Additional bottom-up insights into trading and security selection flow from traders, analysts and portfolio managers across the full range of fixed income securities, including Treasuries, agencies, mortgages and emerging markets. All told, PIMCO has more than 100 global credit investment professionals in nine offices around the world.

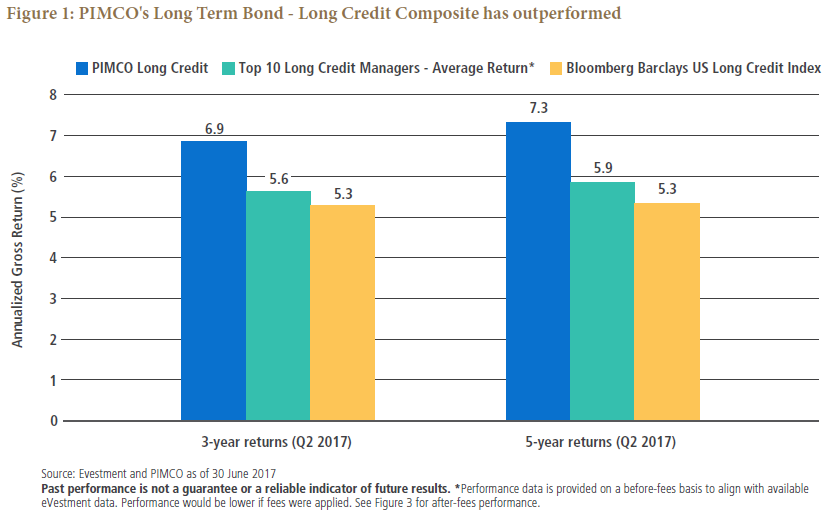

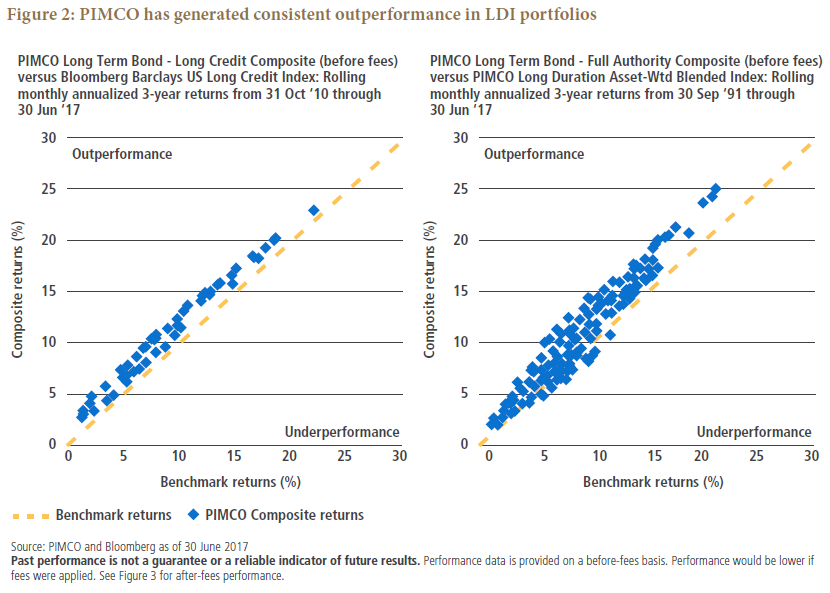

When it comes to LDI, our portfolio construction approach considers the unique nature of long duration portfolios. We analyze key rate-duration buckets, idiosyncratic credit risks related to longer maturities, and the dynamic nature of LDI benchmarks. For example, portfolio liquidity and positioning reflect the fact that certain LDI portfolio benchmarks are adjusted frequently to maintain their fit with liabilities. In addition, the credit research and issue-selection process takes account of the significant difference in average maturities of securities in LDI portfolios relative to broader bond mandates. As such, our tolerance for downgrade events and spread-widening may, at times, be lower in long duration portfolios. Finally, given the domestic focus of LDI strategies - driven by domestic discount rate methodologies - we tend to use non-U.S. exposures and currency management to a lesser extent than in other lines of business. These processes have helped us to achieve the same excess return generation consistency in long duration portfolios as PIMCO seeks across a wide range of strategies and mandates (see Figure 2).

Q: Long-term bonds represent a small subset of the fixed income universe. What challenges does this present to alpha generation?

A: In the U.S., the long duration universe, as defined by investment grade securities (both government and credit bonds) with maturities longer than 10 years, represents approximately 15% of the broad investment grade bond market. This presents some challenges: For example, at times liquidity may be lower than most market sectors, requiring investors to work harder and smarter to achieve proper issuer and sector diversification. Transaction costs also are likely to be higher. In addition, we always keep in mind that in long credit markets we are lending clients' money for fairly long periods of time.

These factors - liquidity, transaction costs and long lending periods - magnify the potential negative impact of a mistake in credit assessment or a misjudgment in the evolution of a credit rating. They explain why thorough credit research is especially important

in LDI.

Importantly, however, these challenges represent alpha opportunities for skilled managers. Having sizeable and skilled credit research resources, we believe we can harness the premiums that potentially exist because of the challenges noted above. In that regard, we view our size as a significant advantage: It allows us to maintain a sizable amount of analyst, portfolio management and technological resources to quickly respond to market opportunities. It also helps facilitate partnerships with companies we view favorably, creating opportunities for long-term financing. Our market footprint can also help us influence debt covenants to the potential benefit of clients. Given all this, we think our ability to add alpha in LDI portfolios is very similar to the potential for adding alpha in traditional total return fixed

income portfolios.

In addition to alpha potential, we have developed innovative investment structures that seek to help our clients overcome challenges in long credit and long duration markets. Our long credit sector fund is a good example. This vehicle, used exclusively within our institutional separate accounts, pools long credit purchases of numerous investors into a private, commingled vehicle that creates opportunities and advantages, including the potential to:

- Get almost immediate exposure to the long credit market – rather than the several weeks often required to put cash to work in that segment of the market

- Achieve a high degree of diversification as investors access a portfolio that has incorporated new issues over several years

(rather than just a few weeks of new-issue exposure)

- Reduce transaction costs thanks to heightened liquidity and the size of the commingled vehicle in relation to the size of any of its underlying investors

- Improve the liquidity profile of a long credit allocation, as any liquidity requirement (be it for benefit payments, rebalancing or other reasons) is generally quite small in relation to the size of the pooled vehicle

Q: Let's talk about current market conditions. Corporate spreads are relatively tight and the Federal Reserve is gradually normalizing rates. Is this environment still conducive to achieving excess returns in line with PIMCO's recent historical experience?

A: Actually, we believe today's environment has the potential to create even greater opportunities than those of the past several years. In recent years, central bank intervention has helped to suppress volatility in markets (although various subsectors have continued to see bouts of volatility, such as energy in Q1 2016/Q2 2017, autos in Q1 2017 and retail in Q2 2017).

As a general rule, increased volatility should lead to increased alpha-generating potential (within reason). Our base case is that the Fed begins to shrink its balance sheet after the September meeting. If so, we see scope for volatility to increase, creating even more potential to add value in LDI portfolios.

Our approach to credit investing seeks to identify companies and sectors that will outperform – or underperform – the broad market. Historically, security and sector selection has contributed about two-thirds of our alpha in credit strategies. Even though the aggregate level of credit spreads has tightened, we believe many sector-specific changes will be important drivers of excess return potential over the next 2-3 years.

Consider, for example, that old media is being replaced by new media, Amazon is disintermediating brick-and-mortar retail stores, technology is revolutionizing energy and autos, and merger-and-acquisition cycles are shaking up numerous other sectors. Similarly, individual companies with strong assets and hard-to-penetrate markets may be well-insulated from future growth slowdowns. With our extensive resources and decades of experience as one of the world's largest investors in the global credit markets, PIMCO remains well-positioned to take advantage of differentiated performance within credit markets.

In our view, the potential for rising interest rates and tighter credit markets heightens the need for active management. In recent years, falling interest rates and tightening credit spreads have boosted returns for passive and lower-active-risk LDI approaches. But with interest rates potentially on the rise and credit markets fairly valued, we are unlikely to witness another tide that lifts all boats. With beta, or benchmark, returns likely to be lower, excess returns take on added significance.

In summary, we believe that today's environment continues to offer strong alpha opportunities. However, alpha is unlikely to stem from higher-beta risk as much as a thorough understanding of changing macro conditions and robust bottom-up credit research.

Nonetheless, investors must recognize that markets are going to be more challenging to navigate than those of the last seven or eight years. Thus, we believe investors should seek to partner with investment managers with a deep bench of resources and experience in managing LDI portfolios through challenging environments (e.g., expertise in managing LDI portfolios in rising rate environments or knowhow in managing credit during spread-widening cycles).

Q: PIMCO is a large player in U.S. long corporate bonds and many other markets. Is this an impediment to adding value in those portfolios?

A: Not at all. In fact, we view our size as a unique advantage. The scale of our business allows us to have large teams of credit analysts and portfolios managers. This is increasingly important: In the last five years, for instance, the number of companies in the Bloomberg Barclays U.S. Long Credit benchmark has grown by about 25%, from 340 to 430 firms. Understanding how companies and sectors will evolve requires human and technological resources.

Indeed, we believe our scale engenders many advantages:

- It helps us navigate changing liquidity conditions. With banks facing tighter post-crisis regulation, they have reduced their market-making function in credit markets. On several occasions, PIMCO has stepped up to become a liquidity provider.

- It can allow us to partner with companies to provide financing through reverse inquiries. In June, The Wall Street Journal highlighted how scale may create value in fixed income investing (see "In the New Bond Market, Bigger Is Better").

- It gives us the resources to develop custom solutions and track risk against bespoke benchmarks and compliance regulations. LDI management requires customized glide paths and benchmarks with unique compliance regulations. Our size also enables us to have a deep bench of resources in pension solutions, compliance and risk management to develop customized solutions for clients and track risk against their liabilities.

- Finally, it helps us capitalize on the growth of passive investing, which has created a unique potential to add further alpha for our clients. Passive strategies buy and sell securities as benchmarks change (for instance, when securities get upgraded or downgraded). This often results in inefficiencies that can create opportunities for large asset managers like PIMCO. We recently explored this issue in "Bonds Are Different: Active Versus Passive Management in 12 Points."

Q: Risk management is also a critical aspect of actively managed LDI portfolios. Could you discuss PIMCO’s risk management approach and how it applies to LDI portfolios?

A: In LDI space, risk is often defined as the potential for (significant) divergence between the performance of assets and liabilities as market conditions fluctuate. As such, the first step in our risk management process is to develop a robust understanding and measurement of a client’s liability risk profile. We use several proprietary tools to measure and quantify liability risk exposure.

Next, we design portfolio guidelines, objectives and benchmarks based on that liability risk exposure as well as our clients’ willingness and tolerance for risk.

From there, we position the actively managed portfolio around liability targets or benchmarks with the objective of exceeding that benchmark return by an amount that is commensurate with the investor’s risk tolerance.

We apply a robust risk management process that helps us scale deviations around the benchmark to an appropriate level in order to stay within the client’s risk tolerance objectives. To carry this out, PIMCO uses a wide range of proprietary analytics tools. We have always believed that to make independent decisions, it's essential to control the means for analyzing potential investments. As a result, we have devoted significant resources to building a library of in-house analytical software that helps to identify and quantify the risks inherent in different portfolio structures and strategies, specific bond market sectors, and securities within those sectors. Over the years, this effort has grown considerably.

Although third parties provide similar tools, we seek to add value with our proprietary models. In-house development by portfolio managers and financial engineers enhances the quality of our models and increases portfolio managers' understanding of the results, since all analytical tools depend on input assumptions. Moreover, because we developed our systems in-house, we are well-positioned to quickly create new tools or enhance existing ones in response to product or market changes.

We recognize, of course, that the coming three to five years will likely present unique challenges. Potential risks include rising geopolitical tensions, the consequences of debt creation over the last five years and the likely reduction of monetary policy support. That said, with our 250-plus portfolio management team, external advisors and client service teams, PIMCO remains committed to seeking consistent alpha for the benefit of its clients.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. The “gross of fees” performance figures above are presented before management fees (for Pacific Investment Management Company LLC described in Part 2 of its Form ADV) and custodial fees (in the case of both separate accounts and mutual funds), but do reflect commissions, other expenses and reinvestment of earnings. The “net of fees" performance figures reflect the deduction of actual investment advisory fees but do not reflect the deduction of custodial fees. All periods longer than one year are annualized. Separate account clients may elect to include PIMCO sector funds in their portfolio; sector funds may be subject to additional terms and fees.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Management risk is the risk that the investment techniques and risk analyses applied by PIMCO will not produce the desired results, and that certain policies or developments may affect the investment techniques available to PIMCO in connection with managing the strategy. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

The Bloomberg Barclays U.S. Long Credit Index includes both corporate and non-corporate sectors with maturities equal to or greater than 10 years. The corporate sectors are Industrial, Utility, and Finance, which include both U.S. and non-U.S. corporations. The non-corporate sectors are Sovereign, Supernatural, Foreign Agency, and Foreign Local Government. Benchmark returns were not examined and are not covered by the report of independent accountants. The PIMCO Long Duration Asset-Weighted Index is a blended benchmark, rebalanced monthly, combining the individual account benchmarks at the same weights as the account weights in the composite. As of December 2016, the benchmark consisted of 28.3% Bloomberg Barclays U.S. Long Credit Index; 26.9% Bloomberg Barclays Long Government/Credit Index; 14.3% a blend of 75% Bloomberg Barclays U.S. Long Credit Index and 25% Bloomberg Barclays U.S. Long Government Index; 6.9% Bloomberg Barclays U.S. Long Corporate Index; 2.1% a blend of 75% Bloomberg Barclays U.S. Long Corporate Index and 25% Bloomberg Barclays U.S. Long Government Index; with the remainder comprised of various other long duration indices, each representing less than 2% of the total blend. The breakdown of the custom benchmark for different time periods is available upon request. Benchmark returns were not examined and are not covered by the report of independent accountants. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO