2018 began with a bang as markets continued to set fresh records. In what some dubbed a “melt-up” ‒ the self-perpetuating rally that often precedes a sell-off ‒ the gains in equities were impressive: Global stocks rose 5.6%, the third best January since the inception of the MSCI AC World Index in 1987, and emerging market equities5 surged 8.3%. Even more notable, though, was the length of the broader rally: Both the S&P 500 and MSCI World Indexes entered their longest periods without a correction of more than 5%. The risk rally was not confined to the bottom of the corporate capital structure: High yield credit spreads11 tightened over 20 bps, Brent crude rose above $70 per barrel for the first time since December 2014, emerging market currencies soared against the U.S. dollar, and U.S. inflation expectations hit a multi-year high. Developed market currencies also rallied against the U.S. dollar, and yields rose across many developed economies, weighing on safe-haven assets. Positive economic data helped stoke the market exuberance, already invigorated by the prospects of stronger global growth and fiscal stimulus in the U.S.

A U.S. government shutdown and the potential for a trade war did little to curb the market rally. The U.S. government shut down for the first time since 2013 as battles over immigration blocked a funding bill. The standoff was short-lived though: Senate Majority Leader Mitch McConnell brokered a deal within three days to provide stopgap funding through 8 February with a promise to address protection for “dreamers” (undocumented immigrants brought to the U.S. as children). With the shutdown behind him, President Donald Trump attended the World Economic Forum in Davos, where Treasury Secretary Steven Mnuchin’s endorsement of a weaker dollar renewed concerns over protectionism. This came just days after the U.S. administration announced its first (largely symbolic) import tariffs ‒ on washing machines and solar panels ‒ and amid growing worries that the U.S. might withdraw from NAFTA as the sixth round of negotiations continued. In Iran, civil unrest escalated with ongoing anti-government protests, and the state of its nuclear deal remained tenuous as President Trump threatened to restore sanctions unless his European counterparts fixed concerns with the agreement. Meanwhile on the Korean peninsula, tensions appeared to thaw somewhat as North Korea agreed to participate at the Winter Olympics in PyeongChang in February.

Fundamentals continued to underpin the global growth narrative. In the U.S., generally positive growth coupled with steady inflation data appeared to keep the Federal Reserve on a path to another rate hike in March. Americans demonstrated an increased willingness to use their credit cards in recent months: Consumer credit surged above expectations to its highest level in 16 years. Business activity remained firmly in expansionary territory as the ISM manufacturing survey pointed to a sustained recovery in the factory sector, fueled by a boost in new order activity and higher prices paid for inputs. Initial jobless claims dipped to their lowest level in 45 years, despite a smaller-than-expected gain in new jobs, while the unemployment rate was unchanged. However, retail sales lagged after a strong report in December, and the initial reading of fourth-quarter GDP came in below expectations. Elsewhere, the rise in core inflation in Europe, while still below the European Central Bank’s (ECB) target, supported an optimistic near-term outlook for the European economy. Despite this backdrop, ECB President Mario Draghi pushed back against suggestions that the ECB could begin to raise rates this year.

In a league of its own While the S&P 500’s 22% rally in 2017 (and 16% annualized return over the past five years) is impressive, January’s single month return of nearly 6% was in a league of its own. Yet the U.S. was in good company: The MSCI World jumped 5% in January, and the MSCI EM Index soared over 8% – emerging markets’ best start to the year since 2012. What’s more, both the S&P 500 and MSCI World Indexes entered their longest period without a correction of more than 5% (foreshadowing for February?). As risk markets surged, bond prices fell and yields rose in response to fading central bank stimulus, prospects for higher inflation, and increased fiscal stimulus in the U.S. In contrast, the U.S. dollar fell sharply in January on a pickup in global growth expectations and after Treasury Secretary Steven Mnuchin endorsed a weaker dollar at the World Economic Forum in Davos.

Market snapshot

EQUITIES

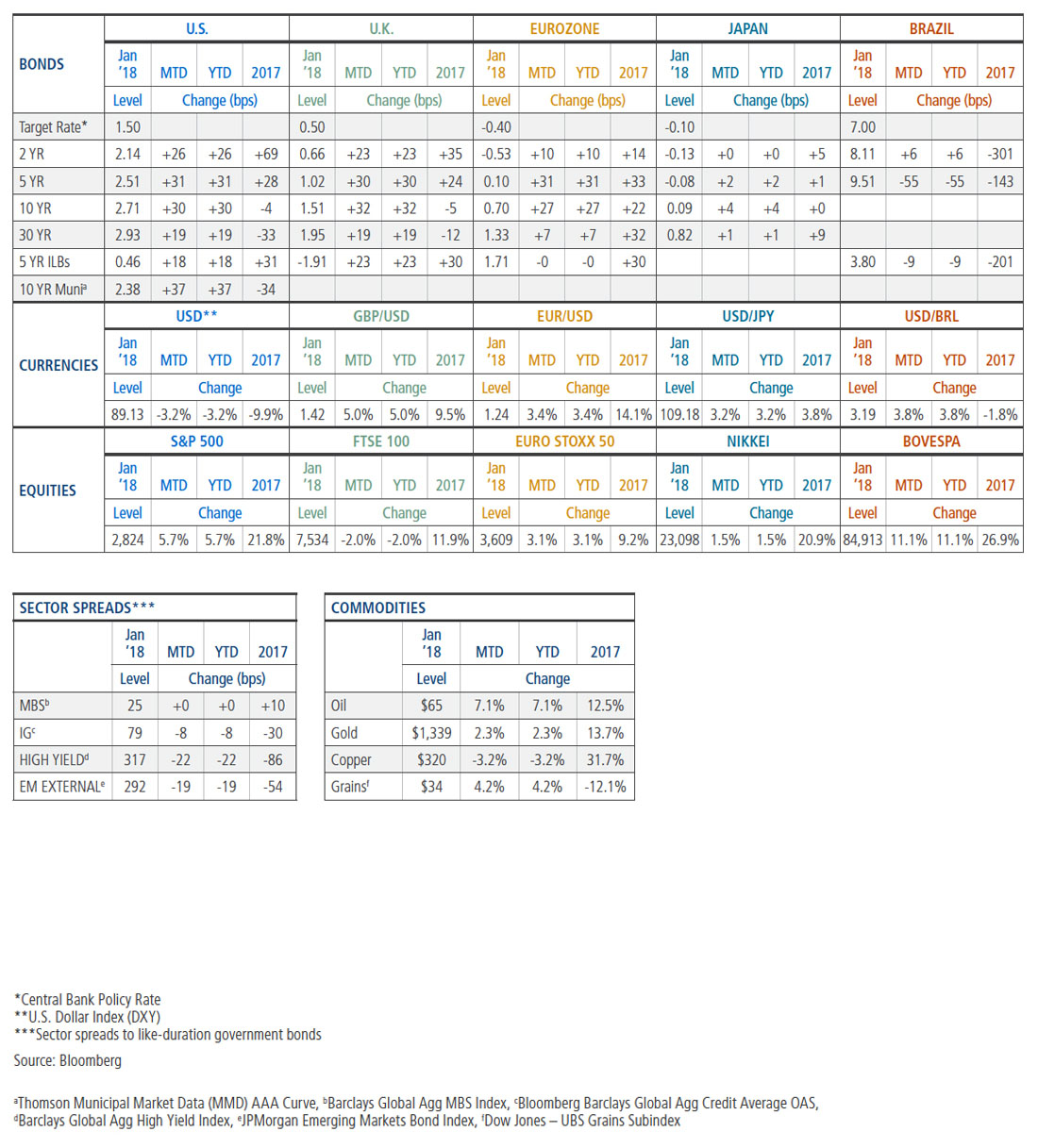

Strong fundamentals boosted investors’ appetite for risk, and developed market stocks1 returned 5.3% in January. Gripped by surging optimism that tax reform will lift corporate profits, stocks in the U.S.2 rose 5.7% and thus marked their longest run without a correction greater than 5%. European stocks3 returned 1.6% on the back of generally positive earnings despite a stronger euro. Japanese equities4 rose 1.5% to a 26-year high after the Nikkei 225 breached 24,000 for the first time since 1991.

In emerging markets,5 stocks returned a remarkable 8.3% for the month, benefitting from relatively stable global market conditions and a strong technical backdrop. In Brazil,6 stocks surged 11.1% after a Brazilian court dismissed an appeal by former President Luiz Inácio Lula da Silva against a corruption conviction. Buoyed by stronger-than-expected growth and renewed optimism over the economy, Chinese equities7rose 5.3%. Stocks in India8 rose 5.6%, as euphoric momentum continued to underpin strong investment flows. Russian equities9 gained 8.6% amid higher crude oil prices.

DEVELOPED MARKET DEBT

Broad-based growth, expectations for higher inflation, and greater supply put upward pressure on developed market bond yields throughout the month. In the U.S., rates moved higher as generally positive economic data pointed toward a rate hike in March. The U.S. 10-year Treasury yield ended the month at 2.71%, its highest level since April 2014. In the eurozone, German bonds experienced a similar sell-off: A rise in core inflation pushed the 10-year bund yield 27 basis points (bps) higher to 0.70%. In the UK, rates rose on the back of growing optimism around Brexit negotiations – the UK 10-year yield ended the month 32 bps higher at 1.51%.

INFLATION-LINKED DEBT

Global inflation-linked bonds (ILBs) posted negative returns but outperformed comparable nominal bonds across the major markets in January. Global real yields broadly rose after the Bank of Japan modestly trimmed its purchases of Japanese government bonds and the Bank of Canada raised interest rates, sparking speculation that global central banks are taking a synchronized approach toward tighter monetary policy. In the U.S., real yields followed global yields higher, and the yield curve steepened; but rising commodity prices and a strong-than-expected December inflation report supported another strong performance for breakeven inflation rates (BEI). In the UK, index-linked gilts posted negative returns: Expectations for a rate hike increased after a surprise pick-up in UK growth in the fourth quarter. UK breakeven inflation rates ended the month higher, despite the headwind of a strong British pound.

CREDIT

Global investment grade credit10 spreads tightened eight bps in January on improving confidence in corporate profits under the new U.S. tax law. The sector outperformed like-duration global government bonds by 0.62% during the month, as demand for high quality credit remained robust and Treasury yields rose.

Global high yield bonds11 performed well out of the gate, alongside the strong equity market and higher oil prices. But they softened in the second half of the month when higher Treasury yields weighed on investor sentiment and investment flows turned negative. Nevertheless, the asset class was up 0.6% for the month, as spreads compressed by over 25 bps and yields remained flat.

EMERGING MARKET DEBT

Emerging market (EM) debt performance diverged between external and local markets in January. Local debt performance was positive, driven both by a move lower in index yields and by the appreciation of EM currencies versus the U.S. dollar. External debt performance was mixed: External sovereign debt posted negative returns as a sharp move higher in U.S. Treasury yields more than offset spread tightening; lower-duration EM corporate bonds, however, posted modestly positive returns. Brazilian local debt was a notable outperformer after an appeals court unanimously upheld the conviction of former President Luiz Inácio Lula da Silva, diminishing his chance of running in the upcoming presidential elections. Argentina’s central bank cut interest rates despite persistently high inflation, causing both local and external asset performance to lag.

MORTGAGE-BACKED SECURITIES

Driven by higher rates, yield curve flattening and increasing volatility, agency MBS12 returned ‒1.17% and underperformed like-duration Treasuries by 15 bps. Lower coupon MBS outperformed as higher coupons extended, while Ginnie Mae MBS outperformed conventional MBS in response to the introduction of a bill in the Senate that aims to crack down on aggressive marketing of mortgage refinancing to veterans. Gross MBS issuance decreased 8% in January, prepayment speeds fell 4%, and the cap on the monthly runoff of MBS from the Federal Reserve’s balance sheet increased from $4 billion to $8 billion. Non-agency residential MBS outperformed like-duration Treasuries during the month and spreads tightened, while non-agency commercial MBS13 returned ‒0.86%, outperforming like-duration Treasuries by 60 bps.

MUNICIPAL BONDS

The Bloomberg Barclays Municipal Bond Index returned ‒1.18% in January, making it the worst start to the year since at least 1980, but even so, munis outperformed Treasuries. As AAA muni rates moved at least 35 bps higher over the month in most maturities (10-year Treasury rates moved 30 bps higher) duration was the largest contributor to market softness. Short maturities outperformed both intermediate and long maturities and the muni yield curve steepened. Despite two big uncertainties ‒ the path of interest rates and federal infrastructure plans ‒ municipal bond mutual fund demand was positive during the month. Total muni supply fell below the long-term average to $21 billion; this was not a surprise to investors because the surge in muni issuance in December leading up to tax reform had effectively “pulled forward” issuance from future years.

CURRENCIES

The U.S. dollar began the year weaker against a backdrop of trade tensions and a healthy appetite for risk assets. Comments from U.S. Treasury Secretary Steven Mnuchin ignited a debate around the administration’s dollar policy, and capital flows into non-U.S. developed and emerging market risk assets quickened. The strengthening European economy pushed the euro to three year highs, and European Central Bank President Mario Draghi chose not to forcefully push back against the euro’s strength in remarks to the media. The British pound rallied 5% thanks to greater optimism surrounding Brexit negotiations and stronger-than-expected GDP growth. Despite a widening trade surplus with the U.S., the Chinese yuan posted its best monthly gain in more than 10 years following a hawkish change to official foreign exchange policy.

COMMODITIES

Commodities started the year on a strong note. Crude oil continued its upward trek: It overcame a mid-month dip and climbed to a three-year high as the U.S. dollar weakened, U.S. inventories fell and compliance with OPEC’s output agreement remained high. Natural gas managed to stay in positive territory; prices were buoyed by inventory draws early in the month and strong demand during a bout of cold weather. The agriculture sector posted modest positive returns as gains in grains more than offset losses in other products. Leading the rally in grains, wheat recovered from a mid-month USDA report showing supplies had increased when concerns surfaced over winter crop quality during the drought. Sugar continued to lose ground as supply data began to reflect the favorable monsoon season in Asia. Dollar weakness following a three-day U.S. government shutdown supported metals prices, especially precious metals.

Outlook

PIMCO expects world GDP growth to remain above-trend at 3.0%‒3.5% in 2018, in a “Goldilocks” environment of synchronized global growth and low but gently rising inflation. Relatively easy financial conditions, reflecting buoyant risk assets and low interest rates, and fiscal stimulus in several advanced economies imply near-term tailwinds. However, 2017-2018 could mark the peak for economic growth in this cycle, and with many markets already reflecting an optimistic outlook, we see risks ahead: U.S. fiscal stimulus late in the cycle leaves less room for stimulus in the next recession; inflation may well overshoot expectations in 2018 due to fiscal stimulus, rises in commodity prices and easy financial conditions; and the reduction of accommodative monetary policy by global central banks could pressure economies and asset markets, which have become accustomed to low interest rates, possibly leading to bouts of market volatility.

In the U.S., we look for above-consensus growth of 2.25%–2.75% in 2018. Tax cuts and higher federal spending ‒ due to hurricane-related disaster relief and a likely rise in discretionary spending limits under an expected government funding compromise – should boost growth. With unemployment likely to drop below 4%, we expect some upward pressure on wages and consumer prices, and core inflation to rise above 2% over the course of 2018. Under new leadership, the Federal Reserve is expected to continue tightening gradually; our baseline forecast calls for three rate hikes this year.

For the eurozone, we expect growth will be in a range of 2.0%‒2.5% this year, significantly above trend. The expansion is now broad-based across the region, with growth momentum strong and financial conditions favorable. Core inflation, though, is expected to remain very low, creeping only marginally above 1% this year due to low wage pressures and the appreciation of the euro in 2017. We expect the European Central Bank to end its bond purchases in September, but we do not foresee a rate increase until mid-2019.

In the UK, we expect above-consensus growth in the range of 1.25%–1.75% in 2018. Our base case is that a deal for a transitional arrangement will be struck in the first half of this year, smoothing the UK’s separation from the European Union, and that growth will reaccelerate in the second half as business confidence and investment pick up. Inflation should fall back to the 2% target by year-end, with the effect of sterling’s depreciation in 2017 fading. The Bank of England will likely follow a very gradual path higher; we expect one to two hikes in 2018.

Japan’s GDP growth is expected to remain firm at 1.0%–1.5% in 2018, with risks tilted to the upside. Fiscal policy should remain supportive ahead of the planned value-added tax hike in 2019. With unemployment below 3% and job growth accelerating, we think inflation will move up gradually toward 1% over the year, but the 2% inflation target is likely to remain out of reach. We expect the Bank of Japan to aim to slow its balance sheet expansion and/or tweak its yield curve control policy so that the yield curve steepens this year.

In China, we expect a controlled deceleration in growth to 5.75%–6.75% this year. The authorities’ focus is likely to be on controlling financial excesses, particularly in the shadow banking system, and on some fiscal consolidation, chiefly by local governments. We expect inflation to accelerate to 2.5% on stronger core inflation and higher oil prices, inducing the People’s Bank of China to tighten policy by raising official interest rates, versus the consensus expectation of no hikes. We are broadly neutral on the yuan and expect exchange rate volatility to remain low.

In Brazil, Russia, India and Mexico, we expect growth to collectively rise to 4% in 2018, slightly above consensus, with modest upside risk from recoveries in Brazil and Russia. Emerging markets are catching up to the recovery in developed markets, with improving fundamentals and greater differentiation among countries. This recovery is likely to be shallower and slower than others, however; EM potential growth has fallen, and key political events are likely to keep investors cautious. We expect inflation to stabilize around 4.1%, also above consensus as most of the decline in EM inflation thus far appears cyclical rather than structural.

1MSCI World Index, 2S&P 500 Index, 3MSCI Europe Index (MSDEE15N INDEX), 4Nikkei 225 Index (NKY Index), 5MSCI Emerging Markets Index Daily Net TR, 6IBOVESPA Index (IBOV Index), 7Shanghai Composite Index (SHCOMP Index), 8S&P BSE SENSEX Index (SENSEX Index), 9MICEX Index (INDEXCF Index), 10Barclays Global Aggregate Credit USD Hedged Index, 11BofA Merrill Lynch Developed Markets High Yield Index, Constrained, 12Barclays Fixed Rate MBS Index (Total Return, Unhedged), 13Barclays Investment Grade Non-Agency MBS Index

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominatedand/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation- Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income. It is not possible to invest directly in an unmanaged index.

PIMCO does not provide legal or tax advice. Please consult your tax and/or legal counsel for specific tax or legal questions and concerns. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Any tax statements contained herein are not intended or written to be used, and cannot be relied upon or used for the purpose of avoiding penalties imposed by the Internal Revenue Service or state and local tax authorities. Individuals should consult their own legal and tax counsel as to matters discussed herein and before entering into any estate planning, trust, investment, retirement, or insurance arrangement.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.