“It’s my party, and I’ll cry if I want to

Cry if I want to, cry if I want to

You would cry too if it happened to you”

... Lesley Gore, “It’s My Party,” 1963, (It's My Party)

The year was 1963, the singer was Lesley Gore, and the song was “It’s My Party.” Clearly, that song seems appropriate given the government shutdown over the weekend. Indeed, “It’s My Party” and the blame rests with both parties in the political equation. Said song is also appropriate given that Saturday was President Trump’s one-year presidential “birthday party!” As Axios’ Mike Allen wrote, “The House was standing by in case a 1:00 a.m. vote was needed. One member told me at 8 a.m.: ‘Everybody’s grumpy, their families want to kill them, and nobody knows anything.’" Not to be outdone, Fox TV’s Jesse Watters stated on the show “The Five,” "This country’s run by imbeciles. We're $20 trillion in debt. We do this every single year." Nevertheless, a shutdown is a shutdown is a shutdown, and how the stock market reacts to it should be determined by how long the shutdown lasts. If it is short, there should be a de minimis impact on stocks. If it is drawn-out, however, investor confidence could be impacted with a concurrent headwind for equities. As for us, our sense is the shutdown will be short because of the negative feedback for ALL politicians as they face the upcoming midterm elections.

So last Wednesday we concluded our comments on Neil Cavuto’s “Coast to Coast” Fox TV show by noting, “We worked in the D.C. Beltway years ago, but still have pretty good contacts on Capitol Hill. And as of Tuesday night we were told that there were not enough votes to prevent a government shutdown.” B-i-n-g-o... our contacts got it dead right as the government did shut down at midnight last Friday. Now the history of government shutdowns is that they tend to be short. The longest took place between 12/15/95 and 1/6/96, lasting 21 days. The shortest, at only one day, occurred in 1982, 1984, 1986, and 1987. The average decline during the shutdown for the S&P 500 (SPX/2810.30) was -0.6%, the median decline was 0.0%, with a positive percentage for the SPX of 44.4% of the 18 shutdowns going back to 1976.

So how is the shutdown going to affect the economy? Well according to Goldman Sachs’ Alec Phillips:

A shutdown would have a modest economic impact, provided it does not last very long. We estimate that each week of shutdown would reduce real GDP growth in Q1 by 0.2 (percentage points, quarter over quarter) annualized. The effects would be reversed the next quarter, however. Shutdowns have also tended to have modest effects on financial markets. Most of the notable shutdowns over the last few decades coincided with debt limit deadlines. Even so, those led to only modest and temporary declines in equities and even smaller effects in Treasury yields and the dollar. With the debt limit deadline farther away, we would expect a muted initial reaction in financial markets to a shutdown.

Consequently, this shutdown should be short and should not affect our short-term market call in that stocks should trade higher into February, where our models suggest the first point of downside vulnerability.

Moving on, irrespective of the shutdown, there is an acceleration in synchronized global growth, most notably in China. That acceleration is causing the world’s GDP growth estimates to ratchet upward. Here in our country, 1Q18 GDP growth of 3.0% or more seems increasingly likely, which would make it four 3% GDP growth quarters in a row. Given that, and the corporate tax cuts, is it any wonder earnings estimates for the S&P 500 are moving up? Indeed, bottom-up (operating) earnings estimates for 4Q17 have improved to a solid +6.9% year-over-year. Moreover, those same earnings estimates have leaped to $150 for all of 2018, with one bulge-bracket investment bank estimating $157. If that estimate is correct, it implies the S&P 500 is trading at 17.9x forward earnings (2810÷ $157=17.9).

Speaking to earnings, in last Thursday’s “Morning Tack” we wrote:

We would also note that four companies dominate the S&P 500, accounting for 10% of the index, and trade at an average P/E of ~29x earnings, skewing the P/E to the higher side (AMZN, FB, GOOG, MSFT, as reported by Barron's). There's also a huge amount of cash on corporate balance sheets that implies a higher P/E multiple since there are no earnings generated from that cash. According to McKinsey & Company, "Removing the four companies mentioned from the calculation and adjusting for the excess cash that companies hold as they await changes to tax laws before repatriating foreign profits, reduces the current P/E ratio to 16.9x." So no, we are not worried about the valuation levels of the major indices.

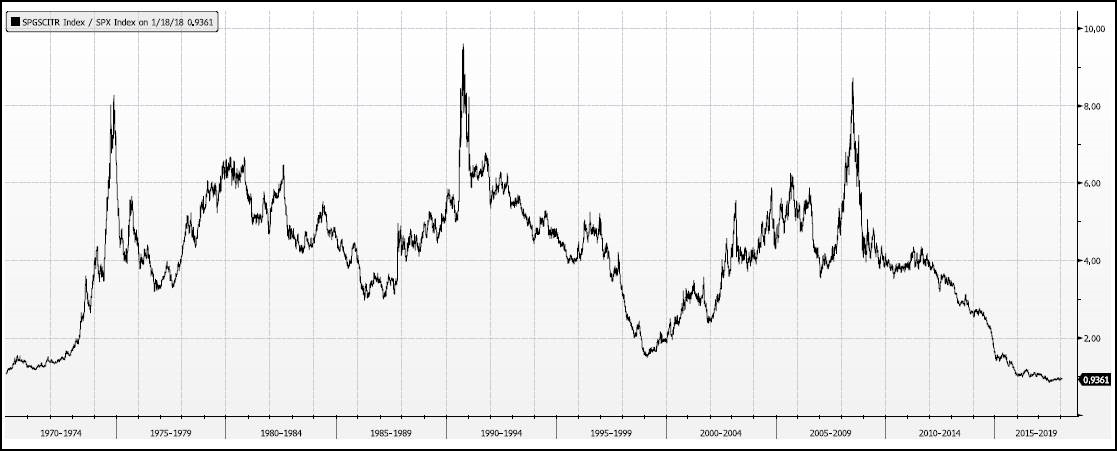

Meanwhile, Retail Sales surged at a 11.3% rate in 4Q17, Consumer Comfort is at a multi-decade high, Consumer Credit increased at a 9.2% annualized rate in November, the NFIB’s small business survey of compensation is near all-time highs, inflation is picking up, the U.S. dollar is falling, and the list goes on. Consistent with these metrics, investors are buying into the Technology and Industrial sectors while shifting out of the defensive sectors like Telecom and Utilities. Investors are also buying emerging markets and some commodity-centric assets. Not surprisingly, that is what DoubleLine Capital’s Jeffrey Gundlach is recommending for 2018, namely emerging markets and commodities, themes we have been featuring for quite some time. Manifestly, commodities relative to stock are as cheap as they have been in a long time (see chart 1 below).

The call for this week: Friday’s option expiration usually leads to a lower Monday open for stocks on position squaring. That is what is happening this morning with the preopening futures down marginally. Our conversations with international accounts suggest they are more worried about the government shutdown than our domestic institutional accounts. Ergo, if stocks decline during the morning, look for a rally after the European close. The real question is, “Will U.S. investors continue to ignore the shutdown like they did in 2013?” 2800, 2767 (gap), 2750 (gap), 2736, 2723 (gap), 2714 (gap) on the S&P 500 Index are support levels.

Click here to enlarge

Additional information is available on request. This document may not be reprinted without permission.

Raymond James & Associates may make a market in stocks mentioned in this report and may have managed/co-managed a public/follow-on offering of these shares or otherwise provided investment banking services to companies mentioned in this report in the past three years.

RJ&A or its officers, employees, or affiliates may 1) currently own shares, options, rights or warrants and/or 2) execute transactions in the securities mentioned in this report that may or may not be consistent with this report’s conclusions.

The opinions offered by Mr. Saut should be considered a part of your overall decision-making process. For more information about this report – to discuss how this outlook may affect your personal situation and/or to learn how this insight may be incorporated into your investment strategy – please contact your Raymond James Financial Advisor.

All expressions of opinion reflect the judgment of the Equity Research Department of Raymond James & Associates at this time and are subject to change. Information has been obtained from sources considered reliable, but we do not guarantee that the material presented is accurate or that it provides a complete description of the securities, markets or developments mentioned. Other Raymond James departments may have information that is not available to the Equity Research Department about companies mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this presentation’s conclusions. We may perform investment banking or other services for, or solicit investment banking business from, any company mentioned. Investments mentioned are subject to availability and market conditions. All yields represent past performance and may not be indicative of future results. Raymond James & Associates, Raymond James Financial Services and Raymond James Ltd. are wholly-owned subsidiaries of Raymond James Financial.

International securities involve additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets.

Investors should consider the investment objectives, risks, and charges and expenses of mutual funds carefully before investing. The prospectus contains this and other information about mutual funds. The prospectus is available from your financial advisor and should be read carefully before investing.

© Raymond James

© Raymond James

Read more commentaries by Raymond James