SUMMARY

- Investors in municipal bond funds tend to be seeking high quality, tax-efficient income with limited price volatility, but several characteristics of rules-based passive strategies may run counter to these objectives.

- Passive portfolios often don’t prioritize tax efficiency, and the highly fragmented muni market makes index replication costly and inefficient. Index-based approaches may also expose passive investors to outsize credit risk and may be pressured into to buying high and selling low.

- We believe active strategies may better equip investors to meet their objectives, withstand market volatility and ultimately generate better risk-adjusted, after-tax returns.

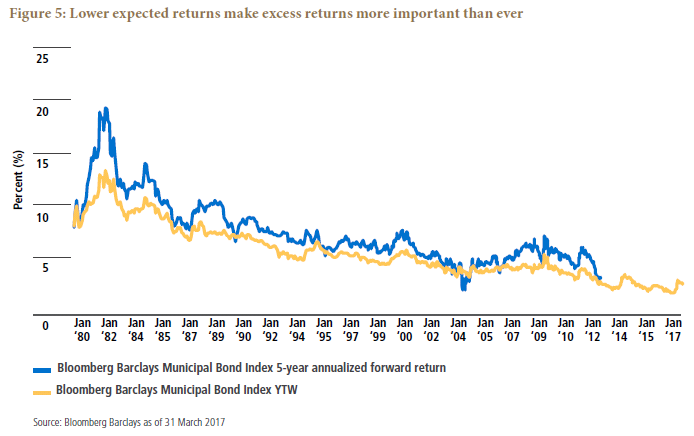

History has shown that when it comes to the cost/benefit tradeoff between active and passive management, bonds are different from equities – and this distinction may be especially striking for municipal bond strategies. On the surface, the argument that a lower-fee passive solution can support higher after-fee returns may seem reasonable and even compelling, particularly in an investment environment where returns are expected to be lower than in the past. But our years of managing investments in the complex, fragmented municipal bond market – with its often idiosyncratic risks and opportunities – have shown that an active approach may benefit investors in several important ways.

The first question investors must ask when considering their approach to investing in municipal bond funds is what they’re hoping to gain from this exposure, and for most, the answer is high quality, tax-efficient income with limited price volatility. But several characteristics inherent to rules-based passive strategies may run counter to these objectives.

Passive portfolios often don’t prioritize tax efficiency, to investors’ cost

In an effort to replicate an index, passive strategies tend to trade more frequently and at higher volumes. Such frequent rebalancing by passive municipal bond funds may lead to higher capital gains costs relative to those for active municipal managers, who have the freedom to tactically manage gains and losses (for instance, by seeking to harvest losses and enhance tax-exempt1 dividends) and are not bound to recognize capital gains associated with market value appreciation as part of a rebalancing process.

We’ve observed that passive strategies, on balance, often pay lower tax-exempt distributions than open-end funds with similar risk profiles, possibly as a result of higher costs associated with a rebalancing process. When looking at the active funds within the Morningstar Municipal Intermediate category, the advantage is marked: The median tax-exempt distribution yield is 141 basis points (bps) higher than the distribution yield for the passive funds within the category (and with a median expense ratio differential of just 37 bps). These higher tax-exempt distributions mean higher tax-exempt income for investors.

The highly fragmented muni market makes index replication costly and inefficient

The sheer size and complexity of the municipal market are also pertinent to the active-versus-passive question. With approximately 40,000 issuers and over 900,000 CUSIPs outstanding across a multitude of sectors, the muni market is highly fragmented relative to the corporate bond market. Replicating and managing to an index with thousands of constituents can be costly and inefficient, and trading dynamics are often unpredictable. An active approach to municipal portfolio construction has the potential to be superior to a rules-based process that aims simply to deliver municipal beta (at whatever cost).

We believe a robust credit research process is crucial. The municipal allocation is often considered a higher-quality component of an investor’s overall portfolio, where capital preservation and high quality income are key objectives. Yet despite relatively low historical default rates for the asset class, investors are coming to realize that the muni market is now a credit market. The decline of insurance from the marketplace (from roughly 60% of primary issuance in 2005 to less than 5% today, according to Thomson Reuters), along with states’ generally slow economic recovery from the Great Recession, has made municipal credit selection increasingly important. This is evidenced by multiple-notch downgrades of some of the largest obligors in the marketplace (Puerto Rico being a prime example, as we discuss below).