The development of a personal trading or investing philosophy is usually an evolutionary and highly personal process. Through a combination of experience, trial-and-error, and the attainment of knowledge, successful market participants hone their skills until they find a strategy that works for them and that is consistent with their general mindset. Despite the individualized journey, though, battle lines are generally formed between those who practice more value-based fundamental analysis and those who practice price-based technical analysis. Both disciplines can obviously be used together, but most people in this business probably do lean either more one way or the other, hence the friendly friction between the two schools of thought.

To greatly oversimply things, the “fundamentalists” are commonly followers of Benjamin Graham and David Dodd, the noted Columbia Business School professors who wrote the seminal book Security Analysis back in 1934. Their work treated stocks as the businesses they represented, and they endeavored to uncover situations where the price of shares in a company diverged from the true intrinsic value of its business. “Technicians,” on the other hand, study Technical Analysis of Stock Trends written by Robert D. Edwards and John Magee in 1948 and believe that stocks are just pieces of paper and the prices paid for them at any given time are the true “values” of the companies. Technical analysts argue that the fundamentals don’t make you any money unless the market agrees with your assessment of those fundamentals, and even if one’s fundamental opinion is correct and the price moves to the intrinsic value, it will be reflected in the charts anyway so the technically inclined can take advantage of the move as well. Fundamentalists, of course, retort that the true value of a company can be known in advance of a price move, which potentially allows for getting in or out before the chartists start picking up on any changes in trend. It’s also tough to argue against a strategy that turned Graham & Dodd disciple, Warren Buffett, into the world’s wealthiest person!

Doug Kass of Seabreeze Partners touched on a similar discussion in a comment last Friday that pondered whether investors and traders should be reactionary (more technical) or anticipatory (more fundamental). His conclusion was: “It can be debated which is the proper strategy…[but] I believe they can coexist.” We very much agree and think the two disciplines should coexist and be used together to form an investment opinion. We tend to be more reactionary on a longer-term basis but anticipatory on a shorter-term basis, and the combination has mostly worked well for us.

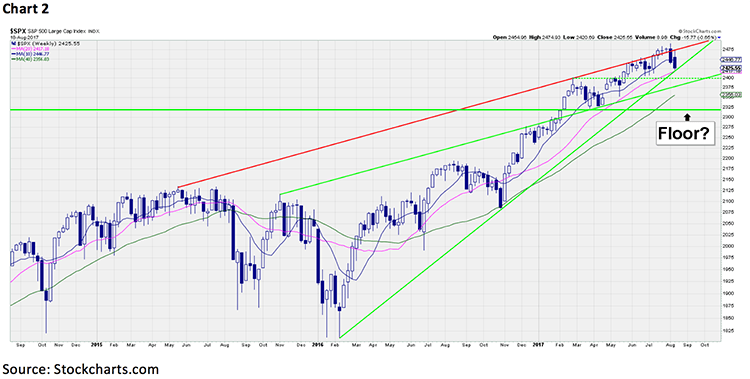

However, the Edwards & Magee crowd have most certainly won out over the last year, as the stock market has largely traded higher despite consistent calls from the Graham & Dodd contingent that the aggregate value of companies does not justify the current price level. The charts support the view that the long-term uptrend remains intact and the recent weakness is little more than a harmless pullback at this point. The Graham & Dodd believers, conversely, have intensified their warnings over the last two weeks, as they argue this down-move is only the beginning of a larger market adjustment.

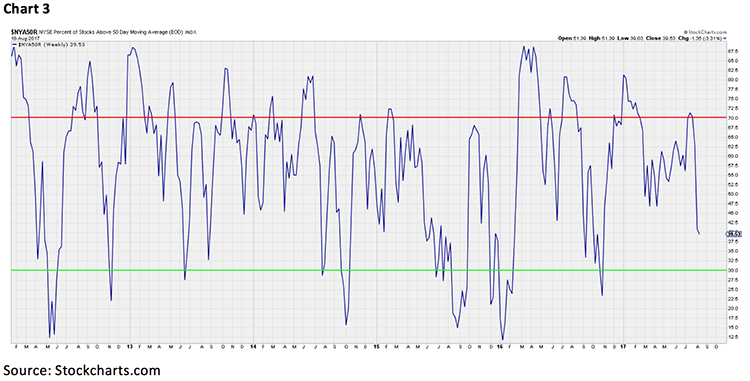

Unfortunately, there exists no 100% accurate method; we, therefore, try to separate out and weigh as many factors as we can to see which direction the odds favor over various time horizons. At this stage, it is important to realize that all we’ve been dealt so far is a 2.82% dip on an intraday basis, so we think it’s much too early to mourn the death of the secular bull market. Remember, other than an overheated market pausing to cool off, little has changed from just a couple weeks ago. Specific events are always given credit for causing market moves, but it is funny how these events seem to come out of “nowhere” just as the technicals are indicating a change is likely due. Looking beyond the headlines, though, there really has not been a noticeable change in the overall conditions that have driven stocks to higher prices since the February 2016 lows: the U.S. economy is still reflecting okay, but not great growth; earnings season was strong even if the results were largely already priced in; and really no part of our overall secular bull market thesis has been interrupted by the action over the last two weeks. Instead, a convergence of negative news items have arrived at a time when there are few earnings releases or other positive fundamental news to help counter the bad sentiment and during a pre-Labor Day period when volumes tend to dry up anyway.