At the height of the technology bubble, the median of the most reliable market valuation measures we follow (those most strongly correlated with actual subsequent S&P 500 total returns) briefly reached an apex 178% above historical norms that had been regularly approached or breached over the completion of every market cycle in history. That level of valuation implied a prospective market loss of (1/(1+1.78)-1 = ) -64% as the bubble collapsed. In real-time, I suggested, based on related measures, that prospective market losses would likely be tiered, with tech stocks losing about -83%, the S&P 500 losing more than half of its value. As it happened, the 2000-2002 collapse took the S&P 500 down by 50%, while the tech-heavy Nasdaq 100 Index lost an oddly precise -83%. Smaller capitalization stocks suffered less extensive losses due to better valuations, as they had materially lagged the large-cap indices during the late-stages of that bubble.

Attempting to “stimulate” the economy from the recession that followed, the Federal Reserve cut short-term interest rates to just 1%, provoking an episode of yield-seeking speculation, where yield-starved investors created demand for higher-yielding mortgage-backed securities, and a weakly-regulated Wall Street rushed to create new “product” to meet the demand (by lending to anyone with a pulse). At its peak, the resulting bubble took the median of the most reliable market valuation measures we follow to a level more than 95% above their historical norms, implying a prospective market loss on the order of -49% as that bubble collapsed.

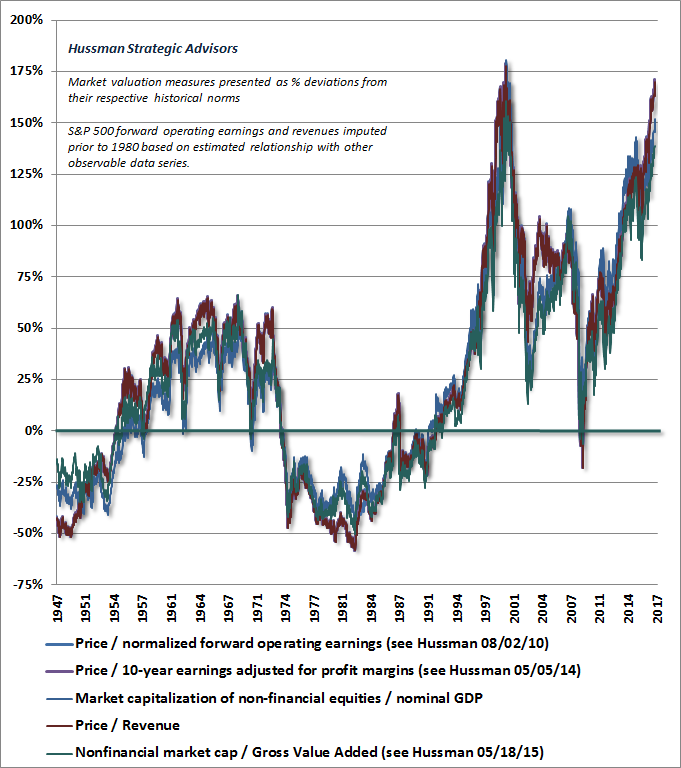

While I've written about numerous valuation measures over time, the most reliable ones share a common feature: they focus on identifying "sufficient statistics" for the very, very long-term stream of cash flows that stocks can be expected to deliver into the hands of investors over time. On that front, revenues are typically more robust "sufficient statistics" than current or year-ahead earnings. See Exhaustion Gaps and the Fear of Missing Out for a table showing the relative reliability of a variety of measures. In April 2007, I estimated that an appropriate valuation for the S&P 500 stood about 850, roughly -40% lower than prevailing levels. By the October peak, the prospective market loss to normal valuation had increased to about -46%. As it happened, the subsequent collapse of the housing bubble took the S&P 500 about -55% lower. In late-October 1998, as the market plunge crossed below historically reliable valuation norms, I observed that the S&P 500 had become undervalued on our measures.

Again attempting to “stimulate” the economy from the recession that followed, the Federal Reserve cut short-term interest rates to zero in recent years, provoking yet another episode of yield-seeking speculation, where yield-starved investors created demand for virtually every class of securities, in the hope of achieving returns in excess of zero. Meanwhile, Wall Street, suffering from what J.K. Galbraith once called the “extreme brevity of the financial memory,” convinced itself yet again that the whole episode was built on something more solid than quotes on a screen and blotches of ink on paper. At last week’s highs, the median of the most reliable market valuation measures we follow reached an extreme that placed them 170% above their historical norms, implying a prospective market loss on the order of -63% in what I fully expect to be the collapse of the third speculative bubble since 2000. Notably, there is only a single week in history where the median valuation on our most reliable measures exceeded the level we just observed. That was the week of March 24, 2000, which set the peak of the tech bubble. Unlike the 2000-2002 retreat however, the damage to paper values over the completion of the current cycle is likely to spare few sectors, as the median valuation across individual stocks is at a record high, and far beyond the 2000 peak.

The chart below presents some of these valuation measures. Note that even if the completion of this cycle leaves these measures 25% above their historical norms, the resulting market decline would amount to about (1.25/2.70-1 =) -54%, while a decline that leaves valuations still 50% above their norms would still represent a market loss in excess of -44%. Aside from shorter-term bursts of speculative enthusiasm, even low interest rates are not likely to mitigate full-cycle market losses, because over time, the benefits of low rates are typically offset by the disappointing economic growth that produces them (see Rarified Air: Valuations and Subsequent Market Returns for a deep dive into these relationships). It’s important to be very clear on this point: a market loss between -44% and -63% over the completion of this cycle would not represent a worst-case scenario, but instead an ordinary, pedestrian, historically run-of-the-mill outcome given current valuation extremes.

While valuation measures are extremely informative about the prospects for market total returns on a 10-12 year horizon, as well as prospective market losses over the completion of any given market cycle, valuations are rather weak indicators of near-term market returns. Outcomes over shorter segments of the market cycle are much more dependent on the psychological inclination of investors toward speculation or risk-aversion, which we infer from the uniformity or divergence of market internals across a broad range of securities and markets (when investors are inclined toward speculation, they tend to be indiscriminate about it).

The central lesson of the recent advancing half-cycle, for us, was that in the presence of zero interest rates, even extreme “overvalued, overbought, overbullish” syndromes that had reliably warned of steep market losses in prior cycles were not enough; one had to wait for explicit deterioration in market internals before responding to hypervaluation with a hard-negative outlook. That will indeed be something to remember if the condition of market internals improves, and particularly if that occurs in the face of fresh zero-interest rate policy. But here and now, all of these measures present a hostile outlook. Dismissing present risks on the basis of my own stumble in the advancing half of this cycle is unlikely to be rewarding in the market wipeout that a century of history suggests will complete this cycle.

By the completion of the current cycle, investors will likely relearn how erroneous and irrelevant it was to worry about “selling too early” in an extremely overvalued market. It’s worth remembering now that by the end of the 2000-2002 decline, the entire total return of the S&P 500, in excess of Treasury bills, had been wiped out all the way back to May 1996. By the end of the 2007-2009 collapse, the entire total return of the S&P 500, in excess of Treasury bills, had been wiped out all the way back to June 1995. Likewise, my expectation is that the completion of the current market cycle will wipe out the total returns of the S&P 500, in excess of Treasury bill returns, all the way back to roughly October 1997 (from the standpoint of of the recent bull market advance, that would also erase the entire total return of the S&P 500, in excess of Treasury bill returns, since late-2009). This outcome would not even require the most reliable valuation measures to breach historical norms that they have revisited in virtually every market cycle, even those associated with very low interest rates. See Durable Returns, Transient Returns for a reminder of how all of this works.

Having correctly anticipated and watched major collapses unfold in prior market cycles, my sense is that many investors are likely thinking “I can always get out if the news gets bad and a steep loss starts to unfold.” More likely, what will actually happen is that the first market loss off the top will be a nearly vertical drop on the order of 12-14% and will be associated with virtually no meaningful news at all, and most investors will consider the decline far too steep to make selling worthwhile. A subsequent advance from that low, whether it recovers a third, or a half, or nearly all of the loss, will reinforce that mentality. Except for outright crashes like 1987, steep market losses are regularly punctuated by fast, furious advances that restore hope, and then give way to a fresh cascade of losses. If possible, get some charts and go through a few past market collapses day-by-day (blocking out the right side so it’s not clear what happened next), and you’ll get a feel for this constant flux between fear and relief, all the way down.

Hot Potatoes and Dutch Tulips

In the meantime, a few observations regarding quantitative easing may be useful. Recall that the Federal Reserve implements quantitative easing by buying existing government securities and creating base money (bank reserves and currency) to pay for them. Once the base money is created, it remains in the form of base money until it is retired. It can never “turn into” something else, nor does it “go into” any other market in the hands of a buyer without immediately coming right back out in the hands of a seller. So while base money can go everywhere as part of various transactions, it ultimately goes nowhere in the sense that it remains base money at every moment in time. The only way to eliminate the base money is to retire it. To do so, the Federal Reserve plans to let the bonds in its portfolio mature without reinvesting the proceeds, beginning later this year.

Understanding this, it’s easy to answer the question “where will the money come from to buy Treasury bonds if the Fed doesn’t reinvest?” Regardless of how many transactions take place, at the end of the day, there will be less base money held by the public, and there will be more Treasuries held by the public. In equilibrium, it must be true that the Treasuries not bought by the Fed must be purchased, in aggregate, by investors who would otherwise have held base money. So instead of holding short-term, liquid base money at 1%, they’ll hold longer-term Treasury bonds at a somewhat higher yield. As a side note, bank reserves earn 1% here because the Fed explicitly pays interest on them in order to execute monetary policy - see How to Wind Down a $4 Trillion Balance Sheet for details.

Presently, 1% short-term interest rates and current Treasury bond yields are sufficient to induce investors to hold the outstanding quantity of both. It’s not entirely clear that investors will be willing to swap one for the other in vastly larger dollar amounts without some additional inducement to do so, but there’s no obvious reason to think investors will be massively averse to swapping 1% short-term base money for higher-yielding longer-term Treasury bonds

Presently, the Federal Reserve holds about $4.5 trillion in assets, comprised mostly of Treasury debt ($2.5 trillion) and mortgage-backed securities (about $1.8 trillion). To pay for those assets, it has created liabilities in the form of currency in circulation (about $1.6 trillion), bank reserves (about $2.3 trillion) and other liabilities (about $0.6 trillion), the main additional form being “reverse repurchase agreements” (see my December 15, 2015 commentfor an explanation of reverse repos).

The key fact is that once base money is created, that base money continues to exist, precisely in the form of base money, until it is retired. Assertions that Fed-created liquidity went “into” stocks, or bonds, or junk debt, or real-estate or anything else are incomplete, because any time base money goes “into” a transaction in the hands of a buyer, it immediately comes “out of” that same transaction in the hands of a seller, and the base money is unchanged by the operation. So even if base money changes hands a million times a minute, at every moment in time, somebody still holds that base money, in the form of base money. If Joe Schmoe writes a check to his brokerage account to buy stocks, and Holden McCash sells stocks to Joe, then Joe ends up with Holden’s stocks, and Holden ends up with Joe’s base money.

If we take a snapshot of the banking system, even if there are lots of transactions and loans taking place throughout the economy, the fact is that of the $2.3 trillion in bank reserves right now, over $2 trillion of those are “excess” reserves. Sure, if one bank lends some of these excess reserves to Jane, and Jane uses them to buy something from Ed, they’ll still show up as excess reserves in Ed’s bank, and if Ed then uses them to buy something from Jimmy, they’ll end up in Jimmy’s bank, nearly entirely as excess reserves. Yet all of this could still happen with a vastly smaller pool of excess reserves. Indeed, the entire banking system could function just as well with a just fraction of present reserve levels.

But see, greater real economic activity was never the likely outcome of all this quantitative easing (indeed, one can show that the path of the economy since the crisis has not been materially different than what one could have projected using wholly non-monetary variables). Rather, Ben Bernanke, in his self-appointed role as Mad Hatter, was convinced that offensively hypervalued financial markets - that encourage the speculative misallocation of capital, imply dismal expected future returns, and create temporary paper profits that ultimately collapse - somehow represent a greater and more desirable form of “wealth”compared with reasonably-valued financial markets that offer attractive expected returns and help to soundly allocate capital. Believing that wealth is embodied by the price of a security rather than its future stream of cash flows, QE has created a world of hypervaluation, zero prospective future returns, and massive downside risks across nearly every conventional asset class.

And so, the Fed created such an enormous pool of zero interest bank reserves that investors would feel pressure to chase stocks, junk debt, anything to get rid of these yield-free hot potatoes. That didn’t stimulate more lending; it just created more investors who were frustrated with zero returns, because someone had to hold that base money, and in aggregate, all of them had to hold over $4 trillion of the stuff at every moment in time.

When you look objectively at what the Fed actually did, should be obvious how its actions encouraged this bubble. Every time someone would get rid of zero-interest base money by buying a riskier security, the seller would get the base money, and the cycle would continue until every asset was priced to deliver future returns near zero. We’re now at the point where junk yields are among the lowest in history, stock market valuations are so extreme that we estimate zero or negative S&P 500 average annual nominal total returns over the coming 10-12 year horizon, and our estimate of 12-year prospective total returns on a conventional mix of 60% stocks, 30% Treasury bonds, and 10% Treasury bills has never been lower (about 1% annually here). This whole episode is likely to end so badly that future children will learn about it in school and shake their heads in wonder at the rank stupidity of it all, just like many of us did when we learned about the Dutch Tulip mania.

Examine all risk exposures, consider your investment horizon and risk-tolerance carefully, commit to the flexibility toward greater market exposure at points where a material retreat in valuations is joined by early improvement in market action (even if the news happens to be very negative at that point), fasten your protective gear, and expect a little bit of whiplash. Remember that the “catalysts” often become evident after prices move, not before. The completion of this market cycle may or may not be immediate, but with the median stock at easily the most extreme price/revenue ratio in history, and a run-of-the-mill outcome now being market loss on the order of -60%, the contrast between recent stability and likely future volatility could hardly be more striking.

© Hussman Funds

© Hussman Funds

Read more commentaries by Hussman Funds