Despite the upswing in economic growth, certain banks in Europe continue to hold high levels of non-performing loans (NPLs) on their balance sheets. The European Central Bank (ECB) has acknowledged this problem and has made addressing bank asset quality issues a key priority for the supervisory group. While there is broad agreement that banks should remove NPLs, how to do so remains in flux. We think more creative solutions need to be considered – and equity investors should be more proactive.

Quick cleanup makes sense

The leverage of financial institutions, together with their importance to the overall economy and reliance on retail deposits, justifies a swift cleanup of NPLs, which by nature have highly volatile cash flows.

When a performing loan becomes non-performing, the likelihood that the original principal won’t be fully repaid increases. At the same time, the cash flow from the loan likely extends if resources are not devoted to special servicing, and becomes more volatile. Recovery thus incurs expensive legal costs. The buyer base of NPLs is also fairly limited with higher funding costs versus bank’s cost of funds. As such, holding a non-performing loan requires a higher risk premium, all else equal.

Different approaches to NPLs

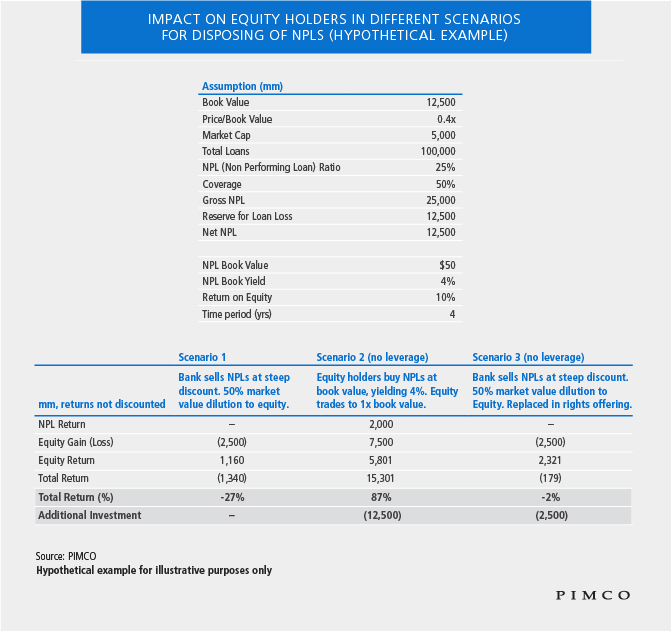

Generally speaking, two approaches have been used to deal with NPLs to date: Keep the loans on balance sheet and write them down over time (earning your way out of trouble), or sell them immediately at prices below book value (potentially at distressed levels). While there are always systemic and political considerations, from a current shareholder’s perspective, neither approach may be optimal.

Rather than jump to one of these methods, we think it makes sense to consider the trade-off between dilution over time, and owning the NPLs outright, closer to book value. Owning NPLs outright also give stakeholders the ability to mitigate extension risk through special servicing to resolve NPLs and unlock value.

Theoretically, a bank could consider spinning off the NPLs at the lowest price possible without having to raise capital. We acknowledge that a spin-off is difficult, and realistically, it could look more like a rights offering with equity holders bridging the valuation gap between current book value and distressed bid value. Equity investors could then choose either to buy the NPLs (bridge the valuation gap), or get diluted through capital raises.

While the equity holders may experience low returns, or a small loss on the NPLs following the disposal, their shares in what is now a “good bank” could potentially significantly increase in value, offsetting any losses on the NPLs. There are numerous factors that must be considered; the table illustrates this concept.

Challenges remain

Although the economics of this approach may be compelling, there are structural challenges to implementation. Local jurisdictions would need to have the appropriate financial framework and accounting regulations in place to facilitate the transfer of NPLs to equity holders. There could also be legal risks if retail investors suffer losses.

However, when faced with dilution, many shareholders would naturally be assertive in requiring management to protect their interests. If the theoretical spinoff of NPLs could be achieved in a liquid construct, such as tradeable equity or notes, it could also be possible for equity holders to fund the position (potentially with funding from the selling bank), reducing their initial outlay.

Either way, decisions on how to address Europe’s NPL problem will likely occur over the next 18 to 24 months. Our view is that spinning off the bad loans to existing equity holders, or more likely, allowing them to bridge the valuation gap between distressed bid price and current book value through a rights offering, should at least be considered as an option.

Joshua Anderson is one of the lead portfolio managers for PIMCO’s mortgage- and real-estate-related opportunistic strategies. Stacey Shi is a portfolio manager on PIMCO’s mortgage team.

DISCLOSURES

All investments contain risk and may lose value. Investing in the market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets.

References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included. Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice. Investors should consult their investment professional prior to making an investment decision.

© PIMCO

© PIMCO

Read more commentaries by PIMCO