SUMMARY

- We believe U.S. economic expansion and federal tax cuts will be generally supportive of municipal credit fundamentals in 2018.

- After a surge in muni issuance in December leading up to tax reform, we expect a decline in issuance this year, which we anticipate would provide a tailwind for valuations.

- Banks and insurance companies, paying less in federal taxes, will likely require higher relative yields and lower prices on tax-exempt municipals before becoming net buyers during outflow periods. And with the risks of a cyclical inflation overshoot rising, a pickup in interest rate market volatility could test this new muni liquidity paradigm.

- In our view, a modest duration underweight and an emphasis on portfolio liquidity will provide the ability to turn municipal valuation overshoots into opportunities.

We expect policy will continue to drive municipal bond markets in 2018, if more constructively than in 2017. Municipal investors may remember 2017 as the year of unrealized policy fear. While the threat of tax reform and its potential to reduce the value of the muni exemption for retail investors loomed large, ultimately it had little impact on individual municipal bonds.

For 2018 and beyond, more significant policy changes – including limitations on certain muni issues, curtailment of the state and local tax (SALT) deduction and the reduction in corporate tax rates – we anticipate will influence supply and demand and underscore the need for an active approach. In our Cyclical Outlook for the next six to 12 months, PIMCO’s top global macro and investment experts identified three areas of risk that we believe municipal investors should watch this year:

-

Late-cycle fiscal stimulus. We estimate that U.S. fiscal expansion will contribute close to 0.5% of GDP in 2018, with the economy already operating near full employment.

-

Rising risks of wage and/or price inflation. Global structural forces are still weighing on inflation, but cyclical pressures and the risks of an overshoot are rising.

-

Risk of monetary policy overkill. We expect the Federal Reserve to hike three times this year, the European Central Bank to begin signaling hikes in 2019 and the Bank of Japan to curb balance sheet expansion and/or tweak its yield curve control policy toward a steeper curve.

Against this backdrop of fiscal expansion and reduced monetary accommodation, PIMCO plans to position for pockets of interest rate and price volatility that may give rise to active opportunities in the muni market. We expect to be moderately underweight duration and will look to apply the best bottom-up ideas while maintaining the flexibility and liquidity to take advantage of opportunities presented in more difficult market conditions. At the start of 2018, credit spreads in lower-quality municipal assets look attractive versus other U.S. credit alternatives.

Issuance set to decline after December surge, creating a performance tailwind

December 2017 marked the single largest month of issuance in municipal market history, with $64 billion in supply, surpassing the period just before tax reform in 1986. With not-for-profit healthcare, higher education, private activity bonds and advanced refundings all on the chopping block in dueling House and Senate tax reform proposals, issuers rushed to market to beat the year-end deadline, effectively “pulling forward” issuance from future years.

When the dust settled, advanced refundings – which allow municipal issuers to refinance debt with call dates greater than 90 days – were the only form of issuance to get the ax in the Tax Cuts and Jobs Act. These issues represented 22% of primary supply in 2017, and while it’s hard to gauge exactly how much future healthcare, higher education and private activity bond issuance was pulled forward into 2017, we think a decline in total primary supply of 25% or more in 2018 seems probable. This could create a tailwind for municipal asset performance over the cyclical horizon.

We believe such declines in municipal issuance could firm into a lasting trend. A number of factors have constrained supply over the past decade, including the 2009–2010 federal Build America Bonds (BABs) program, which diverted callable federally tax-exempt income muni issuance into taxable noncallable bonds, along with a dip in issuance in 2011 amid global market volatility. All told, we expect there to be less callable tax-exempt debt eligible for refinancing into longer-duration primary supply over the next three to four years, which will support valuations on outstanding bonds.

In our view, only a large-scale national infrastructure program that taps the traditional tax-exempt municipal bond market to finance new assets or improve existing ones could significantly expand future supply. However, we think this may prove difficult in 2018 given the need for bipartisan support and an already crowded legislative agenda.

Tax reform likely to boost demand from individual investors, test corporate appetite

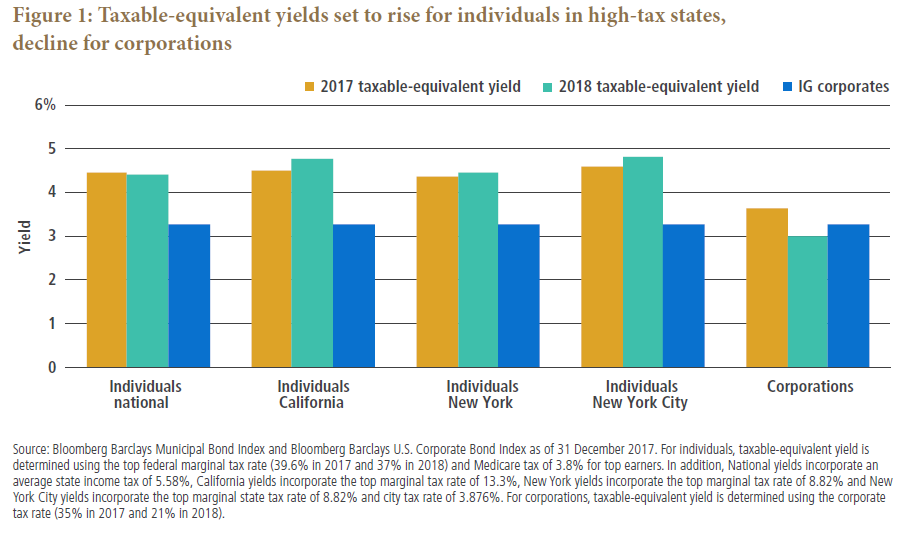

Federal tax reform will likely boost demand for tax-exempt municipals among individual investors, especially in high-tax states like California and New York, where the elimination of the SALT deduction will make the tax advantage more attractive on a relative basis (see Figure 1). Moreover, the aging of the U.S. population, a wave of retiring baby boomers and the corresponding need for high quality tax-efficient income will also support individual demand.

However, corporations – not individuals – will likely have the biggest impact on demand. Banks and insurance companies own more than $1 trillion in tax-exempt muni bonds, or roughly 30% of outstanding debt, up from approximately 20% in 2009 (according to Federal Reserve data). The reduction in corporate tax rates to 21% from 35% is quite meaningful for muni yields on a taxable-equivalent basis, as Figure 1 shows. Still, this doesn’t necessarily presage widespread selling. Banks and insurance companies have other compelling reasons to hold on to their muni investments, including low correlations with other assets, low default rates historically and built-up investment income through “book yield” portfolio management. However, they may be less likely to step in as buyers of tax-exempt bonds during periods of market stress, as they’ve tended to do over the past decade (making these companies the marginal price-setters for muni bonds during periods of retail-focused outflows). Lower corporate tax rates will make munis less attractive to these investors on a relative basis, meaning prices will have to fall further to attract new capital during outflow cycles.

Volatility may give rise to active opportunities

PIMCO’s baseline U.S. forecast for 2018 calls for 2.25%–2.75% real GDP growth, gently rising inflation and three Fed rate hikes – an environment likely favorable to tax-exempt munis, which have outperformed during previous Fed hiking cycles (see Figure 2). The value of the muni tax exemption increases at higher absolute yields. For example, a corporate bond would require an 84 basis point (bp) increase in taxable yields (to 5.91% from 5.07%) to achieve the same after-tax yield as a 50 basis point (bp) increase in tax-free muni yields (to 3.5% from 3.0%). (Taxable-equivalent yield is determined using the top federal marginal tax rate of 37% and Medicare tax of 3.8% for top earners. Together, these top tax rates accumulate to 40.8%.)

What often matters most for muni investors, however, is not the destination of higher rates but the speed of the journey. Interest rate volatility combined with higher yield targets for banks and insurance companies could lead to a short-term overshoot of tax-exempt yields relative to fundamentals, creating opportunities for active managers.

Muni credit conditions remain solid

The combination of economic growth and federal tax cuts should support U.S. municipal credit conditions over the next year. U.S. taxpayers as a group will see an increase in disposable real income, buoying consumer spending (which contributes 70% to the U.S. economy). Sales tax collections will likely increase in kind, benefiting the general funds of most states and many local governments. Corporations may transfer savings from tax reform to the real economy through higher wages and accelerated capital investing.

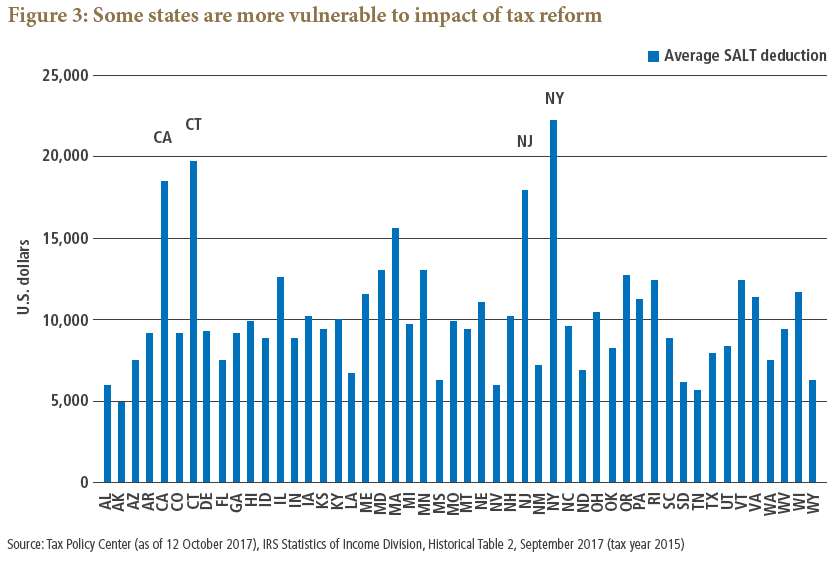

The curtailments of the SALT deduction and the mortgage interest deduction (MID) for new loans have generated political anxiety in high-tax states. Under federal tax reform, individual taxpayers may only deduct $10,000 in aggregate for property, income and sales taxes paid locally. Officials fear higher effective tax rates on wealthier residents may challenge the ability to balance state budgets, maintain spending priorities and cover the rising cost of nondiscretionary items (such as pension costs) while encouraging migration of residents to lower-tax states. California, Connecticut, New York and New Jersey appear most susceptible, with average SALT deductions ranging from approximately $18,000 to $22,000 versus a national median of roughly $9,000 (see Figure 3).

We think concerns about accelerated outmigration in these states are overblown, but higher effective tax burdens may contribute to greater budget volatility if even a small number of taxpayers depart. In addition, local municipalities in these high-tax states may see a reduction of state funding while simultaneously facing pressure to lower taxes. Moreover, political discord could even flare during state budget talks as legislators struggle to adjust their priorities to federal tax reform. Despite these risks, we believe state and local governments have the financial capacity to adjust to any negative fiscal shocks over multiple years and budget cycles.

California and New York have already challenged aspects of federal tax reform, proposing various workarounds to replace the SALT deduction with a payroll tax or allow taxpayers to make charitable deductions directly to the state. New York Governor Andrew Cuomo has even suggested that the federal tax reform may be unconstitutional. We believe the federal government will contest these proposals and that the workarounds will probably fail to achieve their desired objectives.

Muni sector outlooks for 2018

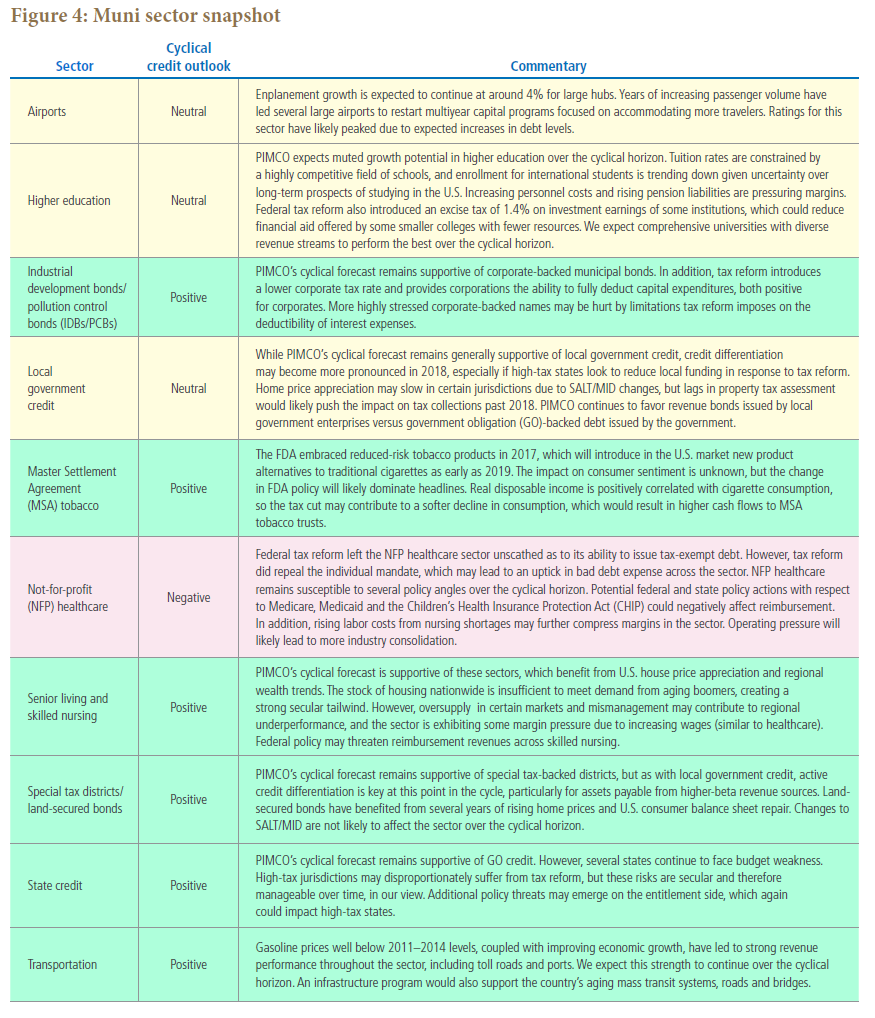

Despite our constructive cyclical view of municipal credit in 2018, we remain cautious and believe active sector positioning and credit selection will be important drivers of performance this year. See Figure 4 for our outlook on key municipal sectors in 2018:

Investment implications

The combination of continued synchronized global growth and a gradual pace of Fed tightening bodes well for the municipal asset class in 2018, in our opinion. We anticipate that U.S. economic expansion and federal tax cuts will be generally supportive of municipal credit fundamentals, and a sharp decrease in tax-exempt municipal issuance would provide a tailwind for municipal valuations.

However, while there is much to be optimistic about for 2018, the risks of a cyclical inflation overshoot are rising. A pickup in interest rate market volatility could test the new muni liquidity paradigm. Banks and insurance companies – paying less in federal taxes – will likely require higher relative yields, and lower bond prices, for tax-exempt municipals before becoming net buyers during a retail outflow cycle. In our view, a modest duration underweight and an emphasis on portfolio liquidity will provide active investors the ability to turn municipal valuation overshoots into opportunities.

DISCLOSURES

The term “tax-exempt” used herein refers to municipal bond federal tax-exempt income. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax.

Past performance is not a guarantee or a reliable indicator of future results.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

PIMCO does not provide legal or tax advice. Please consult your tax and/or legal counsel for specific tax or legal questions and concerns. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Any tax statements contained herein are not intended or written to be used, and cannot be relied upon or used for the purpose of avoiding penalties imposed by the Internal Revenue Service or state and local tax authorities. Individuals should consult their own legal and tax counsel as to matters discussed herein and before entering into any estate planning, trust, investment, retirement, or insurance arrangement.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2018, PIMCO.

CMR2018-0119-311746

© PIMCO

© PIMCO

Read more commentaries by PIMCO