SUMMARY

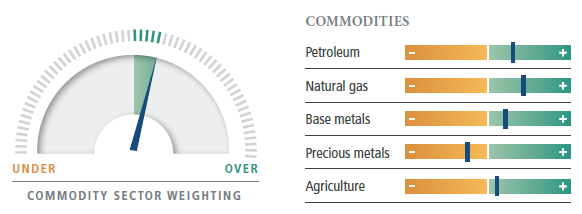

- Our overall positive outlook on commodities reflects our sector-specific views, which range from an underweight for precious metals to a modestly positive view on oil and a more sanguine outlook for natural gas.

- Although we expect prices for oil to remain range-bound, we believe positive returns from oil are still likely given investors’ ability to roll higher-priced short-term contracts into lower-priced longer-term contracts (generating “roll yield”).

- We see the greatest potential for price gains in natural gas, given low inventories and the need for strong production growth to provide adequate supplies for next winter.

Everyone seems to be a commodities bull lately. PIMCO is no exception: Our latest Asset Allocation Outlook suggests an overweight to real assets, including commodities.

Yet despite our positive view, we think those who expect commodities prices to keep rising may be disappointed. The secular themes of innovation and fading resource constraints are still intact, as best exemplified by the growth in shale production that sparked a bear market in natural gas seven years ago, ultimately spreading to oil. While we see potential for higher prices for most commodities, we believe oil, the largest component in nearly every commodity index, will remain range-bound. We think positive returns from oil are still likely, however, given investors’ ability to roll higher-priced short-term contracts into lower-priced longer-term contracts. Such “roll yield” opportunities will likely be an important contributor to oil returns.

On net, we favor a modest overweight to commodities.

Sector snapshots

Our overall positive outlook reflects our sector-specific views, which vary from an underweight for precious metals to our constructive view on natural gas.

Oil

Oil prices have recovered strongly over the past 12 months, briefly touching $70 per barrel (bbl) in early 2018. The idea that oil could trade so high seemed unlikely even several months ago, before a combination of production outages, strong, synchronized global growth and continued OPEC discipline fueled the rally. Now that we are here, there is much talk about why $80 is the next stop for oil. For our part, while we expect oil inventory draws in the second half to support prices after a period of seasonal builds, we believe several factors will keep the back end of the oil price curve anchored, limiting upside.

The biggest (but not the sole) driver of this anchor is U.S. shale production growth. This year, we expect shale oil in the U.S. to grow by 1.25 million barrels per day (b/d) for crude and by 1.5 million b/d including natural gas liquids – nearly meeting, on its own, the 1.6 million b/d of projected growth in global demand. We are also seeing incremental investments in some non-shale conventional resources, such as offshore, as efforts to drive down costs have made these supplies economical. Lastly, when oil prices move higher, alternative energy sources become even more viable, denting demand. Given this confluence of factors, we expect the back end of the Brent oil curve (defined as the five-year forward price) to be anchored in the $55–$60 range, where it has effectively remained for the past few years.

Our cautious price outlook does not mean oil is unattractive for investors, given the downward slope of the forward curve. The market is currently pricing one-year oil futures at a 6% discount to spot, indicating a potential gain of 6% from being long oil even if oil prices remain unchanged. Said another way, we are positive on oil prices relative to the one-year forward price.

Without delving too deeply into all the potential outcomes, we think it is worth highlighting a few risks to our outlook, which skew modestly to the upside overall. On the bullish side, synchronized global demand growth could simply exceed our forecast, allowing for a more rapid drawdown of inventories and supporting price appreciation to the low-to-mid $70s, above our base case. In addition, come May, the White House will have to decide yet again whether to extend the waiver on U.S. sanctions on Iran. Should sanctions be restored, the ultimate impact on output volumes would likely be far less significant than in previous periods, given their unilateral nature; however, any loss of output would incrementally reduce global inventories without offsetting OPEC output increases. Meanwhile, instability in several key producers, such as Venezuela and Libya, could also provide a boost to prices.

Turning to the downside risks, one cannot help but think back to 2014, when U.S. production accelerated above expectations and tilted global balances into a material surplus. Upward revisions by several data aggregation and forecasting agencies reflect rather impressive, higher-than-expected production already. Given that public companies have been highlighting their capital discipline and balance sheet focus, we believe nonpublic enterprises would be the most likely contributors to a production overshoot in the U.S.

Natural gas

The natural gas market is the area of the commodity complex with the greatest potential price gains, in our view. Notwithstanding a few historically cold weeks, weather has been relatively normal in the U.S. this winter. Nonetheless, inventories will likely end the season at the second-lowest level of the past 10 years, owing to strong underlying demand and export growth (which have contributed to tighter-than-normal balances on a weather-adjusted basis). Strong production growth will be required to rebuild inventories to normal levels and provide adequate supplies for next winter. We are skeptical that this growth can happen at current prices, particularly given that several of the largest gas-focused exploration and production (E&P) companies are guiding to lower capital expenditures and slower investment growth.

Agriculture

Grain prices are near 10-year lows, weighed down by abundant inventories of corn, soybeans and wheat. However, global inventories can change quickly in agriculture: One bad crop from a major global producer of corn or beans can send the market from well-above-average stocks to critical lows, making price action necessary to ration demand. Given the highly weather-dependent annual resupply cycles in these markets, the outlook for agricultural prices essentially boils down to the weather. The most likely outcome is a relatively normal year with trend-line yields and prices hovering around current levels. In this scenario, returns for grains would be negative, as forward curves are upward-sloping. However, if drought hits the U.S. this summer or South American crops disappoint, prices could move up sharply. These disparate potentialities net out to our flat to mildly positive outlook for forward-looking returns in agriculture.

Precious metals

We have written before about the link, both theoretical and practical, between gold and real yields: Gold prices have tended to rise as real yields fall, and vice versa. Yet recently, gold prices have moved higher even as yields in the U.S. have risen, perhaps because the market is focusing less on gold’s real duration and more on the reflationary theme that has bid up commodities generally. In other words, investors are currently demanding more gold at a given level of real yields than in the past. As in the case of oil – where we think extrapolating too much from recent strength is not wise, and that back-end prices remain anchored – we believe gold’s ability to decouple from the level of yields is ultimately limited. Certain factors, such as emerging market (EM) central banks increasing their gold holdings, could be a continued force behind a sustained repricing; however, it is also possible that demand from exchange-traded fund (ETF) investors will wane, and we will see liquidations from retail investors. Assuming the relationship between supply-demand for gold and real yields observed in recent years largely holds, we view gold as rich relative to real yields.

Base metals

The base metals sector is influenced more by the global growth outlook than any other commodity grouping, given that its supply-side response does not reset annually (as with agriculture) or have a short-cycle investment response (like energy). While metals broadly have tended to be tied to China’s economy in particular, we think a modest deceleration in China would be unlikely to derail the supportive metals outlook, given expectations for strong, synchronous global growth. In addition, years of underinvestment will limit supply growth in the next few years, outside of some brownfield expansions. In our view, the primary downside risk for base metals is a surprise downgrade in the global economic outlook, given the strong consensus that has developed.

Key takeaways

All told, we see generally a positive picture for the commodity complex this year, outside of gold. In the case of oil, our modestly positive view is driven primarily by the shape of the oil price curve – which is currently in backwardation – and the ability for forward prices to move up toward current spot prices. We are quite sanguine on natural gas and mildly positive on agriculture, though for the latter, we believe some deviation away from normal weather will be necessary to realize potential gains. Lastly, while we think gold is currently rich, we are cautiously positive on base metals given the solid global growth outlook.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Derivatives and commodity-linked derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Commodity-linked derivative instruments may involve additional costs and risks such as changes in commodity index volatility or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Investing in derivatives could lose more than the amount invested.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2018, PIMCO.

© PIMCO

Read more commentaries by PIMCO