So most know we took one of our South Florida speaking tours last week. Such tours consist of meeting with portfolio managers, presentations to clients of Raymond James, branch visits with our financial advisors, doing the media thing, well you get the idea. To all of those emailers/callers we were unable to respond to – apologies – but, the fact of the matter is we were doing five or six events a day, interspersed with a massive amount of phone calls, and then drive to the next event. While there were many questions about the bond/stock/commodity markets, the economy, earnings, etc., by far the most questions were about the December Low Indicator, because we broke below the December low last week. Recall, we brought this indicator to the attention of Jeff and Yale Hirsch decades ago and they have published it in The Stock Trader’s Almanac ever since. Since then it has been quoted by many Wall Street pundits, yet Lucien Hooper’s December Low Indicator would likely have been lost if not scribed by us a long, long time ago. We like this story:

It was back in the early 1970s, when I was working on Wall Street that I encountered Lucien. At that time Lucien, then in his 70s, was considered one of the savviest “players” in this business. While known for many market axioms and insights, the one that stuck with me was Lucien’s “December Low Indicator.” It seems like only yesterday we were sitting at Harry’s at the Amex Bar & Grill having lunch when he explained it. “Jeff,” he began, “Forget all the noise you hear about the January barometer; pay much more attention to the December low. That would be the lowest closing price for the Dow Jones during the month of December. If that low is violated during the first quarter of the New Year, watch out!”

Now the track record of Lucien’s indicator over the past 50 years is pretty good, especially when taken in concert with the January Barometer (“So goes the month of January so goes the year”). In the more recent history, however, Andrew Adam’s comments of last Friday are worth repeating. To wit:

One potential red flag, however, is that that the Dow Jones Industrial Average did close below its December closing low of 24410 to give us violation of the "December Low Indicator" we referenced last month. . . . The last time it happened was only two years ago back in 2016, though the situation was very different considering January 2016 began almost right where the December 2015 low sat, and the Dow ended up closing beneath it on the third trading day of the year. That, of course, culminated in the January/February correction that ended on February 11 and saw the Dow ultimately fall about 14% from its previous trading high of early November 2015. After that, though, the market went almost straight up to finish the year comfortably higher. Overall, the December Low Indicator has a rather mixed history going back to 2000. It is actually not uncommon at all to get a violation, with 12 occurrences since 2000, and the forward returns have been surprisingly encouraging. From the point of the December low being broken, the Dow was up after three months 8 out of 12 times, up after six months 7 out of 12 times, and up after 12 months 9 out of 12 times. So, while it does bear watching, we don't think the indicator, by itself, is enough to be overly concerned about, especially with stocks already near downside extremes.

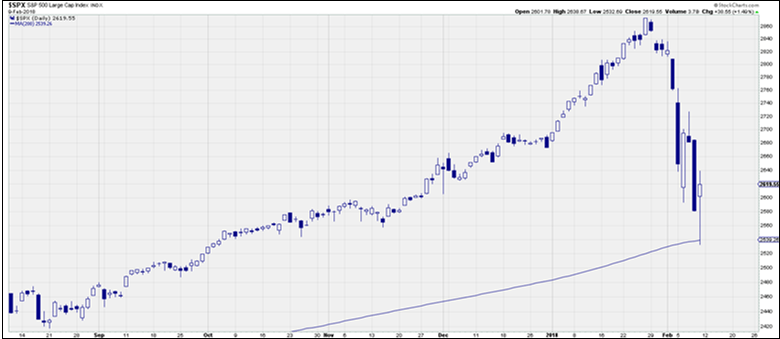

Speaking to “downside extremes,” the envisioned February Flop came three sessions before our February 1 target, but it was within the +/- three-session window our models allow. Subsequently, we got the anticipated selling climax last Tuesday, as related on CNBC that day. Then, as is the typical pattern, the indices experienced a sharp throwback rally that we chatted about on that same CNBC appearance and said that it should fail, with the indices sliding to lower lows. “The textbook chart pattern,” we said, “would be for an undercut low of Tuesday’s selling climax low.” Well, that’s pretty much what has happened. What we find interesting is that pundits that NEVER saw this decline coming have been rushing out over the past few weeks touting various support levels; you pick the index, as well as their various stock buy ideas, all of which are pretty worthless until the equity markets exhaust themselves on the downside. Ladies and gentlemen, when the stock market gets into one of the selling stampedes, all such comments are pretty useless! So what now?

Well, while normally our mantra of “never on a Friday” should have applied to last Friday’s Flop, meaning stocks in a selling skein rarely bottom on a Friday, that mantra probably doesn’t play this time. Indeed, the bottoming process we laid out weeks ago was almost textbook, punctuated by last Friday’s undercut low. As written:

What should happen here is a selling climax low today followed by a throwback rally that fails, leading to a retest of the recent intraday lows. The perfect chart pattern would be for a marginal undercut low downside test of this early week's trading lows, which would turn EVERYBODY bearish looking for another huge leg to the downside, yet we would BUY it, believing the worst has been seen in a continuing secular bull market.

And then there was this over the weekend from Canada’s savviest oracle ever, our pal Leon Tuey:

What a tumultuous week! Don’t sweat and be happy as the correction is over and the great bull market has resumed. On Tuesday, what investors saw was a classic selling climax, which comes at the end of a selling squall. A selling climax is an emotional catharsis when investors “throw the baby out with the bathwater.” Besieged by fear, investors are willing to sell at any price. They fear that their holdings will go to zero. Consequently, stocks move from weak hands into strong hands. How fearful? On Monday, my phone rang off the hook and it didn’t stop ringing until 9:30 p.m. Most of the callers were practitioners in the business, retired or active, and they came from Europe, Asia, and local. That was the most phone calls that I’ve fielded in one day for more than 35 years! They were all very calm and collected. I am flattered that they called, but the calls were instructive. Globally, investors panicked, which is very bullish. Remember what Warren Buffett advised: “Be fearful when others are greedy and be greedy when others are fearful!”

The call for this week: Well, it’s Saturday and we are still on the road. Since we are writing this from Orlando, a fitting title for the last few weeks would be “Mr. Toad’s Wild Ride” (Toad); but we digress. Speaking to yet another ubiquitous question from last week was, “Did we get a Dow Theory sell signal?” The answer, at least by our interpretation of Dow Theory, is a resounding NO! So, as stated, the bottoming process was picture perfect. We called the downturn, last Tuesday’s selling climax, the subsequent failed throwback rally, and Friday’s undercut low (the print low below last Tuesday’s selling climax low). Indeed, “picture perfect!” Our energy models are calling for an upside energy whoosh this week, so we think the selling stampede is over!

Chart 1 – S&P 500

Click here to enlarge

Additional information is available on request. This document may not be reprinted without permission.

Raymond James & Associates may make a market in stocks mentioned in this report and may have managed/co-managed a public/follow-on offering of these shares or otherwise provided investment banking services to companies mentioned in this report in the past three years.

RJ&A or its officers, employees, or affiliates may 1) currently own shares, options, rights or warrants and/or 2) execute transactions in the securities mentioned in this report that may or may not be consistent with this report’s conclusions.

The opinions offered by Mr. Saut should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your Raymond James Financial Advisor.

All expressions of opinion reflect the judgment of the Equity Research Department of Raymond James & Associates at this time and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the material presented is accurate or that it provides a complete description of the securities, markets or developments mentioned. Other Raymond James departments may have information that is not available to the Equity Research Department about companies mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this presentation’s conclusions. We may perform investment banking or other services for, or solicit investment banking business from, any company mentioned. Investments mentioned are subject to availability and market conditions. All yields represent past performance and may not be indicative of future results. Raymond James & Associates, Raymond James Financial Services and Raymond James Ltd. are wholly-owned subsidiaries of Raymond James Financial.

International securities involve additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

Investors should consider the investment objectives, risks, and charges and expenses of mutual funds carefully before investing. The prospectus contains this and other information about mutual funds. The prospectus is available from your financial advisor and should be read carefully before investing.

© Raymond James

© Raymond James

Read more commentaries by Raymond James