SUMMARY

-

Global political developments continued to capture headlines.From rising optimism about the passage of a tax bill in the U.S. to German Chancellor Angela Merkel’s challenges in forming a coalition government, to turmoil in the Middle East, headlines over the month once more focused on geopolitical events.

-

Economic activity remained steady as data pointed toward an uptick in momentum. Growth and labor market data released in November suggested solid momentum in the U.S. economy. Similarly positive trends were also evident in Europe and Japan, where measures of economic activity were generally robust.

-

Markets were mixed, but risk sentiment remained well supported. The U.S. yield curve continued its flattening trend, and equities marched higher alongside solid third-quarter earnings and strong political momentum backing a tax bill that would, among other things, lower corporate tax rates. Notably, credit struggled – high yield bonds, in particular – and the dollar lost ground to many developed and emerging market counterparts.

In the world

Global political developments continued to capture headlines. In what markets perceived to be a vote of policy continuity, President Donald Trump nominated Federal Reserve Governor Jerome Powell to replace Chair Janet Yellen at the helm of the Fed. Yellen announced she would step down once Powell was confirmed, while William Dudley, president of the Federal Reserve Bank of New York and permanent voting member of the Federal Open Markets Committee, announced his plans to retire as soon as a successor was chosen. In Washington, momentum built around tax reform: The House passed its tax bill on a party-line vote, and the Senate’s version of the bill made its way out of committee and to the floor for debate. Political turmoil brewed elsewhere: German Chancellor Angela Merkel failed to form a coalition government following elections last month; President Robert Mugabe of Zimbabwe resigned following military intervention, marking the end of his 37-year rule; and Lebanese Prime Minister Saad Hariri resigned under mysterious circumstances during a trip to Riyadh. Meanwhile in Saudi Arabia, a corruption probe led to the arrests of prominent businessmen and members of the royal family, and a missile fired from Yemen was intercepted near Riyadh. Venezuela missed deadlines to make interest payments on its government bonds and announced that it would need to restructure its foreign debts.

Economic activity remained steady as data pointed toward an uptick in momentum. U.S. growth measures were more upbeat than previously reported: The latest estimate for GDP growth in the third quarter showed the economy expanded at a 3.3% annualized pace, the strongest reading since 2014, thanks to an acceleration in investment that boosted output. The U.S. labor market also showed signs of resilience, adding 261,000 jobs despite the impact of the recent hurricanes in certain parts of the country. The unemployment rate fell to 4.1%. Preliminary estimates for third-quarter growth in Japan were similarly optimistic: GDP expanded at an annualized rate of 1.4%, the seventh consecutive quarter of expansion, as exports offset a decline in domestic demand. In the eurozone, strong growth in manufacturing orders and a record accumulation of backlogs underpinned robust PMI (Purchasing Managers’ Index) data, indicating strong growth momentum. Bucking the trend of stubbornly low inflation in developed markets, consumer prices in the UK rose 3.0%, unchanged from the previous month and above the Bank of England’s (BOE) 2.0% target. Against this backdrop, the BOE raised its official policy rate by 0.25% to 0.5%, its first rate hike in over 10 years.

Markets were mixed, but risk sentiment generally remained well supported. In the U.S., Treasury yields were higher across much of the curve as short-term rates continued to rise, though long-term rates fell slightly. The flattening yield curve drew more scrutiny in November when the spread between short- and long-term yields narrowed further, with no shortage of theories to explain the trend. Global equities added to their gains in 2017 with another strong month, helped by solid third-quarter earnings and growing political momentum for a corporate tax cut in the U.S. The U.S. dollar, which had strengthened in the prior two months, reversed course in November and weakened against several emerging and developed market currencies, notably the euro and Japanese yen. Meanwhile, crude oil surged on rumors that OPEC might extend its previously agreed production cuts at its upcoming meeting. Not all risk assets gained, though. Higher rates and wider spreads weighed on high yield credit returns; weakness in some sectors, including telecommunications, and concerns about valuations led to outflows from the asset class.

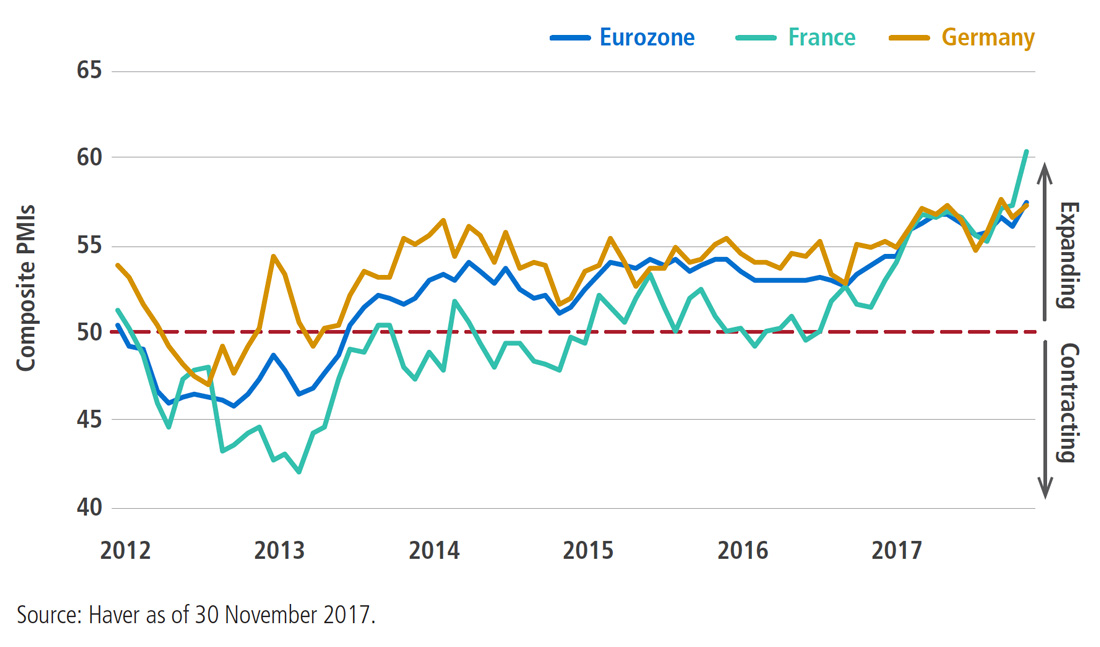

Strength in numbers

Eurozone growth momentum showed signs of acceleration in November, underscored by an uptick in the eurozone Purchasing Managers’ Composite Index (PMI) to 57.5, its highest reading since April 2011. The improvement was led by manufacturing output growth as companies worked through a backlog of orders and hiring rose to the fastest pace in 17 years. In particular, France recorded its highest PMI reading in six years, spurred by growth in the service sector. All in all, the synchronized expansion bodes well for near-term growth prospects across the 19-nation bloc. The business surveys also pointed to a pick-up in pricing pressures, which signals the potential for higher inflation – welcome news for the European Central Bank as it prepares to reduce stimulus measures.

In the markets

EQUITIES

Generally strong fundamentals boosted investors’ appetite for risk, and developed market stocks1 returned 2.2%. In the U.S.,2 stocks rallied 3.1% as tax reform took center stage and Congress made progress toward passing legislation. Japan reported its seventh consecutive quarter of growth, and equities3 climbed to a 25-year high, returning 3.2%. In Europe,4 however, solid growth supported a stronger euro, and stocks fell 2.1%.

Despite relatively stable global market conditions and a strong technical backdrop, emerging market stocks5 returned just 0.2%, weighed down by negative returns in several large economies. In Brazil,6 stocks tumbled 3.1% as investors questioned the government’s ability to pass growth-oriented pension reform. A slump in China’s bond market weighed on risk assets there, with authorities stepping up efforts to deleverage the economy, and stocks7 fell 2.2%. Stocks in India8 also fell 0.1%. A bright spot, Russian equities9 gained 1.8% amid strong corporate profits and higher crude oil prices.

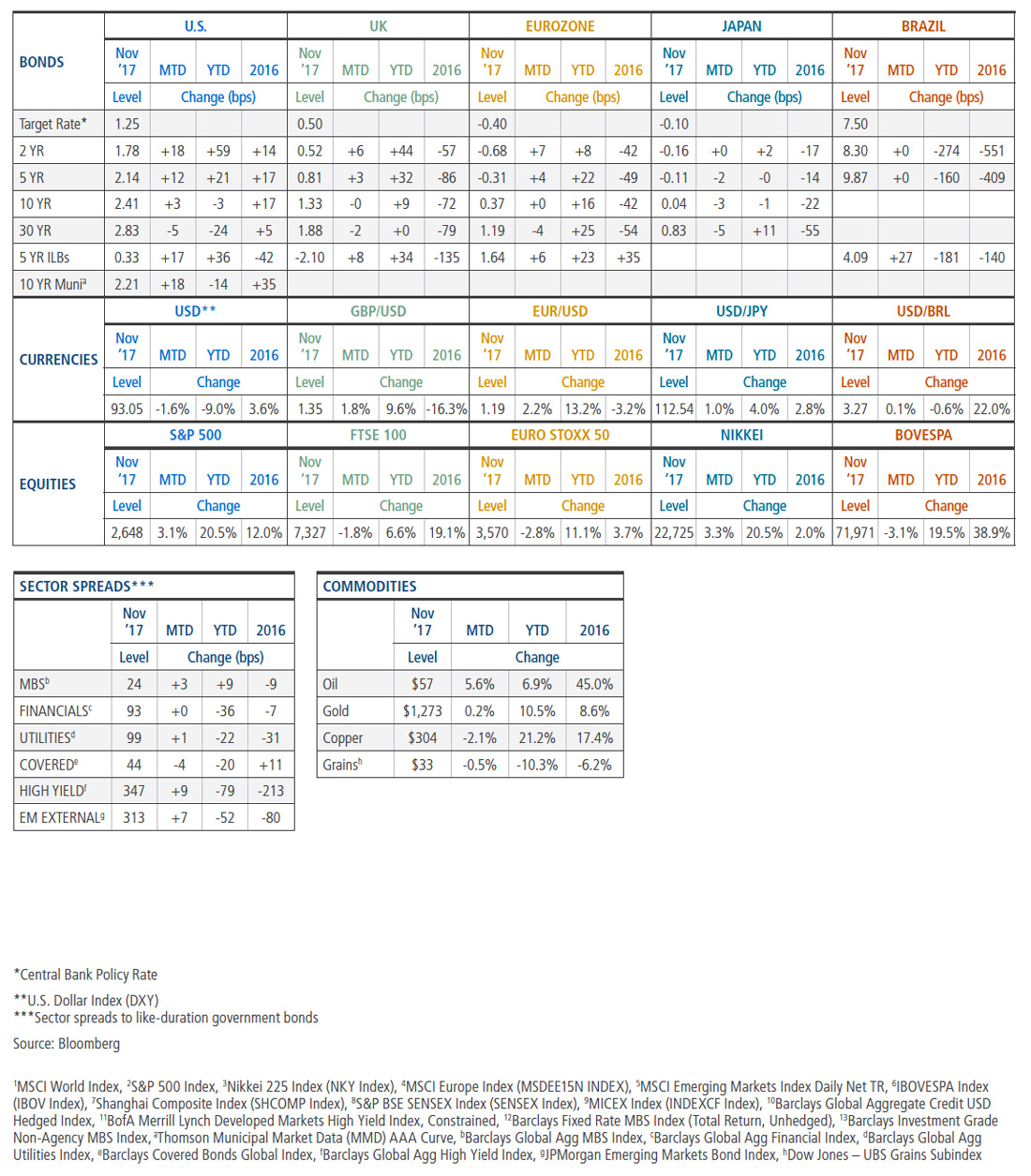

DEVELOPED MARKET DEBT

Developed market yield curves generally flattened over the month as front-end rates moved higher. In the U.S., increased optimism for tax reform and the expectation of a Federal Reserve rate hike in December pushed U.S. two-year yields 18 basis points (bps) higher. However, the 10-year yield remained little changed on concern over low inflation, driving the spread between two-year and 10-year rates to its narrowest level since November 2007. Similarly, UK and German front-end rates moved higher while 10-year yields were generally unchanged. The 10-year UK gilt yield remained steady even though the Bank of England raised its policy rate for the first time in over a decade. Still, the 10-year yield was more than 40 bps higher than its low in September.

INFLATION-LINKED DEBT

Global inflation-linked bonds (ILBs) gained and outperformed comparable nominal bonds across the major markets in November. In the U.S., real yields moved higher and the curve flattened as the minutes of the Fed's November meeting reinforced the expectation of a December rate hike. Breakeven inflation rates (BEI) ended the month broadly flat, as investors weighed the reduction in central bank accommodation against a stronger CPI and higher oil prices. In the UK, index-linked gilts gained, fueled by record investor demand at the long end of the yield curve. UK breakeven inflation rates were mixed; shorter-term inflation expectations dropped after the release of weaker-than-expected inflation readings and in response to a stronger pound.

CREDIT

Global investment grade credit10 spreads were resilient in the face of some intra-month volatility, which stemmed from falling commodity prices, concerns about China’s growth and uncertainty around U.S. tax reform. Risk appetite returned before month-end, and spreads recovered to close November only 1 bp wider, broadly supported by stable fundamentals and strong demand.

Global high yield bonds11 endured a sharp decline amid sector-specific selling and heavy retail outflows but recovered some ground later when oil prices rose, stocks rallied, and U.S. tax reform legislation progressed. Spreads ended the month 15 bps wider, and yields were up nearly 25 bps. Global high yield total returns fell into negative territory for just the second time this year, at –0.3%.

EMERGING MARKET DEBT

Local emerging market (EM) debt bounced back in November, posting positive absolute returns. The main driver: Stronger EM currencies appreciated meaningfully against the U.S. dollar. However, Turkish local rates notably lagged the index once again as diplomatic tensions between the U.S. and Turkey worsened and the central bank struggled to arrest the slide of the lira. External sovereign and corporate debt finished in moderately negative territory, driven by spread widening and higher underlying U.S. Treasury yields. Venezuela was a substantial underperformer on the external side, as the sovereign and state-owned oil company Petróleos de Venezuela (PDVSA) missed several interest payments amid deteriorating economic conditions.

MORTGAGE-BACKED SECURITIES

Agency MBS12 returned –0.14% and outperformed like-duration Treasuries by 4 bps. Headlines supporting the case for transitioning Freddie Mac and Fannie Mae to a full-faith-and-credit U.S. government guarantee (instead of the current implicit guarantee) benefited the asset class broadly, but the flattening of the yield curve weighed on higher coupon MBS. Overall, lower coupons outperformed higher coupons, 30-year MBS outperformed 15-year MBS, and conventional MBS outperformed Ginnie Mae MBS. Gross MBS issuance increased by 5.5% in November, while prepayment speeds rose 8%. Non-agency MBS outperformed like-duration Treasuries despite modest spread widening, while non-agency commercial MBS13 returned –0.38% and underperformed like-duration Treasuries by 1 bp.

MUNICIPAL BONDS

Municipals posted negative returns in November and underperformed U.S. Treasuries. The Bloomberg Barclays Municipal Bond Index returned –0.54%, bringing the year-to-date return to 4.36%. Long and intermediate maturities outperformed the front end as the yield curve continued to flatten. Municipal bond mutual fund demand remained firm, with $1.4 billion of inflows during the month, bringing year-to-date inflows to $11.9 billion. The U.S. House and Senate introduced versions of the tax reform bill, which, if passed, could materially affect muni bonds: Several proposals would limit future tax-exempt issuance, providing long-term support to the market. The municipal market was still assessing the overall potential impact of the current bills, and many issuers were rushing to the market before any changes were enacted.

CURRENCIES

Skepticism over tax reform efforts and political turmoil within the Trump administration drove down the U.S. dollar over the month. Despite rising political uncertainty in Germany, the euro saw its biggest jump since July, boosted by strong economic data. The British pound, which stumbled earlier in the month in the wake of a rate hike, ended November higher after the UK reached an agreement on the financial bill for separating from the EU. In emerging markets, the Turkish lira fell sharply as the inflation outlook worsened. Headlines about a high-profile trial of a Turkish banker in the U.S. accused of trying to evade U.S. sanctions on Iran also weighed on the currency.

COMMODITIES

November was a mixed month for commodities, and energy was the strongest performer. Crude oil continued its upward trajectory, supported by positive sentiment heading into the OPEC meeting at the end of the month. Indeed, OPEC announced an extension of its production cut through the end of 2018. Cotton and sugar were the positive outliers in agriculture, while marginally negative returns in corn and wheat capped overall sector returns. Industrial metals sold off in November, marking the second recent pause from the general 2017 rally. Overall, weaker-than-expected economic data from China and general concern about the future of demand from the region put pressure on the complex. In precious metals, gold prices remained relatively flat; support from U.S. dollar weakness was offset by the headwind of higher real yields.

Outlook**

Based on PIMCO’s cyclical outlook from September 2017.

PIMCO expects world GDP growth in 2018 to remain steady at 2.75%–3.25%, unchanged from 2017. Overall, we see a low near-term risk of recession, a moderate pickup in underlying inflation in the advanced economies, mildly supportive fiscal policies and only a gradual removal of accommodative central bank policy. However, we do see risks that could upset the calm: the aging U.S. expansion, the coming end of central bank balance sheet expansion, and China’s course following its 19th National Communist Party Congress in October.

In the U.S., we see growth below consensus at 1.75%–2.25% in 2018,albeit still above trend, as the U.S. expansion matures and slack in the labor market keeps eroding. The disappearing slack should make it difficult to sustain the current pace of job and output growth, and we also don’t expect a significant acceleration of productivity growth. We forecast core inflation to increase to 2% over the course of 2018, with some upward pressure on wages. The Fed will likely continue along its trajectory of gradual tightening.

For the eurozone, we expect growth will be in a range of 1.75%‒2.25% in 2018, significantly above trend. A key risk for the outlook is the Italian elections in the first half of 2018, although the political risk looks more contained than earlier this year, as the euroskeptical parties have toned down their rhetoric. We think core inflation will make only moderate progress toward the European Central Bank’s (ECB) target of “below but close to 2%” and forecast inflation in a range of 1.0%–1.5% for 2018. The ECB will gradually taper its bond purchases over 2018 and will likely keep policy rates at record lows until well into 2019.

In the UK, we expect growth to be in the range of 1.25%–1.75% for the balance of 2017 and into early 2018. Our base case is that a transitional arrangement will smooth the UK’s separation from the European Union and that growth will reaccelerate as business confidence picks up. Having raised rates already in 2017, the Bank of England (BOE) will likely follow a very gradual path higher in coming years.

Japan’s GDP growth is expected to moderate somewhat to 0.75%–1.25% in 2018 but remain above trend, reflecting ongoing fiscal and monetary support as well as decent global growth. We think inflation will creep up toward 1% over the next year as wage growth accelerates, but the 2% inflation target is likely to remain out of reach. A key swing factor will be the succession of BOJ governor Haruhiko Kuroda. We expect the Bank of Japan (BOJ) to nudge its yield target for 10-year Japanese government bonds higher from the current 0% later in 2018.

In China, we expect growth to decelerate in 2018 from the current 6.6% pace. Our wide forecast range of 5.5%–6.5% reflects uncertainty about the leadership’s prospective stance on financial stability, deleveraging and economic growth. If the leadership continues to focus on suppressing volatility, growth could hold up at higher levels, but if policy pivots, the changes could weigh heavily on growth and lead to greater tolerance for a depreciating Chinese yuan.

In the emerging markets (EM) of Brazil, Russia, India and Mexico,we expect growth to rise to 4% in 2018, slightly above consensus, as recoveries in Brazil and Russia become more entrenched. Overall, most emerging economies are at a different stage of the economic cycle than developed economies and should still benefit from relatively easy global policy conditions. We expect continued disinflation, with headline CPIs falling to around 4.2% in 2018.

** Note that all GDP and inflation forecasts will be subject to revision when conclusions from PIMCO’s December cyclical forum are published later this month.

In sight

The Price is REIT

The 2017 equity rally has left one asset class behind: real estate investment trusts (REITs). The return on the Dow Jones U.S. Select REIT Total Return Index is lagging that of the S&P 500 by nearly 1,100 basis points (bps). The languishing retail REIT sector and the turbocharge stocks have received lately from U.S. tax reform account for much of this underperformance. But analyzing REITs in a real asset framework shows their valuations look attractive.

Equity REITs, which collect rental payments on commercial properties, are basically long-term real assets, and their prices generally rise with inflation. So their expected yields can be compared to the real yields on other financial assets, which can be benchmarked by Treasury Inflation-Protected Securities (TIPS) plus a credit spread and an equity risk premium. When the adjusted funds from operations (AFFO) yield on REITs is materially above the sum of these three components, REITs are typically undervalued. The current spread of roughly 80 bps is solidly above the 15-bp long-term average, and aside from the 2008 financial crisis, is near its highest since June 2004, after which REITs strongly outperformed the S&P 500.

Appendix

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation- Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

© 2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO