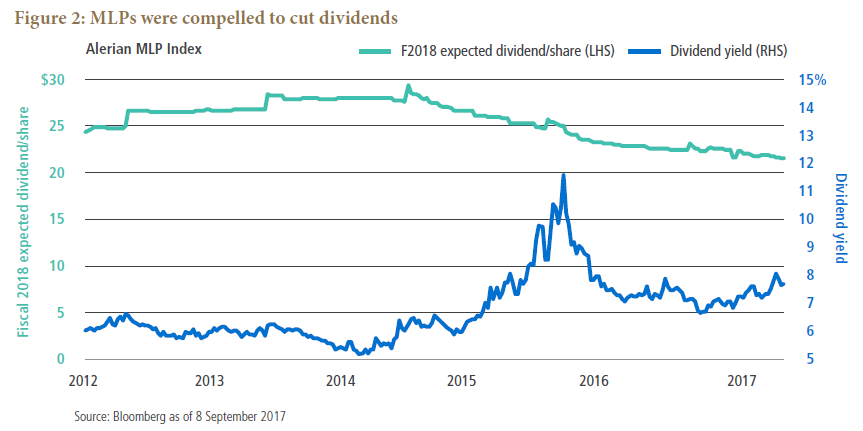

Unfavorable equity markets and stretched credit metrics left many MLPs with little choice but to trim their expected distributions, resulting in a 25% cut to 2018 dividend expectations over the past three years (see Figure 2). For investors seeking utility-like returns, the sustainability of dividends is sacrosanct, and many understandably abandoned the sector.

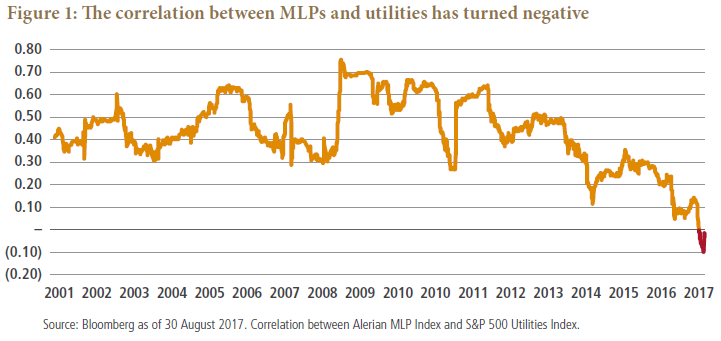

The result has been that since 2014, utilities have benefited from the global hunt for yield securities, while MLPs have not: The Alerian MLP Index has corrected 21%, while the S&P 500 Utilities Index has gained 64%. As MLPs traded off, the spread between MLPs and utilities – which averaged 2.0% after the financial crisis – has now widened to 4.25% currently.

MLPs are becoming more “utility-like” again

In other sectors, it’s typically a sign of distress when companies cut dividends or trade at elevated dividend yields. In our view this is not the case for MLPs, which have rather paused dividends to preserve capital. More importantly, we believe MLP management teams’ mindsets have changed: They now prioritize cash retention. This is a break from the traditional MLP model, which relied on consistent equity issuance to fund growth projects. By lowering dividends to preserve cash, MLPs are evolving into stronger franchises with better credit metrics, higher dividend coverage ratios and less reliance on capital markets – actions that should make MLPs more attractive to discerning investors.

Improved confidence that the current distributions are sustainable should also help bring back yield-hungry investors. After all, 8% dividend yields would be hard for investors to ignore today – especially when supported by 88% fee-based cash flows, improved balance sheets and attractive coverage ratios. And as fundamentals continue to strengthen, we expect the MLP sector to be less susceptible to daily oil price gyrations, which would further magnify the sector’s attractiveness relative to other yield asset classes.

We don’t deny that volatility related to oil prices may persist in the MLP asset class for some time. However, conditions have fundamentally improved compared with two years ago, suggesting investors will likely embrace a more “range bound” rather than “uncertain” crude price outlook. This could make it easier for new investors to dip their toes into the sector.

Some risks bear watching

Despite the recent improvements in the MLP sector, energy markets are cyclical and subject to unpredictable swings in both supply and demand. In a recession, global demand for energy can drop significantly, leading to lower prices and reduced transport volumes, which can hurt MLPs. Geopolitical risks are also an ongoing reality, given the outsize influence of OPEC and the Middle East on the energy markets.

Additionally, proposed pipeline projects in North America require approval from the Federal Energy Regulatory Commission (in the U.S.) or the National Energy Board (in Canada) to proceed. This process can take a year or more, and pipeline projects have faced increasing opposition given environmental concerns.

These risks bear watching even as MLP fundamentals continue to strengthen.

Key takeaways

Many investors understandably lost confidence in the MLP sector amid the changes over the past few years, but we believe patient investors willing to look past the recent volatility will likely have the opportunity to benefit.

In our view, with dividend cuts nearing an end, balance sheet repair gaining momentum and long-term prospects looking favorable, MLPs’ current valuations do not yet reflect the healing that is taking place and represent an overly negative outlook on the sector – and this creates potentially attractive investment opportunities for select MLPs. According to our analysis, MLPs as a group are trading at a material discount to historical valuations and offer potential for total returns in the low to mid-teens, supported by an 8% dividend yield. While there is no guarantee, this represents one of the most attractive secular growth stories in the market, in our view.

Value-oriented investors seeking higher-yielding opportunities may want to take a fresh look.

All investments contain risk and may lose value. Investing in MLPs involves risks that differ from equities, including limited control and limited rights to vote on matters affecting the partnership. MLPs are a partnership organized in the US and are subject to certain tax risks. Conflicts of interest may arise amongst common unit holders, subordinated unit holders and the general partner or managing member. MLPs may be affected by macro-economic and other factors affecting the stock market in general, expectations of interest rates, investor sentiment towards MLPs or the energy sector, changes in a particular issuer’s financial condition, or unfavorable or unanticipated poor performance of a particular issuer. MLP cash distributions are not guaranteed and depend on each partnership’s ability to generate adequate cash flow.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

The Alerian MLP Index is the leading gauge of large- and mid-cap energy master limited partnerships (MLPs). It is a float-adjusted, capitalization-weighted index, which includes 50 prominent companies. The S&P 500 Energy Index comprises those companies included in the S&P 500 that are classified as members of the GICS energy sector. The S&P 500 Utilities Index comprises those companies included in the S&P 500 that are classified as members of the GICS utilities sector. The S&P 500 Index is an unmanaged market index generally considered representative of the stock market as a whole. The index focuses on the Large-Cap segment of the U.S. equities market. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO