In response, with the recent run up to new highs, we are expecting a softening of upward momentum as the market digests incoming earnings. Spouts of volatility should be expected, but we continue to view weakness as a buying opportunity. Fundamental analysis will drive these tactical calls. As always, we continue to focus on protecting capital while mitigating risk across portfolios. Last Thursday I had the pleasure of spending a few hours with stock market veteran Jeff Saut, someone I hold in high regard and have got to know over the past number of years. Jeff once again eloquently reminded a roomful of some 250 investors, ‘The essence of portfolio management is the management of risks, not the management of returns. All good portfolio management begins and ends with this precept.’

. . . Craig White, portfolio manager, Huggan White

“Managing risk,” what a novel concept, but regrettably many investors fail to do just that. My father taught me to manage risk, a trait emphasized in the sentinel book by Benjamin Graham, The Intelligent Investor, which Warren Buffett has deemed, “The best book ever written on investing” and where the aforementioned quote resides. As my dad always reminded me, “If you manage the downside in a portfolio, and avoid the big loss, the upside will take care of itself.” However, managing risk is one of the hardest things to do, which is why you need a good financial advisor to help you manage the risk.

We are always attempting to manage risk and, most of the time, get it right. Sometimes, however, we too get blindsided. As Li Lu (a Chinese-born American investment banker, investor, and hedge fund manager) reminds us:

Investing is about predicting the future, and the future is inherently unpredictable. Therefore, the only way you can do better is to assess all the facts and truly know what you know and know what you don’t know. That’s your probability edge. Nothing is 100%, but if you always swing when you have an overwhelming better edge, then over time, you will do very well.

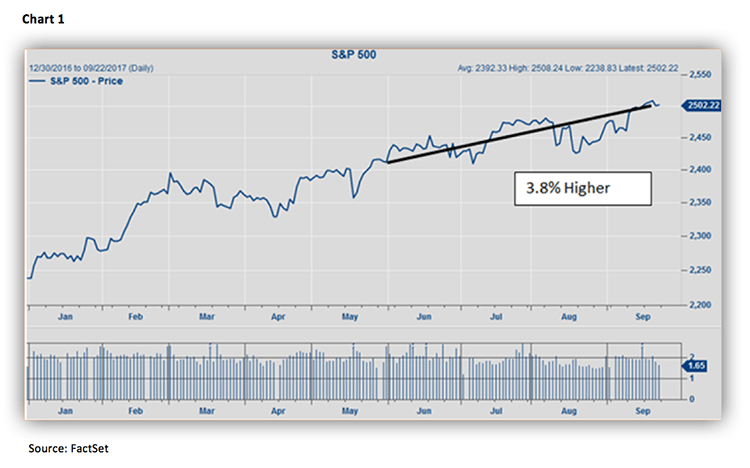

This is why, from time to time, we make “tactical calls” (short-term trading calls) when we do not feel all that comfortable with the near-term direction of the various markets. Most recently, that occurred at the beginning of August with the S&P 500 (SPX/2502.22) changing hands around 2490 as our short-term model registered a cautionary signal. At the time, we noted that and also suggested our internal energy model was out of energy, implying there should not be a whole lot of upside left for the equity markets. Sure enough, the SPX seems to have stalled with an intraday high “print” of some ~2508. Even our friend, and Canadian investing legend, Leon Tuey is looking for some kind of short-term pause within the construct of this secular bull market, for as he wrote last week:

Short-term, the major market indices and their internal measures are overbought. Moreover, short-term sentiment backdrop has deteriorated. Hence, a pause would not be surprising. After a minor pause, however, the rally will continue as the intermediate gauges are far from overbought. Moreover, momentum is re-accelerating. Long term, the primary trend remains powerfully bullish and the end is nowhere near in sight as the six major factors (monetary, economic, valuation, sentiment, supply/demand, and internal/momentum/technical) continue to give bullish readings. One of the most amazing aspects of this great bull market is sentiment. Although the bull market is in its ninth year and most stocks are up several hundred to several thousand percent, investors remain skeptical and pessimistic. Note that many hedge fund managers are bearish. Seth Klarman’s Blaupost holds 42% of its assets in cash. In terms of asset allocation, funds are sitting on a mountain of cash and very low in equities. In fact, funds are the most underweight in U.S. equities in ten years. Also worth noting is the shrinkage in the supply of stocks. In 1996, over 8000 stocks traded in the U.S. Today, that number has been halved. This supply/demand imbalance creates an explosive situation for the market. When the prevailing bearish sentiment recedes, that huge hoard of cash will find its way back to the equity market. I can hardly wait!

In conclusion, evidence continues to suggest that investors are witnessing the biggest bull market on record. The first leg of this great bull market commenced on October 10, 2008 and ended in May 2015. As always, it was driven by an easy/accommodative monetary policy. The second leg commenced in February 2016, which was driven by improving economic conditions caused by the monetary easing of the last 8.5 years. Hence, earnings momentum accelerates. Accordingly, it is always the longest and strongest [segment of a secular bull market]. Investors should emphasize industrials, technology, healthcare, and resource issues and other economy-sensitive areas.

One of the biggest mistakes investors make in a bull market is selling too soon. Accumulate favored areas when they are oversold and hold for the long-term. The time to liquidate is when the Fed starts to tighten meaningfully, i.e., when the Fed drains liquidity from the system; raises the discount rate many times in succession; and inverts the Classic Yield Curve (13-week T-bill Yield vs. the 20-year T-Bond Yield). Do not be distracted by the “noise” and the black headlines.