“Active funds are now 71% overweight in the FANG companies after making the biggest move from value to growth since 2008.”

. . . Bank of America

Andrew and I have been traveling a lot recently and are getting the same question from both individual investors and professional investors. The question goes something like this: “The 10 largest market capitalization stocks are ‘driving’ the overall stock market’s performance. For those of us old enough to remember, it is very reminiscent of the nifty-fifty phase of an era gone by. That nifty-fifty craze did not end well, so can it be any different this time, especially given the current lofty valuation levels?” Speaking to this point is Strategas’ Chris Verrone writes, “The combined weight of the 10 largest in the S&P 500 is only 19%, still below the long-term average (20%) and not even in the ballpark of what we saw in 1999 (27%).”

Concentration was an American television game show based on the children’s memory game of the same name. Matching cards represented prizes that contestants could win. As matching pairs of cards were gradually removed from the board, it would slowly reveal elements of a rebus puzzle that contestants had to solve to win a match (Concentration). In this case, however, we are not referring to the game show, but rather, the ubiquitous notion that, “The 10 largest market capitalization stocks are ‘driving’ the overall stock market’s performance.” We have often addressed this “concentration” point, most recently in the last two weeks. Piqued by our comments, the uber smart Lawrence Hamtil (Fortune Financial Advisors LLC) pinged me and we began an exchange of emails on the subject. In one of those emails, Lawrence included an article he recently scribed and gave me permission to reproduce it in one of these missives. The individual stock names in his article have been removed because, under the new Department of Labor regulations (The DOL Rule) evidentially we cannot mention any stocks in these reports. Here’s what Lawrence wrote:

In "Relative Equity Valuations, Diversification, and Creative Destruction," I argued that one of the main attributes of the U.S. equity market, - one that warrants it a premium to other global markets, - is its dynamism, which almost ensures that the leadership of the market, whether by sector, industry, or company, is constantly changing. The practical effect of this is that investors in U.S. equities, unlike most of their foreign counterparts, are not relying on the same handful of companies that have dominated other markets for years, if not generations. An additional result of this innate market dynamism is that the ability of only a few giant companies to dominate the market is checked by the creative destruction that serves as a kind of automatic rebalancing mechanism for the market.

To follow up on that theme, I wanted to share a few data points that illustrate that even though the feeling is that the U.S. market (as gauged by the S&P 500 index) is currently dominated by several megacaps the reality is that the current market weightings are fairly average, and perhaps even less top-heavy than it has been in the recent past.

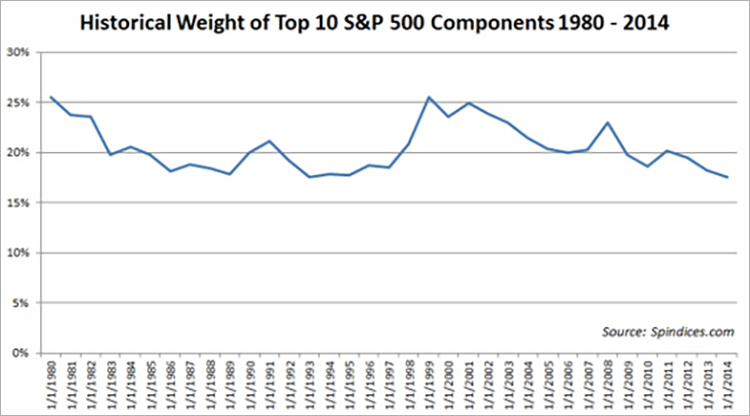

First of all…the current weighting of the top ten S&P 500 components is a little more than 20%, with [one stock] holding the top spot at 3.73%.

This seems fairly concentrated at the top until it is revealed that from 1980 through 2014 (the latest for which I have data), the average weighting of the top ten S&P 500 components was about 20.5%. The current structure is nothing remarkable:

Click here to enlarge

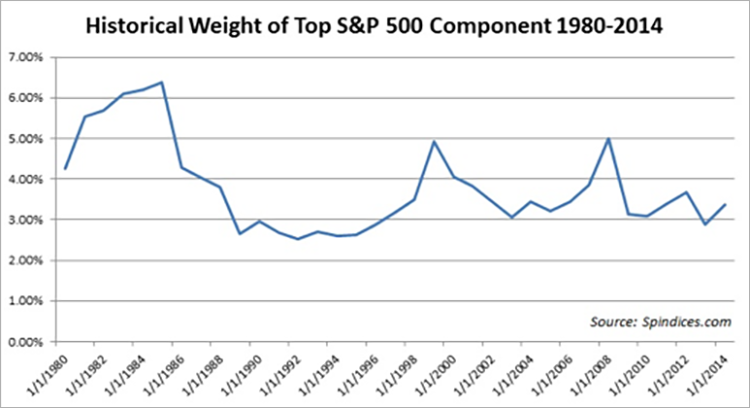

Regarding the S&P 500's heavy concentration in [the top market cap stock], this, too, is nothing remarkable. From 1980 through 2014, the average weighting of the S&P 500's top position was about 3.8%:

Click here to enlarge

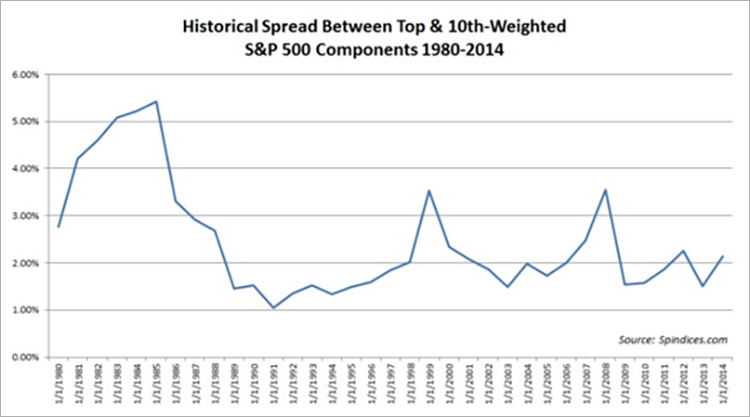

To demonstrate further just how average the current market weighting actually is, one can examine the spread in terms of market weighting between the top component and the tenth-ranked component. The current tenth-weighted component, is about 2.57%. From 1980 - 2014, the average spread has been about 2.4%.

Click here to enlarge

Even though the top portion of the market is remarkably average in terms of size and weighting, there is a legitimate argument to make that growing sectors such as technology are crowding out smaller sectors such as materials and utilities, leaving the market much less balanced on a sector basis than it has been historically. Furthermore, technology companies currently make up about 11% of the top ten of the S&P 500, which is only below 1999 in terms of weighting, when the technology sector made up more than 29% of the S&P 500.

Investors, - particularly those of the passive variety who structure their global portfolios purely based on market capitalization, - would be prudent to consider these factors when structuring their portfolios. Many emerging market portfolios benchmark against the MSCI Emerging Market Index, and as a result, they are likely to have high information technology exposure, given that information technology now composes one-fourth of the MSCI EM Index, which is a larger IT weighting than even that within the S&P 500.

We think Lawrence’s comments are right on point and should put to rest the universal concerns about “over concentration.” As for the “valuation” question, in past letters we have addressed the reason valuations should be higher than the historic norm (more high-growth, high-margin companies in the S&P 500; the tectonic shift from tangible assets to intangible assets; etc.), but the most pushback we get is about the price to earnings multiple (P/E). Granted, just looking at the current P/E ratio on historic bases suggests stocks are expensive. However, as we have pointed out, removing the aberrational low P/Es of the 1970s and 1980s, and beginning in 1990, the S&P 500 average P/E is 23.85. Yet the stock market’s P/E has proven to be not a good predictor of the market future direction. The first problem when using the P/E as a valuation metric is defining which “E” (earnings) to use (GAAP, core, trailing, forward, NTM, as reported earnings, etc.). Second, many investors think an average P/E of below 13 is “cheap” and above 18 is “expensive.” However, this ignores that the current P/E ratio should be based on interest rates. Then there are other metrics like tax rates, inflation, regulations, etc. that determine what the current P/E ratio should be! As stated, in studying P/Es over the years, one finds, “The stock market’s P/E has proven to be not a good predictor of the market future direction.” For example, a bear market began in 1980 when the P/E ratio on the S&P 500 was 9.5 . . . QED.

The call for this week: The S&P 500’s chart pattern is all “coiled up” again (see chart on following page). As the uber smart Jason Goepfert, of SentimenTrader fame, notes:

All coiled up, again. The S&P 500 has gone nowhere since it broke out to a new high three weeks ago. Its range over the past three weeks is one of the tightest-ever following a breakout. That's normally considered a bullish consolidation pattern, but even over the past few years, there were a couple of exceptions to that theory. Historically, how the S&P performed over the next two weeks had a big say in how much it returned over the next year.

We think, consistent with our models’ readings, that the upside chart breakout of three weeks ago is for real. Our models suggest this is the case, and our reading of the stock market’s “internal energy” continues to telegraph there is the potential for a decent upside move from here despite what the negative nabob’s “valuation models” believe. This morning, well that’s not entirely correct, for we are recording this on Sunday night, without the benefit of tomorrow’s news (or future’s pricing readings) because we are speaking at an event. Nevertheless, at 11:00 p.m. Sunday night, the pre-opening S&P 500 futures are “up” and the equity markets look higher into the end of the quarter and the July 4th holiday.

Click here to enlarge

© Raymond James

© Raymond James

Read more commentaries by Raymond James