What are quantitative strategies?

Quantitative, or “quant,” strategies select securities based on prespecified sets of rules. These rules are based on quantifiable evidence, informed by a combination of proprietary analysis and academic research. Quant strategies are then executed based on where current prices are trading relative to the rules of the quantitative framework. For example, a simple quantitative value strategy may rely entirely on a quantifiable measure of value (e.g., price-to-book ratio), rather than on the manager’s forecast of the future price to instruct buy or sell decisions. In this way, quant strategies differ from discretionary strategies, which consistently rely on the skill of the investment manager to make investment decisions at every step of the way.

Are all quant strategies “black boxes”?

While it’s true that some quant managers consider specific details of their implementation strategy proprietary and are not willing to disclose their “secret sauce,” not all strategies rely on top-secret algorithms to make money. In fact, the majority of quant strategies are based on widely understood principles and well-researched pricing anomalies, such as momentum, value and carry, which are difficult to time and are best accessed through a rules-based approach. Managed futures strategies focus on momentum through a rules-based approach, rather than an opaque “black box.” Though managers typically don’t publish all details of their rules, they are generally relatively transparent regarding the substance of the models, making these strategies more like “glass boxes” than “black boxes.” Additionally, managed futures is often offered in liquid and relatively transparent structures.

What is managed futures?

A type of quant strategy, managed futures employs trend-following across asset classes. Trend-following is also referred to as “momentum” investing. Momentum investing contrasts with the more familiar “value” investing that seeks to buy low and sell high. In contrast, momentum investors seek positions in securities that have moved in one direction for a period of time – either up or down. They join the trend, taking long positions in assets that are going up in price, and short positions in assets whose prices are declining.

Momentum investors use quantitative signals to define when securities are trending. Often, these signals compare the current (spot) price of an asset to the trailing (historical) moving average of the price. If the spot price is above the moving averages, then the security is in an uptrend, and vice versa.

While most managed futures strategies focus on time series momentum, there are different types of momentum strategies:

- Time-series momentum strategies use trailing signals of past prices to construct portfolios of trending securities that can be directional based on the nature of the trend signals (e.g., short equities as equities trend lower);

- Cross-sectional momentum strategies look at a set of securities relative to each other and take long positions in those with relatively positive momentum and short positions in securities with relatively negative momentum. This type of strategy is most commonly executed on single stocks in equity markets.

Why does trend-following work?

A well-studied anomaly in academic literature, beginning with Jegadeesh and Titman, 1993,1 momentum is a recognized phenomenon across global asset classes. And in practice, it has worked remarkably well over long periods of time, generating positive returns with low correlations to stocks and bonds, and especially strong positive returns during equity bear markets. But if everyone knows about it, why does it work?

There are some interesting behavioral reasons that are thought to cause momentum to persist over time and across asset classes:

- New information takes time to be fully reflected in security prices, which leads to price trends as global investors adjust their positions.

- The over-reaction or “bandwagon” effect can push winners to trend higher and losers to trend lower for a period of time.

- There’s also the “disposition effect” in which investors tend to hold on to losers and sell winners. In other words, investors tend to gamble with losses to try to earn back their money, but tend to become risk-averse with winners to take profits while they can. Both effects can drive trends by increasing the time it takes for prices to reflect fundamental information.

- Investors tend to behave the same way in response to significant regime shifts, especially in risk-off markets. For example, when equity markets have large sell-offs, many investors tend to reduce risk across their portfolios, which can lead to trending prices across global asset classes.

What’s in the managed futures “box”?

While all managed futures strategies focus on quantitative trend-following, not all trend-following strategies are designed the same. Managed futures strategies commonly vary along the following dimensions:

- The universe of securities: How many securities does the manager access and what is the tradeoff between diversification and liquidity?

- Asset classes often included in managed futures strategies are equities, fixed income, currencies, and commodities.

- Defining trend signals: How long are the “look back windows” used to determine whether a security is trending?

- Shorter windows lead to higher turnover and potentially stronger performance in risk-off markets since they adapt to new trends quickly;

- Longer windows lead to lower frequency strategies with lower turnover.

The choices that managers make for which securities to include and which trend signals to follow can cause performance to vary quite a bit among managed futures managers. It’s important that investors understand each manager’s relative advantage when investing in trend-following strategies to make sure that a particular managed futures strategy will align with their investment objectives.

Why do investors allocate to managed futures?

Managed futures strategies have a unique profile relative to other potential investments, including:

- Long-term positive historical returns of a similar magnitude to equities;

- Very low correlations to equities and other global asset classes;

- Strong historical performance during equity bear markets.

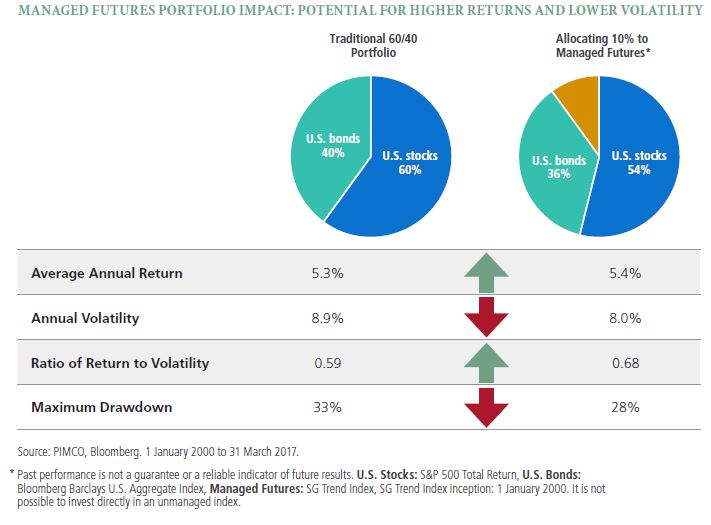

As a result, an allocation to managed futures can have a powerful impact on broader portfolios by potentially increasing returns, reducing risk and mitigating drawdowns.

That said, it is important to keep in mind that managed futures strategies are relatively volatile. While this volatility is likely to reduce risk in a broader portfolio context, it can be significant on a standalone basis. Most managers target levels of volatility between 10–20%, with some variation in those targets over shorter periods.

Another important consideration is that managed futures strategies may not provide a buffer against sudden, short-lived market moves or “flash crashes.” Although these strategies have the potential to be highly diversifying and tend to perform best over periods of prolonged market sell-offs, they cannot be relied on to hedge against sudden market moves. Essentially, if the strategy doesn’t have enough time to identify the trend, then it may not be positioned to profit from it, and may in fact have losses if a sharp move is in the opposite direction of previous trends.

For most investors, a 5–15% allocation to managed futures may offer a good balance of diversification and volatility. Over the long term, the volatility of most managed futures strategies will be closer to that of equities than that of core bonds, and this size of allocation generally may be enough to “move the needle” positively in most portfolio allocations.

1 “Returns To Buying Winners and Selling Losers: Implications for Stock Market Efficiency,” Narasimhan Jegadeesh and Sheridan Titman, The Journal of Finance, March 1993.

© PIMCO

www.pimco.com

© PIMCO

Read more commentaries by PIMCO