Emerging Market Local Debt: Growing Depth, Growing Opportunity

The landscape for emerging market (EM) local debt is expanding fast – and looks set to continue.

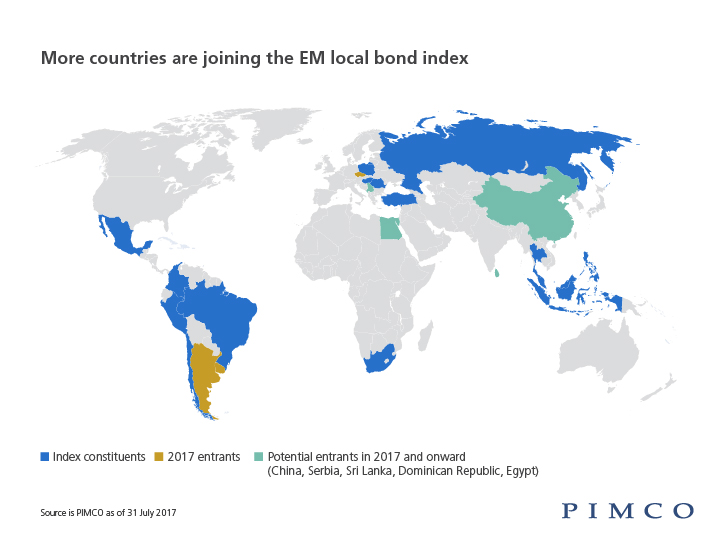

Earlier this year, Argentina, the Czech Republic and Uruguay joined the bellwether benchmark for the asset class, JPMorgan GBI-EM Global Diversified, taking the total to 18 countries. China, Egypt and another three countries may enter the index next year. The inclusions will make the EM local debt asset class much larger, deeper and more liquid. (For more on China, see "China and Emerging Asia: A New Dawn for the Capital Markets.")

Active investors may benefit in two big ways. First, the asset class will become more complex and diversified. This will allow investors to invest in more countries to seek alpha and greater relative-value opportunities. Importantly, the broadening of the index unanchors performance from a small number of index heavyweights. The number of countries whose index weights were capped at 10%, for example, has fallen from six three years ago to two.

Second, index inclusion (or exclusion) will create changing supply and demand forces that, if understood well, could become a significant source of alpha potential in portfolios. Seeking first-mover advantage may require grinding back-office work and taking nonconsensus positions, but the rewards can be handsome.

Offshore investors have shown growing interest in EM local debt, which generally features high nominal and real yields, and undervalued currencies. Peru's launch of $3 billion in local currency bonds in July, for instance, was met with more than $10 billion in demand, according to reports.