I first became aware of Frederick “Shad” Rowe, captain of Dallas-based Greenbrier Partners, by reading his brilliant comments in Forbes magazine decades ago. While Shade no longer writes for Forbes, his stock market insights are available via his monthly letter to the clients in his investment partnership. I always look forward to reading it, and last month’s letter was no exception. Shad actually called me a number of years ago when I began using some of his prose from the old Forbes days, and we have been friends ever since. As a sidebar, he hosted the GIBI Conference (Great Investors Best Ideas) last week where a cast of Wall Street notables spoke. I attended that conference a year ago and had a fabulous time at his dinner the night before the conference for the speakers where we dined with folks like Michael Price, Mario Gabelli, Susan Byrne, David Einhorn, T. Boone Pickens, Gretchen Morgenson, etc. Regrettably, I could not attend this year due to previous commitments, yet I wish I had attended given the speaker lineup; but I digress.

It was Shad that first introduced me to the concept of “Better, Faster, Cheaper.” As he wrote in his September letter:

Our companies are still doing things better, faster, cheaper and for the customer. They have largely vanquished their competition. The biggest threat they face now, however, is political, and politicians are capable of inflicting great business damage. Importantly, unlike the trusts that were busted in the late 19th and early 20th centuries, our businesses are so much more popular with their stakeholders. Here is the question I keep asking myself: "Where are we? In the year 2000 when the dot.com bubble was about to burst and keeping lots of dry powder paid off; or, how about 1455 with the invention of movable type (enabling the printing of the Gutenberg Bible) and the explosion of mankind’s ability to communicate; or, 1820 and the commercialization of the steam engine?" My answer is that this is not a bubble. The period we are currently in represents as significant a leap forward in technology and productivity as the world has ever seen.

Importantly, Shad begins his monthly letter by noting:

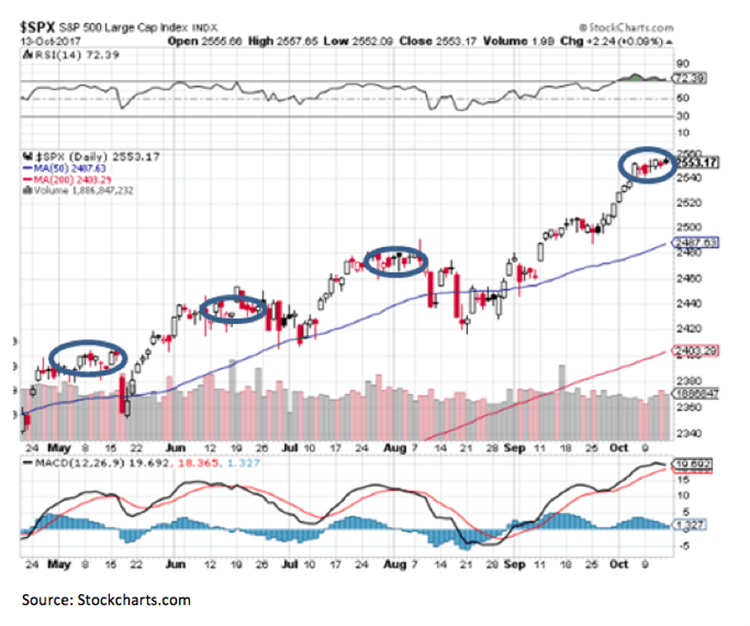

Our joyless bull market continues. Many investors I hear from are worried that another bear market is around the corner because on the surface the world has not changed much and it has been nine years since the last bear market. They argue that now is the time to get out of stocks or lighten up. While it might feel good to take money off the table and assume a regression to the mean based upon recent history, seeking comfort has never been the basis of a winning strategy in the stock market. Neither has being a market timer. Meanwhile stocks, in general, have continued to rise.

The stock market tends to be a predictor of future economic change, discounted back to the present. Our take is that there are great things taking place that are not readily apparent. Behind the political noise of the day, our companies are participating in one of the greatest growth and productivity surges the world has ever seen. Interestingly, this technological leap forward is taking place at the same time that increasing transparency (made possible by technology) is making it more fashionable to do the right thing. Even a small shift toward more ethical behavior opens up an even bigger opportunity for American companies operating throughout the world, further validating our “Americanization” theory. In short, we see plenty of reasons why the current bull market could be extended. All this does not imply that our current worldview is without risk. A number of our companies have transformed themselves from innovative upstarts into total global dominators. Consequently, they have huge targets on their backs courtesy of both sides of the political spectrum. This is a real threat. But is that a reason to get out? We do not think so.

As we have often said, “It’s a bull market you know,” which is the quip from Old Turkey in the must read book “Reminiscence of a Stock Operator” by Edwin Lefèvre. A bull market, indeed, which likely has years left to run, and very few people believe it. As Leon Tuey writes:

What I find interesting and most encouraging is that despite the market’s spectacular performance, there is not only no euphoria, but globally, investors remain skeptical and cautious. Clearly, ghosts of the last two bear markets continue to haunt investors from a sentiment standpoint, which is very bullish, as it tells me that this great bull market still has a long way to go in terms of time and distance. Many others factors continue to support this view. This bull market will die when the Fed sees fit to tighten meaningfully by draining liquidity from the system (which it has not); raising the discount rate many times in succession; and by inverting the Classic Yield Curve. As you know, these steps will only be taken when the economy overheats; inflation surges; and speculation is rampant.

Returning to Shad, the top 12 positions in his partnership represent approximately 95% of his equity exposure. Some of those names that are followed by Raymond James’ fundamental research analysts and screen well on our proprietary models include: Facebook (FB/$173.74/Strong Buy), Apple (AAPL/$156.99/Outperform), Alphabet (GOOG/$989.68/Outperform), Costco (COST/$159.85/Outperform), and PayPal (PYPL/$68.66/Outperform).