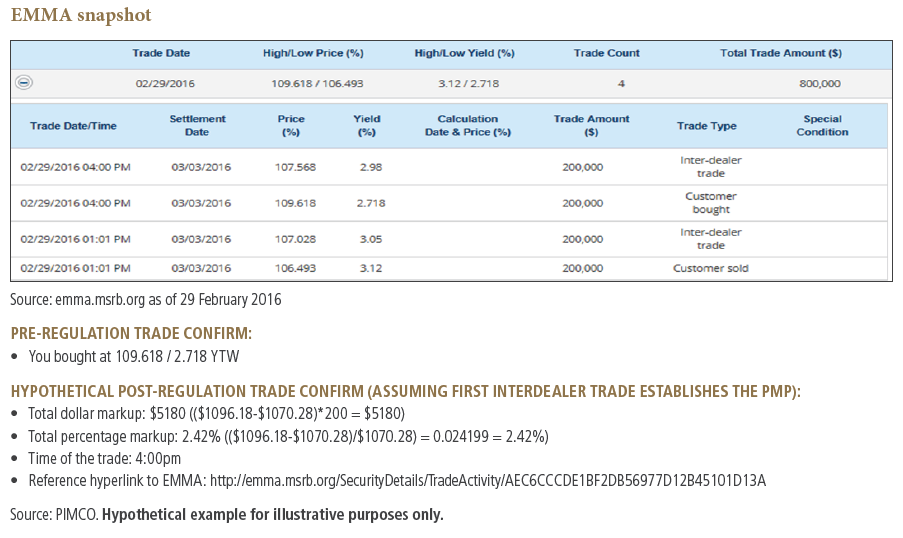

In the past, investor trade confirmations for municipal bond transactions have shown only the total price paid, with any markup already included in the price and not explicitly defined. After the new rule goes into effect, retail investors will see an explicit outline of the markup (or markdown) they paid, including the following required information:

- The total dollar amount of the markup/markdown (i.e., the dollar difference between the customer’s price and the security’s prevailing market price, or PMP)

- The total percentage amount of the markup/markdown (as a percent of the security’s PMP)

- The time of the trade

- A reference or hyperlink to Electronic Municipal Market Access (EMMA), the MSRB’s official repository for information, which includes historical trade price data (see snapshot below)

Trade confirmation before and after the markup disclosure rule

This insight into broker-dealer markups and how investment professionals are paid may generate mixed reactions from clients and could come as a surprise for some. Consider the example above: The markup on a $200,000 trade was over $5,000, which would likely stand in stark contrast to the commissions an investor is used to seeing in other markets, such as equities, where transaction costs are typically just cents per share or a flat (generally low) dollar amount per trade regardless of size

Challenges for broker-dealers

We think this could put further pressure on profitability in the transactional bond business, coming on the heels of other changes in the muni market that have made buying and selling individual bonds increasingly difficult and time-consuming for financial advisors. These include the decline in bond insurance and resulting need for enhanced credit due diligence, decreasing inventory levels, and difficulty getting low-cost, fairly priced execution on retail-sized trades.

Given these realities, some brokers may consider transitioning some or all of their municipal assets to outside managers who have the resources to overcome challenges in the space. This shift offers investors the potential benefits of outsourcing the ongoing credit surveillance, strengthening client relationships (by putting advisors on “the same side of the table” as their clients during portfolio reviews) and – perhaps most importantly – potentially reducing transaction costs for clients, given benefits of scale. Indeed, a 2013 study from the Securities Litigation & Consulting Group1 showed that median markups declined approximately 90% as trade sizes increased from $25,000 to $1 million and fell another 80% as trade sizes increased from $1 million to $5 million.

Knowledge is critical

We believe a thorough understanding of the markup disclosure rule and its implications is critical for all participants in the municipal bond markets. The MSRB’s EMMA site (emma.msrb.org) is a great resource for trade history, both for an advisor’s or individual investor’s own trades and for other trades in the same security. This transparency may provide a point of leverage that could bring transaction costs down in the future.

U.S. readers can visit our Muni Ladder Resource Center for Financial Advisors to learn more about how to communicate with, educate and engage with investors on these issues.

Julie Callahan and Alex Petrone are municipal bond portfolio managers and contributors to the PIMCO Blog.

© PIMCO

1 Geng Deng and Craig McCann, “Using EMMA to Assess Municipal Bond Markups,” Securities Litigation & Consulting Group, 11 June 2013.

© PIMCO

Read more commentaries by PIMCO