Our portfolios have had significant exposure to the Technology sector since the first quarter of 2016. Tech remains one of our biggest sector exposures both on an absolute and relative basis. Our substantial overweight in Technology surprises some of our investors because RBA generally does not make a habit of investing in overvalued or hyped sectors.

Our significant overweight in Tech stocks has been based on one fact: Technology has historically been the best performing sector when overall corporate profits accelerate. Right in step with history, Technology has been the best performing sector since the US profits cycle troughed in 4Q15 and the global profits cycle troughed in 2Q16. The Tech sector’s recent outperformance is not atypical relative to other periods during which profits accelerated.

The historical performance of the Tech sector is the sector’s dirty little secret: the Tech sector is actually a deep cyclical sector and, over multiple cycles, investors seem to habitually confuse that deep cyclicality for stable growth. They appear to be doing it again during this cycle.

Underestimating Tech’s cyclicality

The secular, long-term earnings growth rate of the Technology sector is higher than that of some other sectors, but the sector’s earnings stream is so highly cyclical that one must be careful regarding the time period used when measuring growth. Based on Tech sector valuations, history suggests that investors tend to focus on Tech’s long-term growth and ignore the sector’s deep cyclicality. That valuation strategy works fine so long as the sector’s profits are accelerating, but unravels when profits decelerate. The Tech sector’s history is riddled with disappointment.

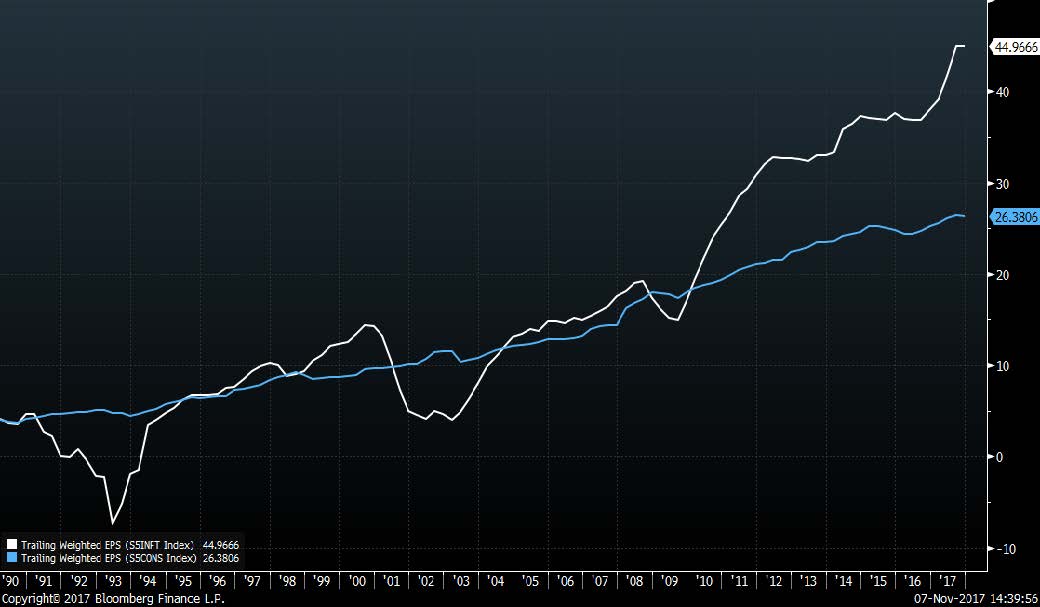

Chart 1 compares the long-term earnings stream of the S&P 500® Information Technology sector (white line) with that of the S&P 500® Consumer Staples sector (blue line). At the peak of a cycle (like today?) the Technology sector looks to be a superior growth sector to Consumer Staples. However, the Technology sector’s growth quickly loses momentum during profits recessions. Tech looks to be a superior grower versus Consumer Staples only toward the peak of a cycle.

CHART 1:

Trailing EPS: S&P 500® Technology vs. Consumer Staples (Sep 1990 – Sep 2017)

Source: Richard Bernstein Advisors LLC., Bloomberg Finance L.P.

Source: Richard Bernstein Advisors LLC., Bloomberg Finance L.P.

Recent experience isn’t unusual

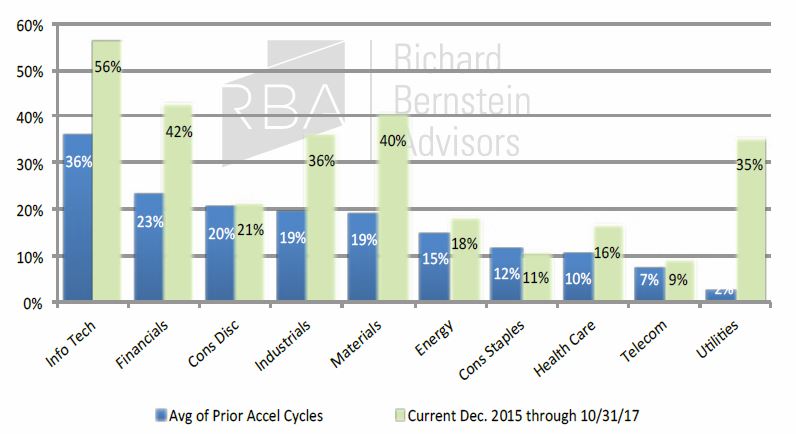

Chart 2 shows the historical average performance of S&P 500® sectors during periods in which profits accelerated compared to the current profits cycle thus far. Technology and Financials historically ranked first and second, which partially explains why those two sectors have been so heavily weighted within our current portfolios.

CHART 2:

S&P 500® Sectors: Average Performance

During Periods of Accelerating Profits (Sep. 1989 - Oct. 2017)

Source: Richard Bernstein Advisors LLC., Standard & Poor's. Bloomberg Finance L.P.

*Real Estate not included as a separate sector as its historical data prior to Sep 2016 is incorporated within the Financial Sector and full standalone data is not available.

“But they’re changing the world!” We’ve heard one that before.

“This time is different” is a short-hand way of saying that business cycles no longer exist. Whether it is optimistic themes like the 2000’s “new economy”, 1998’s emerging markets, or 2007’s “housing prices never go down” or pessimistic themes like the 1987 Crash, the 1989 S&L Crisis, or 2008’s housing collapse and “new normal”, the common thread is that the business cycle no longer exists and traditional analyses no longer apply.

Of course, business cycles are not extinct. Even the current cycle is more typical than many investors believe. Admittedly, the current cycle has been elongated and has had lower amplitude because of the lack of credit creation following the deflation of the global credit bubble, but the high unemployment and the general business malaise that characterized the depths of the last recession have significantly improved as the cycle matured. As we head to the latter stages of this cycle, the risk of boom seems larger to us than the risk of recession.

With that history in mind and remembering that outperformance often drives optimism, investors should be skeptical of the notion that today’s technology companies are somehow changing the world. The stock market doesn’t care about “changing the world”. The stock market cares only about profits, and it is a reasonable assumption that technology profits will be as cyclical as they historically have been, and that the stocks will underperform when that cyclicality reappears.

Past cycles show that the sector is clearly a cyclical sector (see Chart 3). Technology was the epicenter for 2000’s bear market, and the sector fell about 80%. 2008’s bear market had little to do with the Tech sector (it was a credit-induced bear market and recession), but the Tech sector still fell more than 50%. Earlier cycles show similar performance characteristics.

CHART 3:

S&P 500® Technology Index (Weekly from Sep 1997 – Nov 7, 2017)

Source: Richard Bernstein Advisors, LLC., Bloomberg Finance L.P.

For now, party on!

Our substantial overweight of Technology shares within client portfolios has been based on our accepting that Tech is a very cyclical sector, and this cycle’s outperformance mirrors the historical experience we anticipated. Our continued overweight of the Tech sector seems justified because the US and global profits cycles continue to accelerate. It simply makes sense to own cyclicals during a cyclical upturn.

It is likely that investors will get carried away with the sector’s performance and earnings growth, and will extrapolate trend while believing that this cycle is somehow different. Investors seem primed to get burned yet again in Technology shares, but it is still probably too early to worry.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index.

The S&P 500® Index is an unmanaged, capitalization- weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

Sector/Industries: Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s. The GICS structure consists of 11 sectors, 24 industry groups, 68 industries and 157 sub-industries.

About Richard Bernstein Advisors

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $5.8 billion collectively under management and advisement as of October 31st 2017. RBA acts as sub advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund and the Eaton Vance Richard Bernstein All Asset Strategy Fund and also offers income and unique theme oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial Renaissance® ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS, Merrill Lynch, Morgan Stanley Smith Barney, Wells Fargo, RBC, Janney and on select RIA platforms. RBA’s investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.

© Richard Bernstein Advisors LLC. All rights reserved. PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors

Source: Richard Bernstein Advisors LLC., Bloomberg Finance L.P.

Source: Richard Bernstein Advisors LLC., Bloomberg Finance L.P.

Source: Richard Bernstein Advisors, LLC., Bloomberg Finance L.P.

Source: Richard Bernstein Advisors, LLC., Bloomberg Finance L.P.