Hurricane Maria and the case of Puerto Rico

The Commonwealth of Puerto Rico was already in the midst of a complex bankruptcy process when it was devastated by Hurricane Maria, and addressing urgent needs, including restoring power and clean water, are the top near-term priorities. Looking ahead, an effective long-term rebuilding effort will be the key to restoring economic growth to the island and preventing more-rapid depopulation. To this end, municipal bondholders and citizens appear aligned in support of many policy initiatives that could boost prosperity over the next decade, including Medicaid equality (in terms of federal funding relative to states), relief from the Jones Act and the possible reintroduction of certain tax benefits whose expiration helped precipitate the island’s economic decline. Ideally such measures would be lasting or permanent to avoid future policy cliffs and give individuals and businesses the confidence to reinvest in the commonwealth.

PIMCO has long eschewed Puerto Rico government debt, given our view that market prices underappreciated the potential difficulties of servicing the debt burden. With Puerto Rico GO (general obligation) bond prices down more than 40 points since March, trading for roughly 30 cents on the dollar, we think valuations are looking more favorable than in the past. Still, the road to conviction is long and complex. Investors considering Puerto Rico GO debt have much to think about: In addition to an undefined capital structure, ambiguity about the security of specific liens and an untested bankruptcy process, investors must also consider the potential size, scope and form of the federal government response to a natural disaster or other unforeseen event and the impact it may have on the commonwealth’s demographics and economy for years to come.

Policy shifts (and lack thereof) drive healthcare-related muni performance

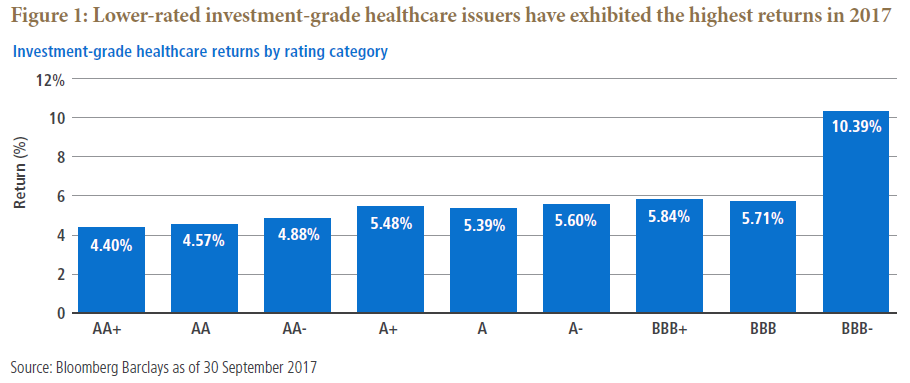

The U.S. presidential election in 2016 signaled big changes in U.S. healthcare policy – chief among them a potential repeal of the Affordable Care Act (ACA), including a roll-back or cap on Medicaid expansion. A unified vision among the legislative majority in the Senate has proved elusive, however, making a large-scale healthcare policy shift less and less likely as the year progresses. This has benefited municipal not-for-profit healthcare markets and issuers, which have outperformed the broader investment-grade muni market this year. Lower-investment-grade (‘BBB’) credits, primarily safety-net and “charity care” providers, have led the way (see Figure 1), with spreads now back within striking distance of pre-election lows.

While Medicaid headline risk has abated, other policy risks could squeeze profit margins for lower-rated safety-net and charity-care providers. Seventeen states are considering funding freezes or reductions that would disproportionately hurt these issuers, as would proposed cuts to the federal 340B Drug Pricing Program (which subsidizes drug prices and financial performance for many).

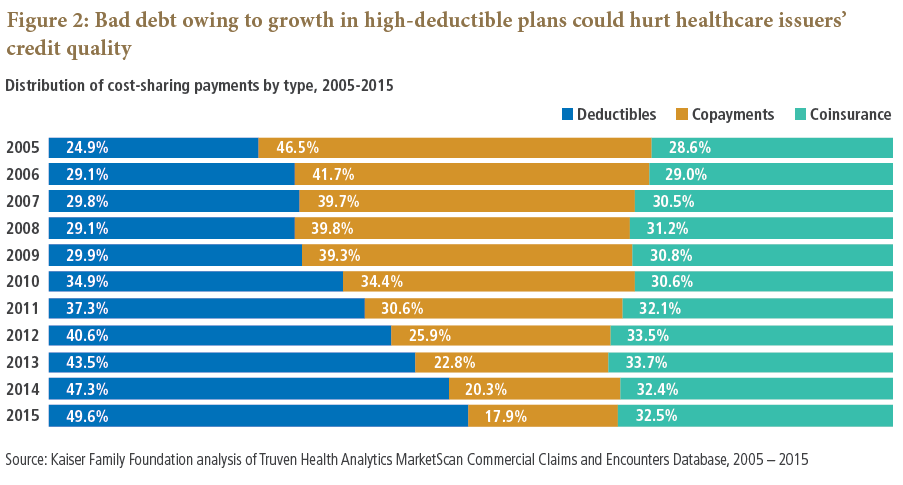

President Trump’s recent executive order expanding the use of association health plans and short-term insurance will likely cause a modest rise in uncompensated care, and the growing prevalence of high-deductible health plans (a trend in place well before the 2016 election) will likely also result in higher bad debt expenses for hospitals (see Figure 2).

Given these trends, PIMCO is constructive on high quality healthcare systems with diverse revenue streams and payer mixes that are less reliant on government programs. While safety-net and charity-care providers have benefited from the lack of healthcare policy progress in 2017, we are underweight these bonds at current valuations given the other policy risks they face. It’s worth noting that the recently proposed House tax reform plan may eliminate the ability for health care providers to access the tax-exempt financing market in the future. If this is enacted, it will likely raise funding costs and squeeze margins for all health care issuers, and the credits with the most to lose are likely the lower-rated safety net providers.

Tax reform fears that spurred muni outflows haven’t been realized

Tax reform concerns contributed to $17 billion in outflows from open-end muni mutual funds in the six weeks following the 2016 election, and these fears appear to have lingered. Despite the relatively benign interest rate environment this year, only $15 billion has returned to the market.

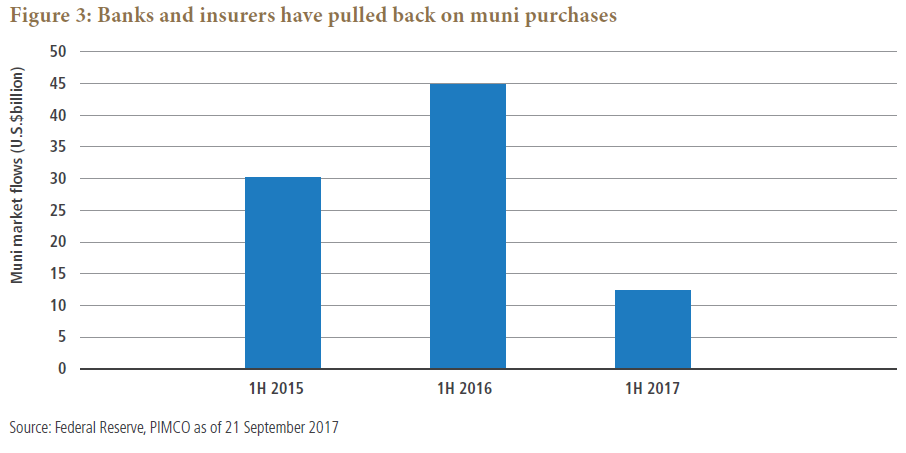

Among investors given pause are banks and insurance companies, which have been buying federally tax-exempt munis at a significantly slower pace in 2017 (see Figure 3). The planned reduction in the corporate tax rate, along with large insurance claims related to natural disasters, remain near-term headwinds to additional allocations.

Meanwhile, the probability that tax reform will reduce the value of the muni tax exemption continues to shrink; in fact, the House tax plan in its current form would likely increase the value of the exemption due to reduced forward supply. Hospitals, private higher education and private activity issuers all would lose the ability to issue tax-exempt bonds. Advance refundings of existing outstanding debt issues would also be prohibited beginning in 2018. In aggregate, this policy mix could lead to a 25% (or more) decline in tax-exempt new issue supply over the next few years. While the ultimate policy path for tax reform still remains difficult to predict, the House plan has introduced a balance of risks for muni investors to consider: Long thought to be solely a downside risk to munis, tax policy changes could in fact be a positive catalyst for investors, with lower supply leading to higher valuations.

A steeper curve means richer front-end valuations – making longer maturities more attractive

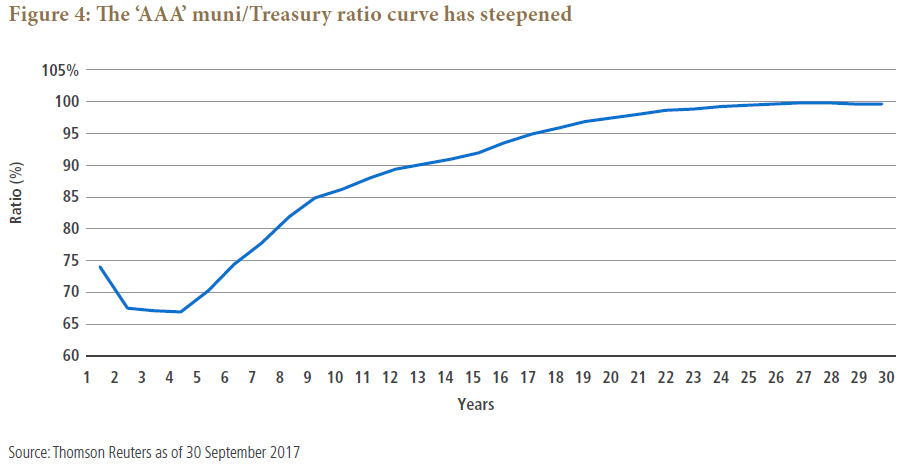

Because banks and insurers tend to buy longer-dated maturities, their absence has contributed to a steeper curve for muni bonds (see Figure 4). We currently favor 20- to 25-year maturities over the richer front end – a relative value call that is evident in the ratio curve and aligns with PIMCO’s Cyclical Outlook. Over the next year, we expect the Federal Reserve to raise the policy rate two to three times, which will likely put more pressure on the front end of the curve relative to the long end.

Adjusting the sails: key investment takeaways

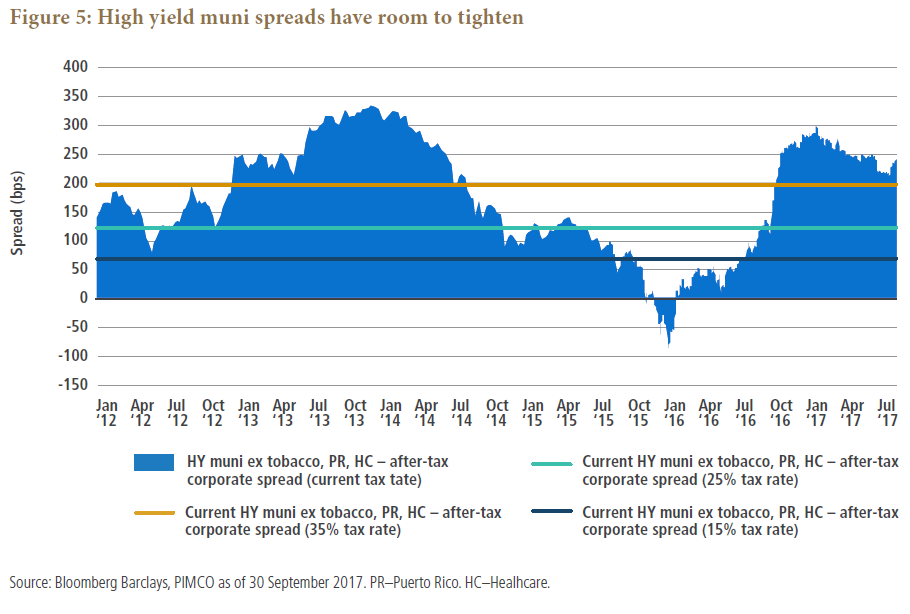

Tight valuations in other U.S. credit markets are informing our muni portfolio positioning, with the relative underperformance of municipal credit spreads since the 2016 election pointing to further upside in spread tightening (see Figure 5). We remain constructive on “traditional” high yield (‘BB’ rated) munis (i.e., excluding MSA tobacco, Puerto Rico and healthcare) and continue to prefer revenue bonds over GOs, with some exceptions. For example, with both Chicago and Illinois GO bonds, we see compelling valuations combined with fundamental uplift in the credit trajectory over our cyclical (six- to 12-month) horizon. Lastly, we continue to focus on identifying opportunities arising from the complexity premium in MSA (Master Settlement Agreement) tobacco asset-backed bonds.

What does adjusting the sails mean for an active municipal bond manager? For us, it entails closely monitoring changes in the market, adapting our outlook in response and repositioning our portfolios accordingly. With this approach, we look to help investors weather periods of turbulence while positioning them to seize opportunities that may emerge in their wake.

Muni positioning snapshot

-

Underweight: safety-net providers and not-for-profit healthcare issuers

-

Modestly underweight: duration

-

Constructive on ‘BB’ rated securities; longer maturities versus the rich front end; structurally overweight revenue bonds versus GO bonds

-

Constructive on select GO bond risk with positive credit trajectory (Chicago and Illinois)

- Identify opportunities in MSA tobacco bonds given the complexity premium associated with less-predictable timing of cash flows

- Provide opportunistic liquidity to harvest bid/ask spreads

To receive up-to-date municipal market insights from PIMCO, subscribe to our Muni Insights list.

(Generally one to three key emails per quarter. Unsubscribe at any time.)

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Certain U.S. government securities are backed by the full faith of the government. Obligations of U.S. government agencies and authorities are supported by varying degrees but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Management risk is the risk that the investment techniques and risk analyses applied by PIMCO will not produce the desired results, and that certain policies or developments may affect the investment techniques available to PIMCO in connection with managing the strategy.

The credit quality of a particular security or group of securities does not ensure the stability or safety of an overall portfolio. The quality ratings of individual issues/issuers are provided to indicate the credit-worthiness of such issues/issuer and generally range from AAA, Aaa, or AAA (highest) to D, C, or D (lowest) for S&P, Moody’s, and Fitch respectively. Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. No representation is being made that any account, product, or strategy will or is likely to achieve profits, losses, or results similar to those shown. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. PIMCO provides services only to qualified institutions and investors. This is not an offer to any person in any jurisdiction where unlawful or unauthorized. | Pacific Investment Management Company LLC, 650 Newport Center Drive, Newport Beach, CA 92660 is regulated by the United States Securities and Exchange Commission. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

CMR2017-1024-296894

© PIMCO

Read more commentaries by PIMCO