he U.S. corporate bond market is a massive, diverse asset class that has seen decades of significant growth. In the past four years alone, the market has increased from around $4 trillion to $5.8 trillion. This growth, however, has been accompanied by a steady decrease in overall credit quality. Investors should watch this trend closely, especially when weighing the potential risks and benefits of passive versus active management in their credit portfolios.

Crucially, the share of the U.S. investment grade (IG) nonfinancial bond market that is rated BBB (i.e., the lowest credit rating still considered IG) has increased to 48% in 2017 from around 25% in the 1990s. Drilling down into the riskiest part of the BBB market segment, the universe of low BBB rated bonds is now bigger than that of all BB rated bonds (i.e., the highest-rated speculative grade bonds) combined. (Read our investor education piece on corporate bonds for a quick refresher on credit ratings, issuers, credit spreads, risks and reasons to invest.)

Average credit fundamentals also declining

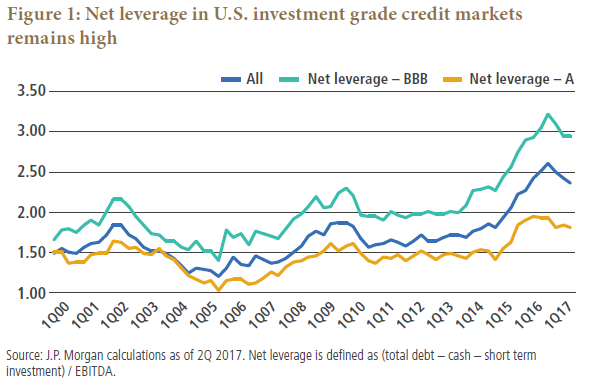

Back in 2000, net leverage of BBB rated nonfinancial corporates was 1.7x on average; in 2017, net leverage for these companies was 2.9x (see Figure 1; net leverage is defined as (total debt – cash – short term investment) / EBITDA (i.e., earnings before interest, taxes, depreciation and amortization)). This suggests a greater tolerance from the credit rating agencies for higher leverage, which in turn warrants extra caution when investing in lower-rated IG names, especially in sectors where earnings are more closely tied to the business cycle.

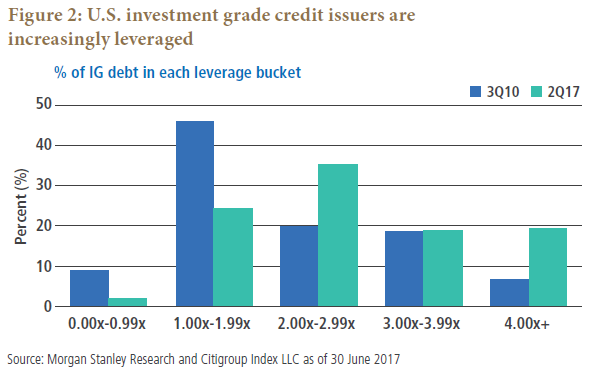

The higher leverage among U.S. investment grade issuers should also be seen in context: Back in 2010, only 6.6% of the IG nonfinancial market had net leverage greater than 4.0x, but as of 2017, that share increased to 19% (see Figure 2). In addition, only 26% of IG nonfinancial debt is leveraged less than 2.0x as of 2017, compared with 55% in 2010.

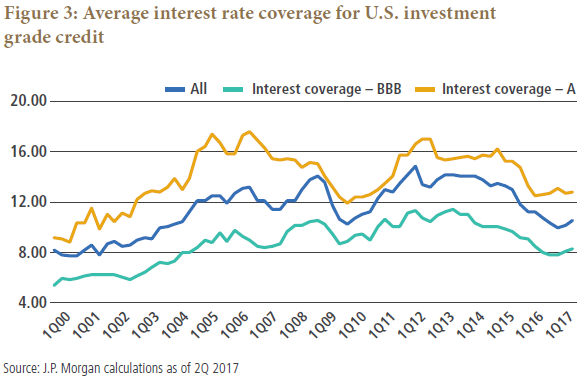

Average interest rate coverage for BBB issuers has improved since 2000, to 8.2x from 5.3x, due to record low interest rates (see Figure 3). That said, interest rate coverage has actually been deteriorating overall in the past few years; it reached 11.4x in 2013.

These negatives are partially offset by average net-debt-to-enterprise values. On that basis, the credit deterioration has been significantly less pronounced: Average net debt/EV has gone from 23.9% 10 years ago to 26.8% five years ago and 29.5% in 2017, attributable to supportive equity prices. This is an important consideration given the strong historical correlation between credit spreads and net debt/EV ratios.

Furthermore, the long-term information ratio of U.S. BBB companies has historically been even better than that of A rated companies because of the excess premium built in for higher downgrade risk. Based on data back to 1997, the Sharpe ratio (risk-adjusted return) of BBBs has been +0.39 versus +0.17 for A rated companies. Using data back to just 2007, the difference is even greater: a Sharpe ratio for BBBs of +0.70 versus +0.14 for As.

Beware fallen angel risk

In 2016, 18% of low BBB rated companies were downgraded below investment grade and became part of the high yield sector, mainly due to lower commodity prices. (Corporate bonds that have been downgraded from investment grade to speculative grade are known as “fallen angels.”) Based on historical issuance averages and migration statistics, this suggests that close to $80 billion in BBB rated bonds potentially could be downgraded in 2018. In many cases, downgrades and even just negative outlooks from the rating agencies have an outsized effect on spreads.

To avoid the potentially negative impact on returns, it is important for investors to recognize fallen angel risk. Yet, the number of corporate bond issuers has expanded by 33% in the past five years and by 67% in the past 10 years, which suggests that bond selection in investment grade corporates has become more challenging.

Active portfolio managers, unlike passive managers, can invest in bonds outside of the benchmark indexes. And active managers with a deep bench of credit research analysts can aim to cover as many issuers as possible in an effort to select the most attractive bonds and determine which are at risk of falling below investment grade – and correspondingly, which have potential to migrate up from high yield to investment grade (such bonds are known as “rising stars”).

Actively selecting corporate sectors and issuers

As a large active bond manager, PIMCO is in our view ideally positioned to manage the risks in corporate fixed income investing, including in the complicated universe of BBB bonds.

The credit team focuses on companies that are supported by high barriers to entry and pricing power, exhibit above-trend growth and have management teams that act in the best interest of bondholders. Such companies, in our opinion, have a greater ability to reduce leverage in an organic way and retain their investment grade status.

With that in mind, we find many compelling BBB bonds in the U.S. marketplace today. For example, we see value in select healthcare, media, telecom and pipeline companies. However, we are cautious on BBB companies in sectors where credit fundamentals have deteriorated overall and where barriers to entry, asset quality and pricing power tend to be lower, such as retail/grocery, certain niches in technology, consumer noncyclicals and industrials.

Investment implications

We think investors may want to consider taking a more cautious and selective approach to BBB nonfinancial corporate bonds, particularly those in the low BBB rated segment where the risk of downgrades is higher and the room for error is lower. Of note, we are not advocating a generic underweight to BBBs, but rather suggesting a more selective approach in this environment. We still see opportunities in select BBB nonfinancials, especially in sectors with high barriers to entry, above-trend growth and strong pricing power.

Our views on the BBB bond market are part of our overall cyclical view on credit, which has us focused on bottom-up ideas in an environment where generic credit is less attractively priced and potentially vulnerable in the event of a downturn. Read our latest Cyclical Outlook,“Peak Growth,” for more on our macro forecasts and the investment takeaways.

As the room for error in selecting BBB corporate bonds narrows and the size of the low BBB rated segment grows, managing idiosyncratic risk is more important than ever. In that context, we believe active management of corporate bond portfolios, supported by a large, experienced team of credit analysts, can be a highly effective approach.

© PIMCO

Read more commentaries by PIMCO